Lagos, NG • GMT +1

Lagos, NG • GMT +1

981 views

981 views

Saturday, May 07, 2022 / 10.00AM / by TheAnalyst, Proshare research / Header Image Credit: Unity Bank Plc.

Unity Bank Plc. has reported solid earnings growth for 2021 despite analysts' continued concerns about its weak capital base. The bank's 2021 audited accounts showed that the management could navigate the COVID-19-induced 2020 economic slowdown and the modest 2021 economic recovery to pull off gross earnings growth of +8.08% and bottom-line improvement of +52.09%.

In the last three years, the bank's management has been in a pinch, struggling to strengthen capital and reset its customer's experience journey by deploying new capital to upscale digital service delivery. The bank has shuffled along nicely, but it could grow faster with larger tier 1 capital (equity and disclosed reserves).

With the need to meet the Basel III requirement, its tier 1 and tier 2 capital (unsecured subordinated debt and undisclosed reserves) of 8% of its average risk-weighted asset (RWA), its future growth in loans and advances would require an addition to its tier 1 capital.

Highlights

- Unity Bank's gross earnings rose from N46.53bn in 2020 to N50.28bn in 2021, a growth of +8.08%. The bank has seen a gradual growth in gross earnings over the past five years and has reversed its net loss position to a net profit.

- The bank's net profit grew by +52.09% from N2.09bn in the financial year ended (FYE) December 31, 2020, to N3.17bn in FYE 2021. The growth came from a +17.22% rise in fees and commission incomes and a -65.74% decline in net trading loss. The reduction in trading losses boosted total operating income and bootstrapped the bank's bottom line.

- Net remeasurement of expected credit loss (ECL) allowance on financial assets fell from N4.13bn in 2020 to N2.56bn in 2021, representing a -38.01% year-on-year (Y-o-Y) decline. A reduction in credit loss allowance expectations reduced the benefits of the bank's low 0.04% non-performing loans ratio (NPLRs). However, the bank's profit and loss (P&L) accounts remained healthy.

- Unity Bank's other comprehensive income (OCI) for 2021 rose % from Nbn in 2020 to Nbn in 2021, a cause for further thoughts on the bank's earnings stability. A large proportion of the OCI may need reconciliation to the profit and loss (P&L) account down the road.

- The deposit money bank (DMB) saw its high-quality liquid assets (HQLA) drop by -20.21%, from N132.33bn in FYE 2020 to N105.59bn in FYE 2021. The decline resulted from the -32.90% fall in cash. In other words, the bank's liquidity situation tightened a few inches between 2020 and 2021 as cash slowly shrank. The fall in cash could partly be attributed to a slide in customer deposits which fell from N356.62bn in FYE 2020 to N322.28bn in FYE 2021, reflecting a -9.63% drop. Analysts have observed that the bank needs to keep an eye on its HQLA as it could affect

