Lagos, NG • GMT +1

Lagos, NG • GMT +1

370 views

370 views

Short trading weeks around the Easter and Eid al-Fitr holidays have, in the past, heralded rallies in the NGX All-Share Index and this year is no exception. Today the index exceeded 50,000 points, for the first time since September 2008. Sifting through the data for value is our task.

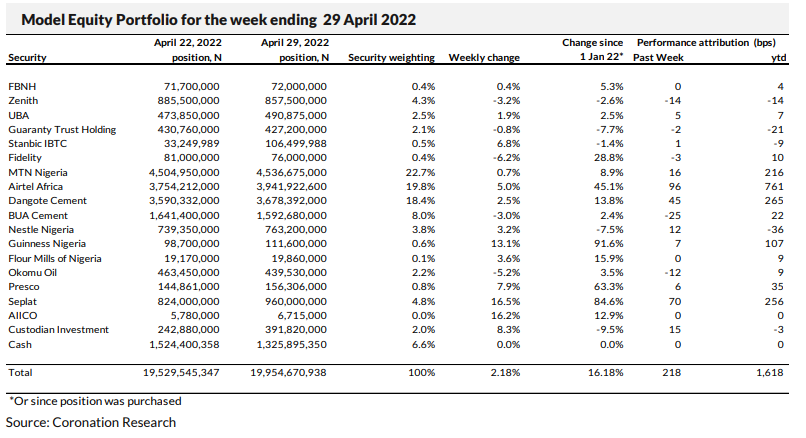

Model Equity Portfolio

Last week, the Model Equity Portfolio rose by 2.18% compared with a rise in the NGX Exchange All-Share Index (NGXASI) of 2.43%, therefore underperforming it by 26 basis points. So far this year it has gained 16.18% against a 16.21% gain in the NGX-ASI, underperforming it by 2bps (allowing for rounding of basis points). This is an unpleasant development, as our underperformance by 26bps last week followed 20bps of underperformance the previous week, in effect wiping out all our hard-won outperformance this year.

What is going wrong? The problem is a significant rally in mid-cap (and therefore not very liquid) stocks in the consumer and brewing sectors, where we have little representation. These stocks do not have much representation in the index, so one would not expect their performance to have much effect. But they have been moving so much that they are having an effect. Nigerian Breweries is a case in point. It represents 1.90% of the index and it rallied by 17.25% last week, giving 33bps of performance for a neutral position. As we are not exposed to the stock at all, we missed out on 33bps of performance in one go

We do these calculations in order to keep our own performance in perspective. We cannot chase every stock that is rallying. For one thing, to do so would be undisciplined and could result in severe underperformance if the gainers later lose. For another thing, we would quickly end up with an entirely neutral portfolio relative to the index, which would limit our room for manoeuvre in trying to outperform it. Our approach is to buy value when we see it, and on occasions like these, we need to remind ourselves of our stance.

As a rule, we do not buy into the idea of consumer-facing industrials and brewers having strong business models. Their ability to pass on price increases to consumers is very limited, in our view. And the announcement that brewers are doing this makes us question whether the consumer is able to footthe bill. We shall see.

Last week, there were positive contributions from our neutral notional position in Airtel Africa (96bps), our double overweight notional position in Seplat (70bps), our neutral notional position in Dangote Cement (45bps), and our overweight position in MTN Nigeria ((16bps). As we wrote last week, we are happy with our key overweight positions in MTN Nigeria, Seplat, Okomu, Presco and Custodian Investment.

Last week, and earlier advised, we continued to build up our overall banks position towards a neutral weight, and we shall continue to do this going forward, though at a measured pace. We took the opportunity, as earlier advised, of strong liquidity in Custodian Investment, to build up a 2.0% notional position in the stock. We have concluded our notional purchases of this stock for the time being. Going forward, we will take our neutral notional position in Dangote Cement towards a 400bps overweight position following our publication on the stock three weeks ago. We will commence building a neutral position in BUA Foods (this will take some time). Much as we do not like chasing stocks, we will build up towards a half-neutral position in Nigerian Breweries, looking for opportunities in short-term corrections here: sometimes one has to be realistic about where the market is heading in the short term, even if one does not agree with it.

