Lagos, NG • GMT +1

Lagos, NG • GMT +1

290 views

290 views

Tuesday, March 29, 2022 / 09:40 AM / by Coronation Research / Header Image Credit: iStock

The scorecard for the listed banks that have reported their FY 21 results is mixed. We expect an improvement in earnings in FY 22, albeit a moderate one, given still-low yields and rising costs. The data points to some winners and losers.

Nigerian Banks: FY 2021 Scorecard

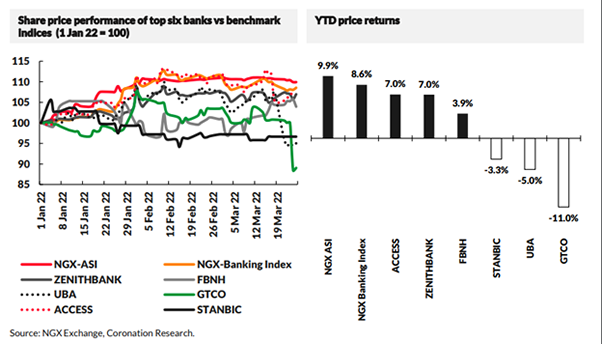

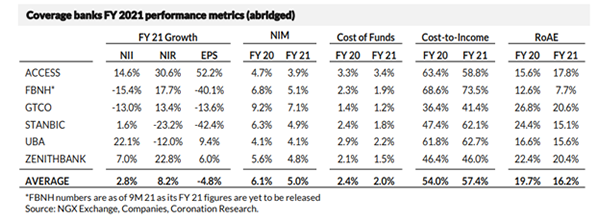

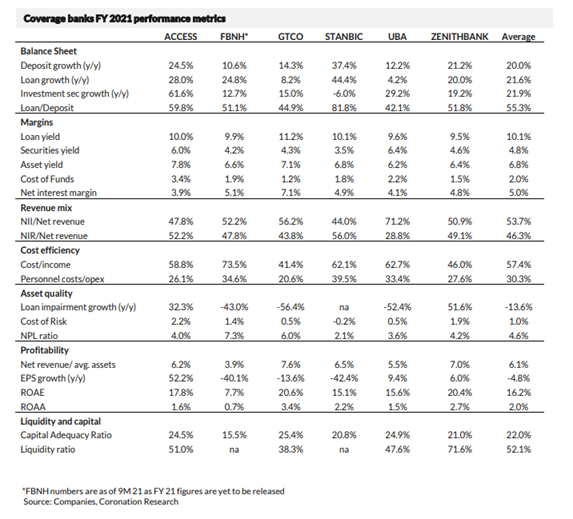

Approximately 80% of the banks within our coverage have now released FY 2021 earnings. Overall, the results across the banks were mixed, with exactly half of the banks recording growth in Net profits while the others recorded Net profit declines. Investors have reacted accordingly, buying up those with solid earnings and good dividend yields (see Coronation Research, The wonder of bank dividends, 7 Mar 2022) and punishing those with weak earnings.

Net interest income, which accounts for c. 54% of the revenues of our coverage banks, remained under pressure in FY 21. Specifically, the still-negative inflation-adjusted market yields adversely impacted their investment securities portfolios. To mitigate this, banks took on more risk, expanding their loan books by 21.6% y/y on average, which is much higher than we had expected.

On lending, most banks stated they were implementing changes (e.g., making loans costlier for customers) in H1 21. However, this did not seem to playout for the most part. In our view, repricing loans upwards proved more challenging for the price-sensitive customer base. As a result, yields on loans were flat across our coverage but were more than double the yields on investment securities. Where banks seemed to be more successful was in lowering their Cost of Funds (borrowing costs). Specifically, the average CoF across the banks we cover fell from 2.4% in FY 20 to 2.0% in FY 21. Overall, average Net Interest Income growth across our coverage was muted (+2.8% y/y). However, Net Interest Margins fell to 5.0% from 6.1% amidst pressured asset yields.