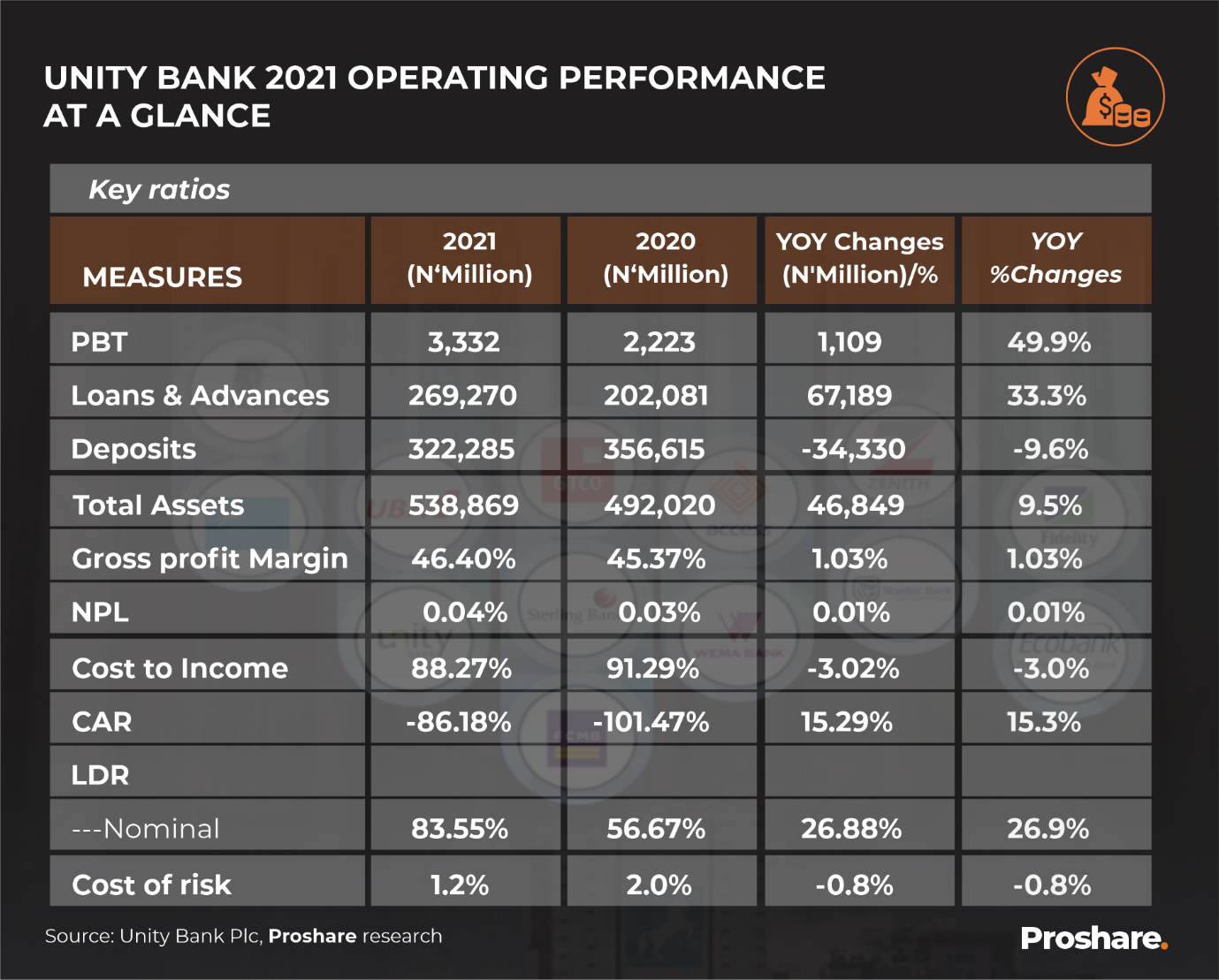

Table 1 Unity Bank Plc Performance Ratios 2021

Profitability- Working on Earnings in Difficult Times

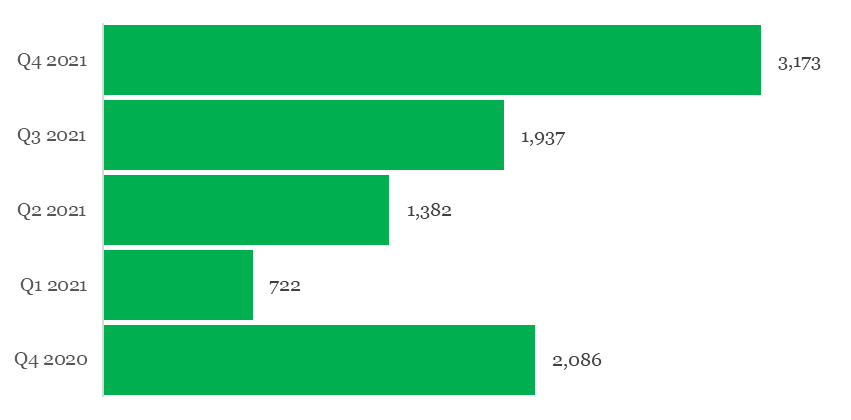

Unity Bank Plc had a relatively profitable year in 2021 as profit after tax (PAT) rose from N2.09bn in FYE 2020 to N3.17bn in FYE 2021, or what came to year on year (Y-o-Y) net earnings growth of 52.11% or an average compound quarterly earnings growth of 11.06%. The earnings numbers may be low relative to industry average net earnings for the year, but the bank's management has pulled off a stellar performance from its complicated recent past. Of course, investors may still feel sore over not being able to take dividends off the table. Still, with negative shareholders' funds of N276.15bn, it might take a while for the bank to be able to pay investors dividends from net earnings. Nevertheless, growth in net earnings could support an upward adjustment in the bank's listed share price, leading to investors benefitting from capital appreciation and future profit-taking opportunities.

