Lagos, NG • GMT +1

Lagos, NG • GMT +1

575 views

575 views

Tuesday, May 10, 2022 09:11 AM / by Coronation Research / Header Image Credit: Globalizationpedia

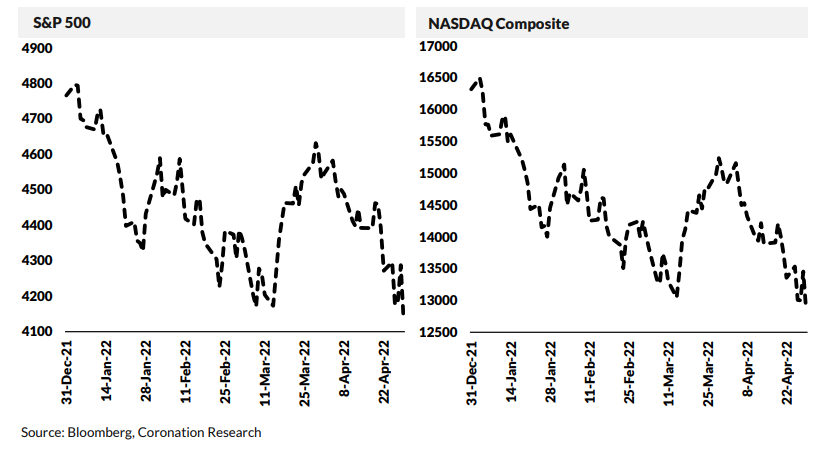

As we often point out, global equity markets do not correlate with the Nigerian Stock Exchange All-Share Index (NGX-ASI). The first four months of this year have provided a spectacular example of this, with the US Nasdaq and the NGX-ASI heading in opposite directions. Nigerian equity investors have reasons to be cheerful.

Global Markets and Nigeria

In a recent publication (see Coronation Research, 2022 Investment Strategy: Optimising Risk and Return, 26 February), we explained how global markets underwent an attack of nerves in the first month and a half of the year. Markets were worried about rising inflation, the required response from monetary authorities (i.e. to raise interest rates), and later by the onset of war in Ukraine. Despite a rally in March, the market rout continued. The S&P 500 is down 13.5% and the Nasdaq Composite is down 22.4% year-to-date.

Rising US bond rates continue to spell trouble for US equity valuations and for market confidence in other developed markets. Such negative sentiment was exacerbated by many companies pulling out from Russia following its invasion of Ukraine on 24 February, and then by the imposition of sanctions.

In our report we stated that while some established business models were proving resilient, other business models (e.g., that of Netflix) are being questioned. Netflix reported poorer-than-expected numbers for Q1 and is forecast to do worse in Q2 as a result of its shaky subscriber base. As this stage, we also note that stocks referred to as Pandemic Darlings, which enjoyed rich valuations due to lockdown measures, are likely to see their sales shrink as the pandemic recedes and the world re-opens

Fundamental Research is back in Fashion

For US equity investors there has been a fundamental change. It is no longer smart to buy and hold tech stocks, still less to ‘buy on the dips’ as the market trends up. This marks the end of a long period – over 10 years – when US equity indices, the Nasdaq in particular, delivered generous returns. Now it is necessary, much more so now than before, for market participants to identify winners from losers. Fundamentalresearch is back in fashion.

Developed market equity strategists are agreed that, going forward, equity returns are not likely to be as generous as they have been over the past decade. The market is weighing up the credibility of monetary authorities, including the US Federal Reserve, to see whether their policy rate increases will be enough to tame inflation. Equity valuations are in the balance.

Going forward, it is difficult to be optimistic about the direction of US equity markets, despite the fact that 80% of Wall Street-listed companies beat earnings expectations for Q1. The challenges are not so much earnings as the bigger questions of inflation and interest rates.

In addition, we consider:

a) the impact of the ongoing war in Ukraine;

b) worsening supply chain bottlenecks;

c) operating costs driven by high crude prices;

d) the possibility of further lockdowns in China to contain the surge in Covid-19 infections in some of its cities.