Elsewhere, many banks found alternative means of driving revenue growth. For example, Access Bank benefitted from significant FX gains from its sovereign swap portfolio. At the same time, GTCO and Zenith Bank recorded substantial growth in Fees and Commission income. As a result, on average, Non-Interest revenues (NIR) grew by 8.2% y/y across our coverage banks.

For the most part, we have been cautious about forecasting significant earnings gains for the banks in 2022F. Although there is an upside risk to market yields from increased FGN borrowings to fund the deficit, the CBN continues to signal that it is not in a hurry to hike interest rates.

Q1 22 numbers are likely to reflect the drop in yields from Q4 21, especially on the income from investment securities line. As a result, NIMs are likely to remain pressured. Elsewhere, the CBN's CRR debits put pressure on the margins of several smaller and less liquid banks last year. The CBN has already resumed these debits in 2022 and is likely to continue throughout the year, driving illiquid banks to increase their uptake of expensive interbank and term deposits for funding.

FX

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) strengthened by 0.08% to N416.33/US$1. Elsewhere, the foreign exchange (FX) reserves of the Central Bank of Nigeria (CBN) declined by 0.34% to US$39.53bn, the lowest level since 13 October 2021. However, our view remains that the CBN's position is strong as the additional US$1.25bn Eurobond proceeds will shore up its FX reserves. Hence, we think stability will likely be maintained in the I&E and NAFEX rates in the medium term

Bonds & T-bills

Last week, trading in the Federal Government of Nigeria (FGN) bond secondary market was bearish amidst tight system liquidity. The average benchmark yield for bonds rose by 16bps to close at 10.69%. Notably, the yield on the 3-year (+31bps to 9.10%), 7-year (+21bps to 10.58%) and 10-year (+14bps to 10.90%) bonds expanded. At the primary auction, the Debt Management Office (DMO) allotted N297.01bn (US$713.40m) (including non-competitive allotments) in bonds to investors. Demand at the auction was strong, as a total subscription of N598.42bn, the highest since the January 2020 auction, was recorded, implying a bid-tooffer ratio of 3.99x (versus 3.72x at the prior auction). As a result, the marginal yield on the January 2026 bond declined by 75bps to 10.90%, while the yield on the January 2042 bond fell by 30bps to 12.70%. We expect a rise in bond yields over the medium term owing to an expected increase in domestic borrowing by the FGN.

The average yield in the Treasury Bill (T-Bill) secondary market dropped by 7bps to close at 3.22% amidst limited trading activity. The yield on the 349-day T-bill closed flat at 4.02%. This week, the DMO is expected to roll over N143.29bn worth of maturities to market participants at the T-bill primary auction. Elsewhere, the average yield for OMO bills closed flat at 3.61%; the yield on the 333-day OMO bill closed flat at 4.37%.

Oil

Last week, the price of Brent rose to as high as US$121.60/bbl, the highest level since 8 March 2022, before settling slightly lower at US$120.65/bbl. This marked an 11.79% w/w gain. Year-to-date, Brent is up 55.12 % and has traded at an average of US$97.00/bbl, 36.82% higher than the average of US$70.89/bbl in 2021.

Oil prices extended gains as European Union members were split on whether to join the United States in sanctioning Russian oil, with some countries, including Germany, arguing that the bloc is too dependent on Russia's fossil fuels. Saudi Aramco's supply disruption reappeared with an oil storage facility taking a missile hit, allegedly from Yemen's Houthi militias. Reflecting the tightness in the oil market, the latest data from the American Petroleum Institute showed crude stocks fell by 4.3 million barrels against an estimated crude inventory rise by 100,000 barrels in the week to 18 March.

Elsewhere, storms damaging Kazakhstan's flagship 1.2 mbpd Caspian Pipeline Consortium (CPC) terminal on Russia's Black Sea coast heightened worries of further supply tightening in the market, giving support to prices. However, there are renewed fears over fuel demand in China as Shanghai's financial hub launched a two-stage lockdown today to contain a surge in COVID-19 infections. In our view, significant price volatility is likely to continue, though with Brent comfortably above the US$60.00/bbl mark during the first half of this year.