Indeed, a further twist could be that the improved earnings position could encourage a new strategic investor to buy a majority stake in the lender. A new investor would perhaps take up shares by an offer for sale by existing shareholders and buy new shares from an offer for subscription. A further advantage of improved earnings is the rise in market valuation of the business and the potential increase in sales value that existing shareholders could receive from an offer for the sale of old shares to a new investor.

Therefore, sustained profitability would be critical to Unity Bank's recapitalization plans (see chart below).

Chart 1 Unity Bank Plc Profit After Tax (N'm) (Q4 2020-Q4 2021)

Source: Unity Bank Plc 2021 Audited Annual Account, NGX, Proshare research

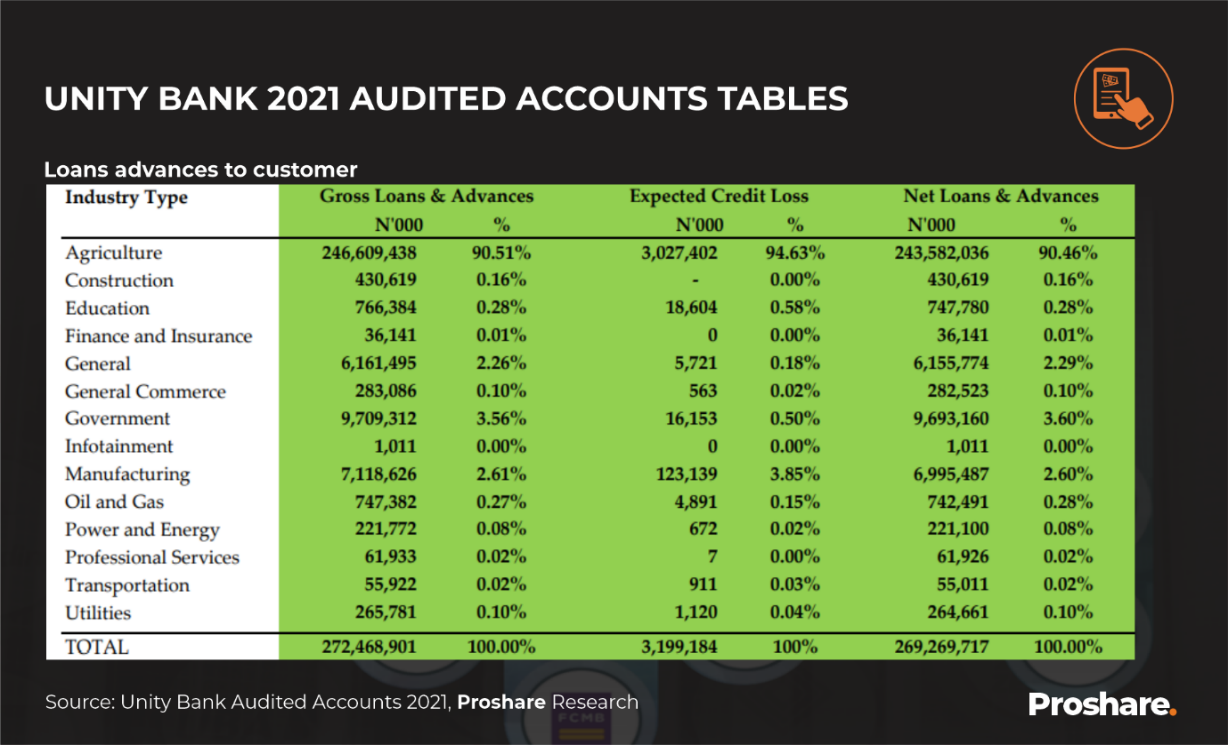

The bank's net earnings margin on gross revenue rose from 4.88% in 2020 to 6.31% in 2021, indicating an improved ability to squeeze profit from income generated from operating activities. Be that as it may, the bank may require additional tier 1 capital to diversify its loan portfolio and improve liquidity (90.51% of the bank's loans went to the agric sector in 2021). Indeed, most of the bank's recent profits have come from a series of Central Bank of Nigeria (CBN)-aided agricultural intervention projects (see loan distribution in the table below).