The Nigerian Equities Market

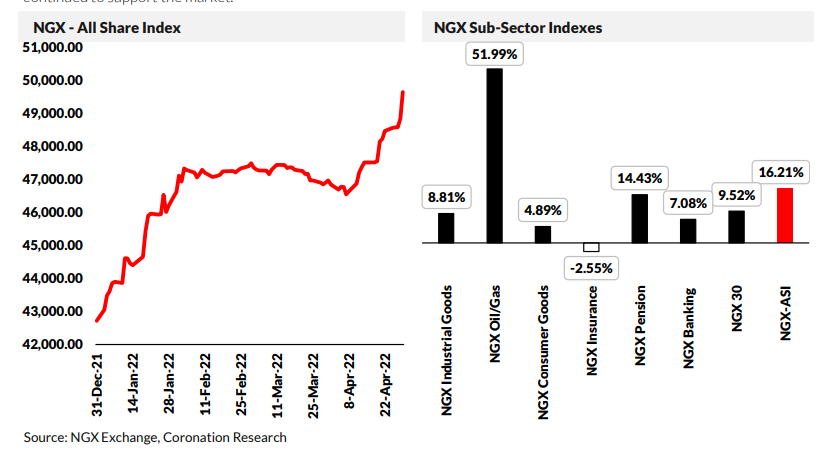

Happily, the Nigerian equity market is disconnected from global markets. The NGX –All Share Index has reached a 13-year high, crossing the 50,000 mark for the first time since 2008. The solid start in January was primarily driven by the listing of BUA Foods (+48.8% since listing), the rally in oil prices reflected in Seplat (+84.6% since 1 January), and investors taking positions in fungible stocks (Airtel Africa and Seplat).

In addition, low short-term market yields have continued to encourage participation in risk assets bringing a 9.15% m/m gain for the index in January, the highest monthly gain since December 2020 and the highest January gain since 2018. Though the market was flatter in February and early March, better-than-expected FY 2021 earnings, positive earnings expectations for Q1 2022, corporate actions, and investors taking positions ahead of FY 2021 dividend payments continued to support the market.

Domestic Naira-based investors continue to dominate activity, and we believe that they are sensitive to changes in market interest rates. According to the NGX Domestic & Foreign Investment report for March 2022, domestic investors’ share of total transactions improved to 77.2% in March from 75.3% in February, while foreign investors’ share was down to 22.8% from 24.8% in February. Going into Q2, we expect the impact of market interest rate increases to be delayed. This may give breathing room for the market, particularly for stocks continuing to show top-line growth, steady margins and earnings growth.

We continue to expect some agricultural stocks to prosper. Commodity prices, both hard commodities like oil and soft commodities like rubber and palm oil, are expected to remain strong, especially in the wake of the EU sanction on Russian energy and the announcement by Indonesia banning oil palm exports. Meanwhile, the strong secular growth trend in telecoms and data services continues to support stocks such as MTN Nigeria (+15.5% since 1 January). There are plenty of reasons for Nigerian equity investors to be cheerful.

FX

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) strengthened by 0.48% to N417.00/US$1. Elsewhere, the foreign exchange (FX) reserves of the Central Bank of Nigeria (CBN) declined by 0.54% to US$39.37bn, the lowest level since 13 October 2021, reflecting the CBN’s continued intervention across the various FX windows. Nonetheless, the FX reserve position is close to historic highs, and we doubt that the CBN wishes to see the exchange rate slip this year. Therefore, we believe that the current I&E Window rate can be maintained within a narrow trading range for at least several months.

Bonds & T-bills

Last week, trading in the Federal Government of Nigeria (FGN) bond secondary market closed bearish as the average benchmark yield for bonds expanded by 12bps to close at 11.28%. Notably, the yield on the 7-year (+32bps to 11.55%) and the 10-year (+15bps to 11.97%) bonds expanded, while the yield on the 3-year bond fell by 8bps to 9.92%. Our view remains that the combination of thin system liquidity and elevated Federal Government domestic borrowing is likely to extend the rise in bond yields over the coming months.

Activity in the Treasury Bill (T-Bill) secondary market was also bearish as the average yield gained 4bps to 3.71%. However, the yield on the 328-day T-bill fell by 1bp to close at 4.47%. Elsewhere, in the first OMO auction in five weeks, the CBN allotted N50.00bn (US$119.90m) worth of OMO bills, maintaining stop rates across the three tenors: 110-day at 7.0%; 187-day at 5.8%; and 362-day at 10.1%, as with prior auctions. In addition, the average yield for OMO bills declined by 12bps to close at 4.09%, while the yield on the 305- day OMO closed flat at 5.04%.

Oil

Last week, the price of Brent rose by 2.79%, its second consecutive weekly gain, to close at US$112.39/bbl, its highest level since 18 April. As a result, Brent is up 44.50% year-to-date and has traded at an average of US$100.44/bbl, 41.69% higher than the average of US$70.89/bbl in 2021.

Oil prices extended gains on the back of the EU's proposal to phase out purchases of Russian crude oil, as well shipping and insurance services for transporting it. So far, the proposal has been hindered by internal disagreements on the phasing-out timeline as countries like Hungary and Slovakia seek exemptions. Elsewhere, the Organisation of the Petroleum Exporting Countries and its allies (OPEC+) maintained the decision to increase their June 2022 production target by 432,000 bpd. This has led to the US Senate Judiciary Committee approving the passage of the "No Oil Producing and Exporting Cartels" (NOPEC) bill that could open OPEC+ members to antitrust lawsuits over collusion to raise global crude oil prices.