Equities

Last week, the NGX All-Share Index lost 0.67%, its second consecutive weekly loss, to settle at 46,964.23 points - the lowest level since 2 February 2022. Its year-to-date return fell to 9.94%. Guaranty Trust HoldCo (-11.64%), United Bank for Africa (-11.56%), and Honeywell Flour Mills (-4.56%) closed negative, while Fidelity Bank (+10.00%), PZ Cussons (+8.14%) and Guinness Nigeria (+7.69%) closed positive. Performances across the NGX sub-indices were broadly negative, with the NGX Insurance index (-1.40%) leading the laggards, followed by the NGX Consumer Goods (-1.10%), NGX-30 (-1.05%), NGX Banking (-0.66%), NGX Pension (-0.27%), NGX Oil and Gas (-0.02%) and the NGX Industrial Goods (-0.02%) indices.

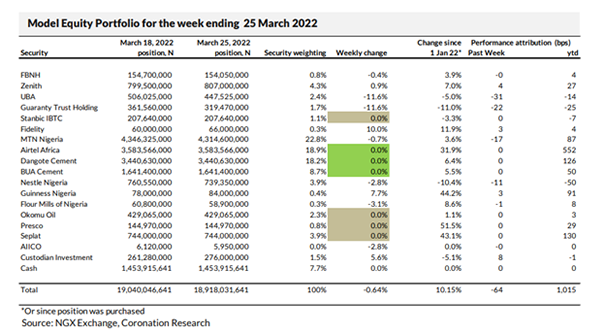

Model Equity Portfolio

Last week the Model Equity Portfolio fell by 0.64% compared with a fall in the NGX Exchange All-Share Index (NGX-ASI) of 0.67%, therefore outperforming it by 3 basis points. So far this year it has gained 10.15% against a 9.94% gain in the NGX-ASI, outperforming it by 20bps.

Last week, there was plenty of damage done by our notional positions in the banks, with UBA costing the portfolio 31bps and Guaranty Trust Holding costing 22bps. On the other hand, almost all this damage can be attributed to the fact that UBA was marked down for going ex-dividend, as was Guaranty Trust Holding. If we add back these dividends, and adjust performance accordingly, then UBA would have fallen 2.3% as opposed to 11.6% and Guaranty Trust Holding would have fallen 1.3% as opposed to 11.8% last week. In other words, when adjusted for dividends, both stocks still fell. We will ask some questions about our notional positions in the banks.

Our notional overweight position in MTN Nigeria cost 17bps. We are content with our notional position in MTN Nigeria as we believe that it is undervalued, and we think that it will perform well when its Q1 2022 results are announced. On the positive side, our 1.5% notional position in Custodian Investment delivered a useful 8bps (it has a very low index weight) while our nearly index-neutral index positions in Fidelity Bank and Guinness Nigeria each delivered 3bps.

Last week we noted that the NGX Exchange All-Share Index had been unusually flat over the preceding six weeks, and we doubted whether it would continue trending sideways for much longer. It seems to us now, on balance, that the market is beginning to trend downwards, though our principal task is not to predict overall market movements but to generate outperformance though stock selection.

What to do about the banks? On 21 February we stated that we would lighten our position in banks, which we began to do. On 28 February we stated that within this process we would rotate out of FBN Holdings and Stanbic IBTC and into Zenith Bank and Guaranty Trust Holding. Then on 7 March we decided to put the process on hold while we assessed the full-year 2021 results and have made no changes to our notional bank positions since then.

Now that we can review the situation (see previous pages), it seems sensible to continue to rotate out of FBN Holding and Stanbic IBTC but to rotate into Zenith Bank and UBA rather than into Zenith Bank and Guaranty Trust Holding. So, this week we will resume lightening our overall notional position in the banks by up to two percentage points (200bps) and within this maneuver rotate out of FBN Holding and Stanbic IBTC and into Zenith Bank and UBA. We will make no further changes, unless we see high liquidity in Custodian Investment in which case, we will take the opportunity to raise our notional stake towards the 2.0% mark.

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top