Table 2 Unity Bank's Sectoral Loans and Advances Allocation, 2021

An Eye on OCIs

The bank's profit and loss account showed an interesting other comprehensive income (OCI) line item. These are usually cost, revenues and other income or expense items that are not immediately considered in the P&L and bottom line. The possibility of mercurial changes in these values has led accountants to shield corporate bottom lines from these items. For Unity Bank, between FYE 2020 and 2021, there was a notable change in its OCI.

Bank OCI net of taxes fell from a positive N1.35bn in FYE 2020 to a negative N3.92bn in FYE 2021. On enquiry about the significant -388.07% difference, the bank explained that the movement in OCI from a gain of N1.35bn in 2020 to a loss of N3.9bn in 2021 was determined by two items:

- These represent the market value of financial instruments (Treasury bills & Bonds) that the bank carries. The bank suffered a net unrealized N7.5bn loss in 2021 (there was a 2020 gain of N0.85bn) on these instruments. The instruments are quoted on FMDQ.com, and market prices periodically change. No actual gain or loss occurs unless the bank sells the instruments. It is worth noting that there has been an upturn in the values in the current year, leading to unrealized gains.

- Equity asset valuation was carried at Fair Value through OCI (FVOCI). The bank enjoyed remeasurement gains of N3.6bn on equity investments in 2021 (2020: N0.51bn). Similarly, gains are only realizable upon the sale of an investment.

Much Ado About Credit Losses

Apart from the Bank's OCI, another figure that nudged analysts' interest was its expected credit loss (ECL) size. Unity Bank's net remeasurement of ECL allowances fell from N4.13bn in FYE 2020 to N2.56bn in FYE 2021, a fall of -38.01%.

In explaining this, the bank noted that "Expected Credit Losses (ECL) are a function of the credit portfolio of the bank. The value is dependent on the historical probability of default (PD), loss given default (LGD), and the value of outstanding credit.

The value is also influenced by the classification of credit facilities. It should be noted that the bank maintained an NPL ratio of just 0.04%, and that contributed immensely to the reduction in ECL numbers. The bank has a model developed by an external consultant (Ernst & Young) that computes the ECL numbers, and the model is independently reviewed by the bank's external auditors (KPMG) to determine the accuracy of the numbers that it produces and the assurance level it commands".

The large improvement in the bank's allowance for expected credit loss (ECL) arises from its low non-performing loans and its agricultural lending support from large CBN agrarian interventions.

The problem with the loan stack of the bank is that it is trapped in the equivalent of a 'key man' risk where a single customer is responsible for a relatively large proportion of a bank's loans and advances. In this case, there is a 'key sector' risk.

Operating Performance 2021- Batting to Win

The bank's management used 2021 to recalibrate its affairs. Analysts have been concerned about Unity Bank over the past three years, particularly regarding its fragile shareholders' funds which have remained negative at a 2021 FYE figure of N276.15bn.

Nevertheless, despite capital adequacy concerns (CAR fell from -101.47% in FYE 2020 to -86.18% in 2021), the deposit money institution (DMB) has painted a picture of the bank management putting in the shift to turn things around, even if modestly.

