Lagos, NG • GMT +1

Lagos, NG • GMT +1

270 views

270 views

Following the release of GTCO's Q1'24 financial results, we have updated our assumptions and estimates for FY'24 and subsequent years.

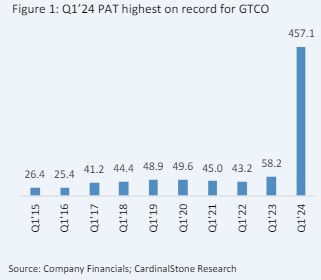

Stellar Q1’24 Financial Performance Rode on Fair Value Gains

The unaudited Q1'24 results for GTCO revealed a 4.4x growth in earnings to N457.1bn. Core earnings (interest income) contributed c.N281.7 billion to this earnings after advancing by 170.6% YoY on the back of improved asset yields (+5.0 ppts YoY to 14.0%) and a 43.9% increase in interest-earning assets (IEA) to N9.5trn from FY'23. Money market placements were a primary fulcrum for the IEA expansion, while the elevated yield environment drove asset yield. Hence, the consequent robust interest income growth masked the 147.9% surge in interest expense and drove net interest income to N227.3bn (+176.7% YoY).

That said, the primary highlight of the results was the N331.6bn fair value gain on financial instruments, which drove a 7.7x expansion in non-interest revenue to N395.0bn and contributed about 49.0% to gross earnings. This gain may have stemmed from the unwinding of c.N100.0 billion net-long FCY positions to meet the new regulatory requirement on net open position limit and the revaluation gains on its dollar-denominated equity investments of c.N800.0 billion. We also note the relatively tamer positive impacts of the growths in fees and commission income (+72.6% YoY) and net trading gains on financial instruments (67.4% YoY) on NIR.

The cost-to-income ratio moderated to 16.0%, with the improvement in operating income (N622.3 billion in Q1'24 vs. N133.7bn in Q1'23) trumping the inflation-induced 76.9% surge in operating expenses. Operating expenses for the period rose to N99.3bn, stemming from increased staff costs, communications, and technological-related expenses, and AMCON charges. Annualised ROAE and ROAA advanced to 105.0% (vs 24.4% in Q1'23) and 16.1% (vs 3.5% in Q1'23), respectively.

We Now Expect FY'24 Earnings to Rise by C.55.0%

Based on the Q1'24 results and subsequent disclosures from management, we now project a 55.0% increase in earnings to N836.5bn for FY'24. This new earnings estimate represents a 35.3% increase from our previous projection and is higher than GTCO's N806.0bn guidance. Our more sanguine outlook also reflects adjustments for the current run rate of NIR, which was buoyed by the N331.6bn fair value gain on financial instruments in Q1'24. As previously highlighted, this gain and potential associated changes in the line item may reflect the effect of the unwinding of c.N100 billion net long FCY position, the revaluation of N800bn dollar-denominated equity investment, and potential net gains on derivative assets.

That said, we also see the latitude for GTCO to extend its robust growth in core performance for the rest of the year, primarily because of a sustained, strong double-digit interest rate environment and a sturdy increase in interest-earning assets. Primarily aided by the drivers highlighted, we note that the bank would still have grown Q1'24 PAT by 128.9% YoY without the impact of the huge fair value gain. Our prognosis for an extension of this strong core performance is hinged on the adjustments to assumptions shown below:

- We have increased our FY'24E loan growth expectation to 37.0% from the cautious 15.0% earlier communicated to reflect the simultaneous impacts of the revaluation of FCY loans and the bank's renewed disposition to loan growth this year. To the latter support, we note that GTCO grew loans by c.33.0% in Q1'24 compared to the average loan growth of 14.4% in the last five years.

- We have lowered our cost-of-risk assumption to 0.5% from 1.0%. In particular, we expect that since the bank has written off sizable legacy problem loans and improved its NPL coverage ratio to 122.7% in FY'23, it is now in a position to return to its 2-year mean cost of risk levels in FY'24.

- Elsewhere, our FY'24 NIR projection has been revised upwards to N526.9 billion from N408.8 billion previously to capture that stronger-than-expected N331.5 billion fair value gain on financial instruments recorded in Q1'24.

- The assumption for FY'24 asset yields was also raised to 14.0% from 13.0% in prior communication to reflect the favourable movements in interest rates. We have cautiously assumed that asset yields will remain flat for the rest of the year, implying that further hawkish monetary policies are an upside risk to this assumption.

- We now expect investment securities to rise to N5.5 trillion in FY'24, aided by the strong 38.0% growth to N3.4 trillion in Q1'24 alone. In our view, this growth in investment securities should reflect strategies to take advantage of the elevated interest rate environment vis-à-vis expectations of moderation/reversal going into FY’25.

- Based on the above, we lower our cost-to-income assumption by 2ppts to 27.0% for FY'24 owing to a more robust operating income

Valuation

Adjustments to our model resulted in a 12-month target price of N74.02, a 6.8% increase from our previously communicated target price (TP). GTCO is trading at a P/B of 0.6x, a steep discount to its 10-year mean of 1.4x and EMEA peer average of 0.9x. We retain our BUY recommendation, with our TP translating to an exit P/B of 1.0x.

Key risk to expectations

- A material Naira devaluation may lead to more gains on revaluating the dollar-denominated N800bn dollar investment, which could bloat earnings. Further, Naira's weakness may also lead to inorganic growth support to gross loans, which may outperform our expectations.

- Conversely, further naira devaluation could also increase risk-weighted assets. However, we expect higher retained earnings to bolster qualifying capital.

- Sharper-than-expected increase in interest rate could drive faster growth in interest income

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top