FX

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) weakened by 0.16% to N419.00/US$1. Elsewhere, the foreign exchange (FX) reserves of the Central Bank of Nigeria (CBN) declined by 0.48% to US$39.62bn, the lowest level since 5 April, reflecting the apex bank’s continued interventions across the various FX windows. Nonetheless, the FX reserve position is close to its historic high and we doubt that the CBN wishes to see the exchange rate slip this year. We think that the I&E Window rates can be maintained for several months, at least.

Bonds & T-bills

Last week, trading in the Federal Government of Nigeria (FGN) bond secondary market closed slightly bullish as primary market auctions in bonds and T-bills took centre stage. The average benchmark yield for bonds fell by 1bp to close at 11.16%. The yield on the 7-year (- 3bps to 11.23%) bond declined while the yield on the 3-year (+80bps to 10.00%) bond expanded. A newly-listed 10-year bond closed at 11.82%. At the primary auction, the Debt Management Office (DMO) allotted N358.90bn (US$856.56m. Investor demand was for N409.41bn, the lowest since January, implying a bid-to-offer ratio of 1.82x (versus 3.99x at the prior auction). The marginal yield on the January 2025 bond declined by 15bps to 10.00%, the yield on the January 2042 bond rose by 20bps to 12.90% and the yield on the April 2032 (new Issue) closed at 12.5%. Our view remains that the combination of thin system liquidity and elevated Federal Government domestic borrowings is likely to extend the rise in bond yields overthe medium term.

Activity in the Treasury Bill (T-Bill) secondary market was bullish following anticipation of the PMA, bringing the average yield down by 9bps to 3.57%. The yield on the 335-day T-bill closed flat at 4.48%. At the primary auction, the DMO allotted N130.05bn (US$310.39m) worth of bills across all tenors. Total subscription was N249.53b, implying a bid-to-offer ratio of 2.06x (vs 1.84x at the previous auction). Notably, the rates on the 91-day bill (1.74%) and the 182-day bill (3.00%) remained unchanged, while at the long end, the rate on the 364-day bill rose by 19bps to 4.79%, the highest level since 9 February. Elsewhere, the average yield for OMO bills expanded by 21bps to close at 4.21%; while the yield on the 312-day OMO bill gained 79bps to close at 5.04%.

Oil

Last week, the price of Brent gained 2.52%, recovering losses from the week before, to US$109.34/bbl, its highest level since 18 April. As a result, Brent is up 40.58% year-to-date and has traded at an average of US$99.93/bbl, 40.96% higher than the average of US$70.89/bbl in 2021.

Oil prices continued to be volatile as the market weighed the impact of Covid-19 in China versus supply disruption fears as Western sanctions curb crude and product exports from Russia. Elsewhere, oil prices continue to be supported by OPEC-induced tightness as OPEC+ data shows a widening discrepancy between its output objectives and reality as the cartel’s production losses amounted to 1.45mbpd in March and are expected to increase in April as Russia’s production is anticipated to fall.

The IEA is set to release its 240 million barrels over the next months in efforts to drive supply. Nonetheless, should demand bounce back in the summer, tightness could worsen, supporting higher oil prices. Our view remains that Brent is expected to stay well above the US$60.00/bbl mark for several more months

Equities

Last week, the NGX All-Share Index gained 2.43%, the largest weekly gain since the week ended 21 January, to settle at 49,638.94 points, the highest level since 4 September 2008. Consequently, its year-to-date return rose to 16.21%. Cadbury Nigeria (+22.02%), Nigerian Breweries (+17.25%) and Seplat Energy (+16.50%) closed positive, while Fidelity Bank (- 6.17%), Okomu Oil Palm (-5.16%) and Honeywell Flour Mills (-5.13%) closed negative. Performances across the NGX sub-indices were broadly positive, with the NGX Oil & Gas (+10.20%) in the lead, followed by the NGX Consumer Goods (+6.35%), NGX Insurance (+3.43%), NGX Pension (+3.02%), NGX-30 (+2.11%) and NGX Industrial Goods (+0.51%) indices. On the flip side, the NGX Banking (-1.50%) index was the only loser

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top{kind=link}