Net Interest Income

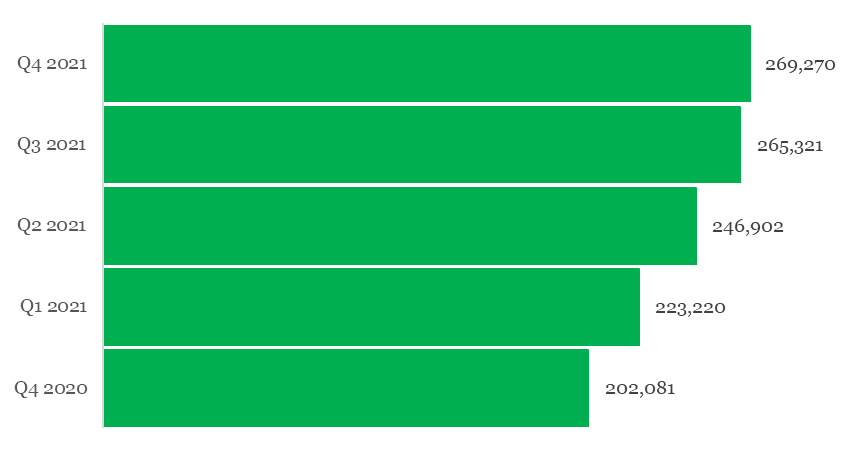

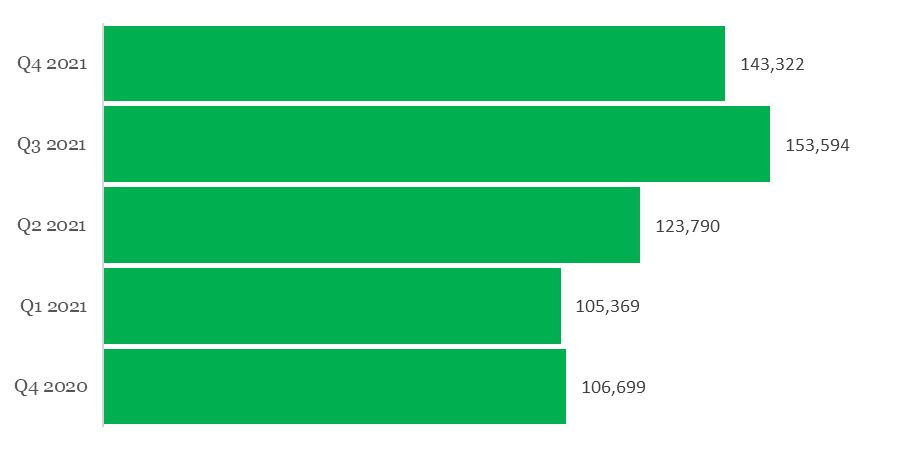

The bank's net interest income rose by +13.01% from N17.75bn in FYE 2020 to N20.06bn in FYE 2021. The rise in net interest income suggests that the bank improved its lending activity in the agricultural sector; this was consistent with a +33.25% rise in its loans and advances Y-o-Y, or what amounted to a compound average quarterly growth rate (CAQGR) of +7.44% (see chart below).

Chart 2 Unity Bank's Net Loans and Advances (N'm) (Q4 2020-Q4 2021)

Source: Unity Bank Plc 2021 Audited Annual Account, NGX, Proshare research

The Deposit Dip

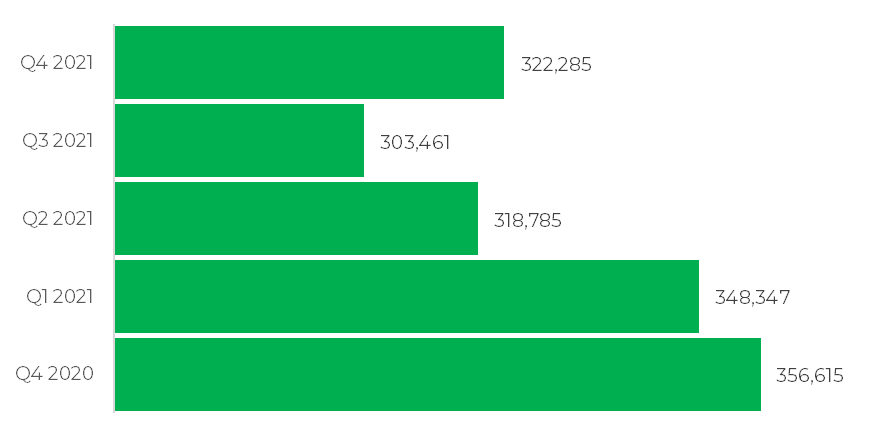

Unity Bank's loans and advance growth were not matched by growth in customer deposits. The bank's customers' deposits fell from N356.62bn in FYE 2020 to N322.29bn in FYE 2021, a slump of -9.63% Y-o-Y or a compound average quarterly fall of -2.50% (see chart below).

Chart 3 Unity Bank Plc Customer Deposits (N'm) (Q4 2020-Q4 2021)