Our view remains that Brent is likely to stay well above the US$60.00/bbl mark for several more months. We choose this US$60.00/bbl benchmark because historically, as a general rule, Nigeria's public finances have been strong when oil prices exceeded it.

Equities

Last week, the NGX All-Share Index gained 2.62%, its fourth consecutive weekly gain, to settle at 50,937.01 points, its highest level since 6 August 2008. Consequently, its year-todate return rose to 19.24%. International Breweries (+32.35%), Cadbury Nigeria (+32.20%) and Nigerian Breweries (+22.59%) closed positive, while Oando (-11.75%), FCMB Group (- 7.22%) and Stanbic IBTC (-3.66%) closed negative. Performances across the NGX subindices were broadly positive, with the NGX Consumer Goods (+7.21%) in the lead, followed by the NGX-30 (+3.34%), NGX Industrial Goods (+3.22%), NGX Pension (+1.61%), and NGX Banking (+0.26%) indexes. On the flip side, the NGX Insurance (-1.98%) and the NGX Oil & Gas (-1.10%) indexes were the laggards.

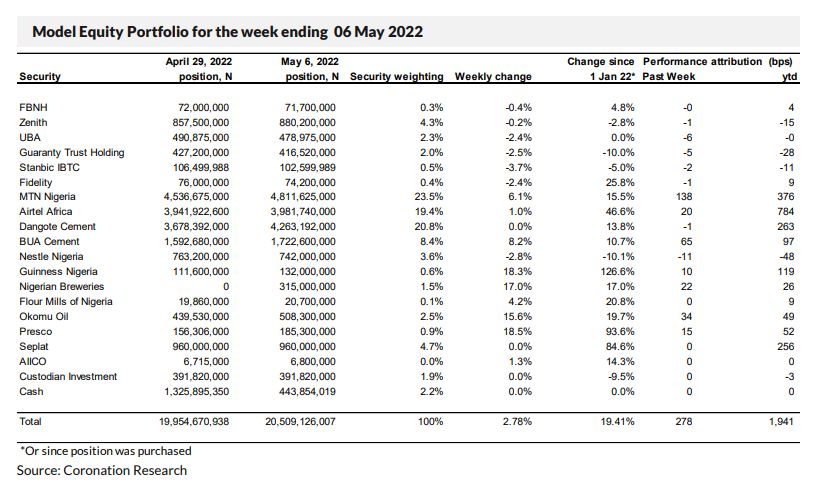

Model Equity Portfolio

Last week the Model Equity Portfolio rose by 2.78% compared with a rise in the NGX Exchange All-Share Index (NGXASI) of 2.62%, outperforming it by 16 basis points. So far this year it has gained 19.41% against a 19.24% gain in the NGX-ASI, outperforming it by 16bps (allowing for rounding of basis points). A benchmark was reached last week when the Model Equity Portfolio doubled its value from its inception in January 2020. It has risen by 105.1% over 125 weeks (a compound annual growth rate of 34.8%) against an 89.8% gain forthe NGX-ASI over the same period.

Last week the main contributors were our notional overweight position in MTN Nigeria, which earned us 138bps (a neutral position would have earned 88bps), our index-neutral notional position in BUA Cement, which earned 65bps, and our overweight notional position in Okomu Oil which earned up 34bps. Losses amounting to 15bps in total were realised in our aggregate notional positions in bank stocks.

Last week we asked ourselves how, in the space of just three trading weeks, we had lost our previous 47bps outperformance of the market year-to-date. The answer was that we were suddenly overtaken by the rally in consumerfacing industrials and particularly the brewing stocks, where we had little representation. Our response was to reiterate that we are happy with our key overweight positions - MTN Nigeria, Okomu Oil, Presco and Seplat - and to begin to increase our position in Dangote Cement to an overweight following our initiation of coverage of that stock, as well as filling up our overall position in banks towards a neutral weight. In addition, we wrote that we would build up a notional stake in Nigerian Breweries because, even if we are not convinced of the business case at this stage, we could profit in the short term by taking some.

Going forward we will continue to build up our notional position in Dangote Cement towards a 400bps overweight position (we are up to 200bps overweight now), which will mean scaling down the rate at which we build up our overall banks position, otherwise we will soon run out of cash. We will continue to build up, tactically, our notional position in Nigerian Breweries towards a neutral weight, but no further. We still study the brewing sector with a view to taking profits over coming weeks, reasoning that the market will soon want to do the same. We plan no other changes this week

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top{kind=link}