Lagos, NG • GMT +1

Lagos, NG • GMT +1

198 views

198 views

Tuesday, April 19, 2022 / 06:24 PM / by Coronation Research / Header Image Credit: City Business News

In the first quarter of 2022 the average yield of our basket of Federal Government of Nigeria (FGN) bonds fell by 1.61 percentage points as redemptions swelled liquidity. During the first two weeks of this quarter bond yields have been inching back up, as liquidity conditions are not as good as they were, and the market considers the implications of a revised FGN budget and a headline inflation for March at 15.92%year-on-year (February 15.70%).

FX

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) weakened by 0.20% to N417.50/US$1. Elsewhere, the foreign exchange (FX) reserves of the Central Bank of Nigeria (CBN) gained 0.17% to US$39.72bn, the highest level since 11 March. Our view remains that the CBN's position is strong as the additional US$1.25bn Eurobond borrowing will help shore up the FX reserves. Hence, stability will likely be maintained in the I&E and NAFEX rates in the medium term.

Bonds & T-bills

Last week, trading in the Federal Government of Nigeria (FGN) bond secondary market continued to be bearish as market participants continued to take profit on select instruments across the curve. Consequently, the average benchmark yield for bonds rose (+7bps) to close at 11.05%. Notably, the yield on the 3-year (+39bps to 9.07%) and 10-year (+1bp to 11.50%) bonds expanded; however, the yield on the 7-year (-1bps to 11.06%) bond declined. Looking forward, we expect a rise in bond yields over the medium term owing to an expected increase in domestic borrowing by the FGN.

Activity in the Treasury Bill (T-Bill) secondary market was muted, as the T-bill auction took center stage, bringing the average yield to remain unchanged at 3.32%. However, the yield on the 329-day T-bill declined by 5bps to close at 4.37%. At the primary auction, the Debt Management Office (DMO) allotted N159.03bn (US$380.92m) worth of bills across all tenors. However, demand was weak, as a total subscription of N260.36bn was recorded, implying a bid-to-offer ratio of 1.84x (vs 1.73x at the previous auction). Notably, the rate on the 91-day bill compressed by 1bp to 1.74%, while the rate on the 182-day remained unchanged at 3.00%. However, at the long end, the rate on the 364-day bill rose by 15bps to 4.60% - the highest level since 9 February 2022. Elsewhere, the average yield for OMO bills expanded by 11bps to close at 3.72%; while the yield on the 313-day OMO bill remained unchanged at 4.36%.

Oil

Last week, the price of Brent gained 8.68% to close at US$111.70/bbl, its highest level since 28 March, snapping two consecutive weeks of losses. As a result, Brent is up 43.61% year-todate and has traded at an average of US$98.79/bbl, 39.35% higher than the average of US$70.89/bbl in 2021.

Oil prices climbed as heightened concerns about faltering demand in China eased after Shanghai relaxed some COVID-19 related restrictions even as the Organisation of the Petroleum Exporting Countries and its allies (OPEC+) warned it would be unable to cover the deficit from lost Russian supply. In addition, worries about the continued risk of supply disruptions in the market returned as Russia confirmed that peace talks with Ukraine had come to a dead end.

Elsewhere, news of a larger-than-expected increase in US oil stocks, by 9.38m barrels, was offset by warnings from the International Energy Agency (IEA) that roughly 3.0mbpd of Russian oil could be shut-in due to sanctions or voluntary embargoes from May onwards; as well as Libya being forced to halt some exports in the wake of renewed political protests. Since we take US$60.00/bbl as a benchmark for the health of Nigeria’s public finances (as long as Nigerian production does not fall too far), it appears that oil prices are in the comfort zone and will likely remain there for several months

Equities

Last week, the NGX All-Share Index gained 1.99%, the highest weekly gain since the week ended 4 February, to settle at 47,558.45 points, the highest point since 17 September 2008. Consequently, its year-to-date return rose to 11.34%. Nigerian Breweries (+11.82%), Zenith Bank (+8.70%) and Fidelity Bank (+8.15%) closed positive, while Stanbic IBTC (-5.86%), Sterling Bank (-4.76%) and Unilever Nigeria (-4.51%) closed negative. Performances across the NGX sub-indices were broadly positive, with the NGX Banking index (+5.59%) in the lead, followed by the NGX Pension (+1.14%), NGX-30 (+2.44%), NGX Consumer Goods (+1.89%), NGX Oil & Gas (+1.59%), NGX Industrial Goods (+1.55%) and NGX Insurance (+1.14%) indices.

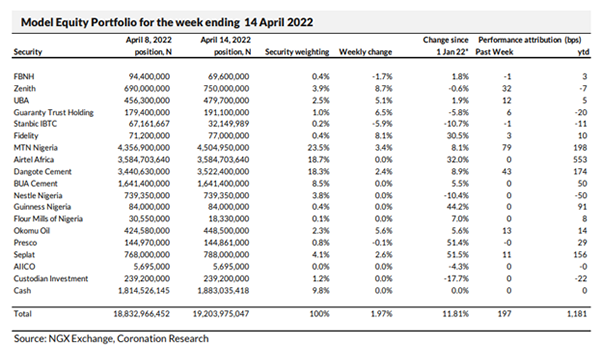

Model Equity Portfolio

Last week the Model Equity Portfolio rose by 1.97% compared with a rise in the NGX Exchange All-Share Index (NGXASI) of 1.99%, therefore underperforming it by 2 basis points. So far this year it has gained 11.81% against a 11.34% gain in the NGX-ASI, outperforming it by 47bps.

Last week the biggest gain came from our overweight notional position in MTN Nigeria which earned us 79bps (a neutral position would have earned us 51bps). We think the stock will continue to perform well in the run-up to the announcement of its Q1 2022 results in a few weeks from now. The neutral notional position in Dangote Cement earned the portfolio 43bps, while the small overweight notional position in Zenith Bank earned 32bps. There were useful contributions from our notional overweight positions in Okomu Oil which delivered 13bps and in Seplat which earned 11bps. It was interesting to see how the price of Dangote Cement, which had been becalmed for months, moved after we published a lengthy report on it on Monday 11 April.

Last week we wrote that the direction of the bank stocks was confounding us, with stock prices moving up while market interest rates were also moving sharply up. Then bank stocks rallied a whole lot more. We sold into the rally, because this is what we advised we would do, but we now need to take stock of the situation. After all, we have made a poor call on the direction of bank stocks, and we need to limit the damage that this is doing to ourrelative performance.

Indeed, our top notional positions, namely MTN Nigeria, Okomu Oil and Seplat, are doing well, and we need to preserve their contributions to the Model Equity Portfolio while not squandering relative performance in the banks. Therefore, we will seek to partly reverse our notional sell-down in banks over the coming two weeks (note the coming week, like last week, has just fourtrading days) and move towards an overall neutral position here.

As earlier advised, we lightened our notional position in Flour Mills of Nigeria last week. This operation has concluded for the time being. If we see significant liquidity in Custodian Investment, we will raise our notional position in it towards the 2.0% mark. We plan no further changes.

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top