Source: Unity Bank Plc 2021 Audited Annual Account, NGX, Proshare research

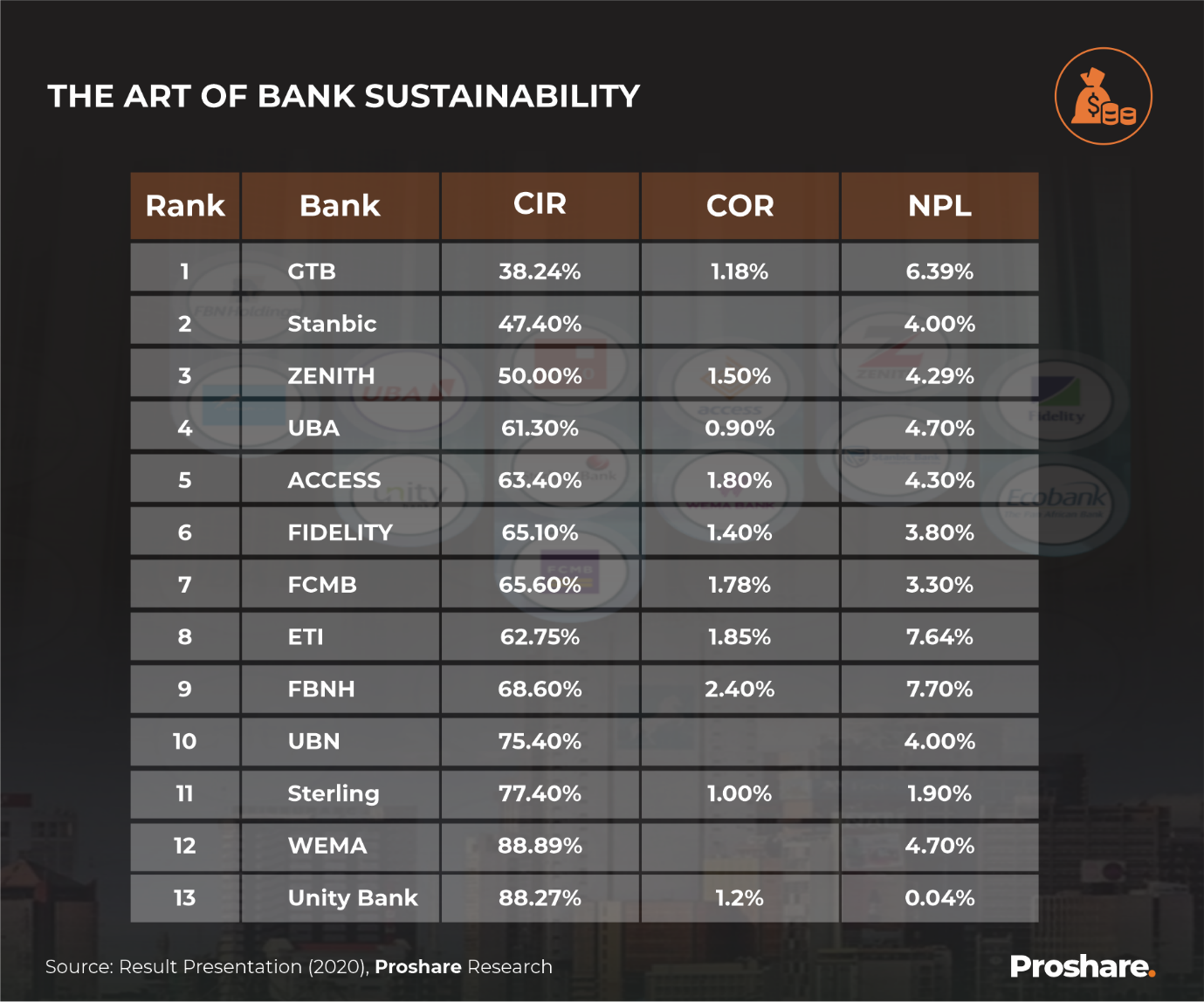

The drop in the bank's deposits from customers partly explains its high cost to income ratio (CIR). Unity Bank's CIR (88.27%) is among the highest within the banking industry, sharing prime attention with Wema Bank (88.89%). The CIRs of both banks contrast the other end of the table, with GTCO posting an FYE 2021 CIR of 38.24% and StanbicIBTC with an FYE 2021 CIR of 47.40%.

On the flipside, Unity Bank’s cost of risk (CoR) is among the best, with a CoR of 1.2% against 2.40% for FBNH, 1.85% for ETI, and 1.80% for Access Holdings. Equally, Unity Bank posted the best non-performing loans ratio (NPLR) for listed bank’s on the Nigerian Exchange Limited (NGX) in 2021, with an NPLR of 0.04% (see table below).

Table 3 Key 2021 Operating Ratios of Nigerian Banks Listed on the NGX

The agric-focused lender appears to have resorted to taking higher-cost deposits from other banks to cushion the fall in deposits from customers on its balance sheet. Y-o-Y, other banks' deposits rose by +34.32% or +7.66% on a compound average quarterly basis (see chart below).

Chart 4 Unity Bank Plc Deposits Due to Banks (N’m) (Q4 Q2020-Q4 2021)

Source: Unity Bank Plc 2021 Audited Annual Account, NGX, Proshare research

High contemporary operating costs for Unity Bank indicate a need to increase the bank’s overall capital and raise the relative proportion of tier 1 reserves in its capital stack.

Agile Liquidity and Nimble Cash

Unity Bank’s management may need to find a ‘sweet spot’ beyond agriculture to ensure sustained operational liquidity. Currently, the bank’s high loan concentration, large deposits due to other banks, falling low-cost customer deposits, and negative shareholders’ funds suggest a need for improved liquidity.

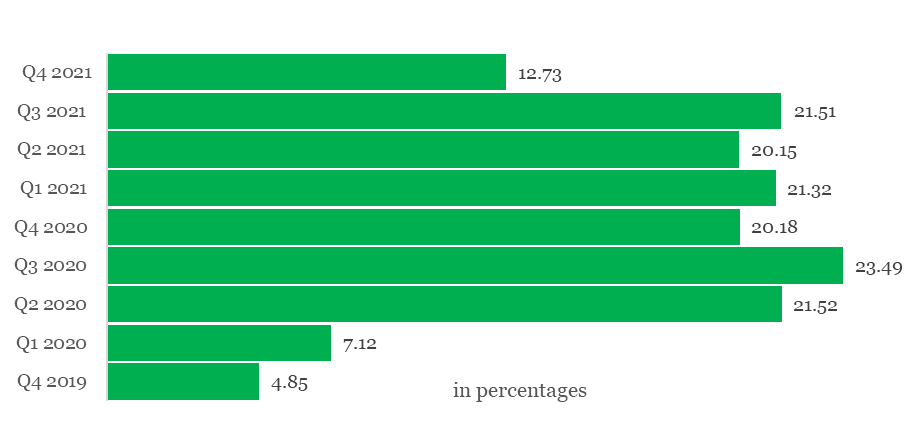

A look at the bank’s balance sheet between Q4 2020 and Q4 2021 shows that the lender has held slightly over 20% of its total assets in liquid items like cash and balances with the CBN. The exception was in Q4 2021 when cash as a proportion of total assets collapsed to 12.73%. The last time such low cash-to-assets ratio were witnessed was in Q4 2019 (4.85%) and Q1 2020 (7.12%) (see chart below).

Chart 5 Ratio of Cash and Balances with CBN to Total Assets (Q4 2019-Q4 2021)

Source: Unity Bank Plc 2021 Audited Annual Account, NGX, Proshare research

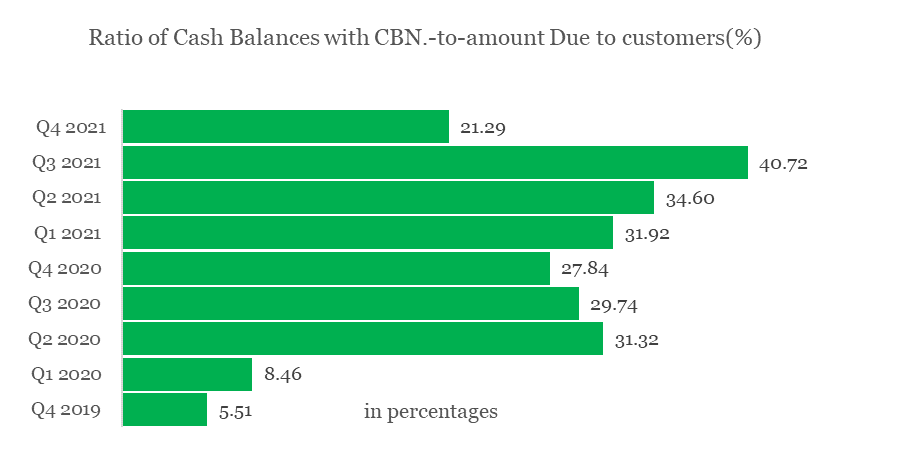

The recent liquidity concerns are reinforced by reviewing the ratio of the bank’s cash and balances with the CBN to its deposit liabilities from customers. Between Q2 2020 and Q3 2021 ratio stayed above 27% and in Q3 2021 rose to 40.72%. Between Q4 2019 and Q1 2020 (the start of the COVID-19 pandemic) the bank’s cash-to-customer deposit ratio was as low as 5.51% in Q4 2019 and 8.46% in Q1 2020. The middle of 2020 saw an upward lunge in cash as the ratio rose to 31.32% in Q2 2020 (see chart below)

Chart 6 Ratio of Cash and Balances with CBN to Customer Deposits (Q4 2019-Q4 2021)

Source: Unity Bank Plc 2021 Audited Annual Account, NGX, Proshare research

A rule-of-thumb minimum cash threshold of one-quarter of customer deposits was sustained until Q4 2021 when the ratio dipped to 21% or what amounted to a fifth of customer deposits.

Excessive cash balances could be a sign of operational inefficiency, but analysts believe that as a proportion of customers’ deposits, banks must hold at least a quarter of such liabilities in the form of operational cash balances. Corporate agility rests on the ability to meet customers’ needs both before and after such needs have been expressed, banks would, therefore, need to understand their average customers’ cash-to-cash cycle and uphold cash and cost-of-carry policy that optimizes the bank’s balance sheet without compromising profitability and customer satisfaction.

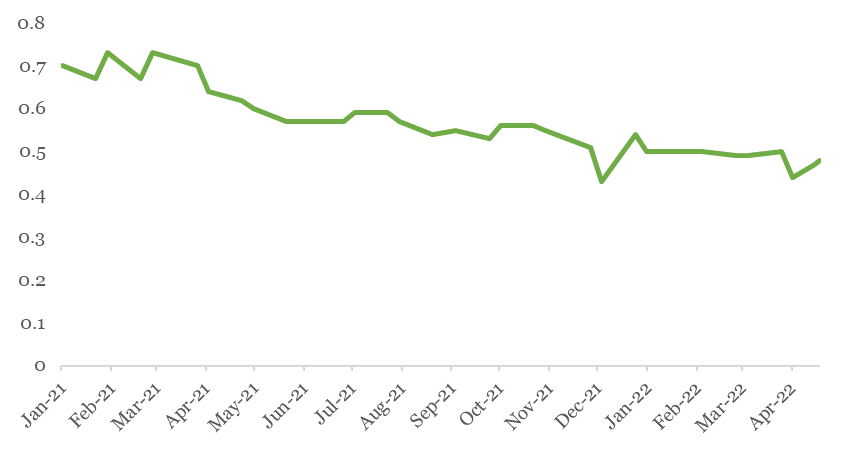

Share Price Blues-Sweating for Success

Tough times do not only shape who we are, they define what we should expect. Unity Bank has had to pass through a season of difficult operating challenges and has started to work through the pain barrier but in doing so it has had to tolerate abnormalities.

The bank’s continued negative shareholders funds and its absence of tier 1 capital make it an unusual lending business. Capital market operators bemused about the bank’s underlying value have generally taken a short (sell) position with the bank’s share price sliding south in a ‘bearish tunnel’ between January 2021 and April 2022 (see chart below)

Chart 7 Unity Bank Plc’s NGX Price Movement Jan. 2021-Apr. 2022

Source: NGX, Proshare research

Thinking Forward

There are indications that the bank is in discussions with prospective new investors who would raise the cash to repair its damaged tier 1 capital and restore its shareholders’ funds to pristine condition.

The bank’s share price may continue to fall a little longer until clear public statements are made concerning the status of its recapitalization programme. The CBN’s Anchor Borrowers Programme (ABP) has helped the bank sustain operations and support stability but this cannot be a sustainable business model. The excessive weight of the agricultural sector in the bank’s loan portfolio makes it susceptible to severe industry shocks that need to be diversified away.

With fresh funds coming from a potential new investor the bank should reconsider its lending portfolio and diversify its sizable sectorial risk. The bank may also need to reduce its cost-to-income ratio (CIR) and intensify its technology-driven approach to customer satisficing. The customer journey experience must see a strong reboot as the bank introduces broader applications of its artificial intelligence (AI) and machine learning (ML) infrastructure. The future cannot be seen but it can be anticipated, Unity Bank will need to clearly rethink, reimagine, and restrategize its future.

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top