Lagos, NG • GMT +1

Lagos, NG • GMT +1

250 views

250 views

Tuesday, April 12, 2022 / 10:41 AM / by Coronation Research / Header Image Credit: Dangote Cement

Today we initiate coverage of Dangote Cement, a company which we believe will continue to benefit from strong trends in cement consumption in Nigeria and several other African nations. With a return of equity (RoE) comfortably above its cost of capital, and with this set to improve during our forecast period out to 2025, we think the stock will perform well.

Dangote Cement, African Colossus

Three weeks ago, on these pages, we featured 'The strange case of cement'. Nigeria's cement industry has grown at an average rate of 4.5% per annum over the past four years (2018 - 2021) in inflation-adjusted terms. Not only is this three times the growth rate of the economy overall, it is also much faster than growth in the related construction sector. This begs the question, "Can stock market investors benefit from this?"

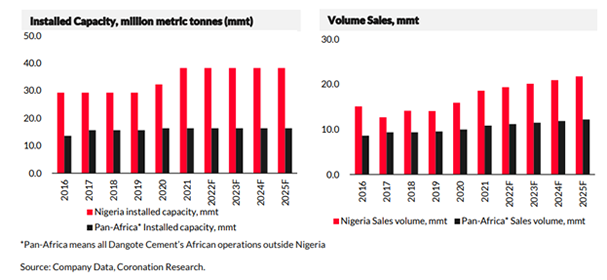

Our key point about Dangote Cement's Nigerian operations is that the company is succeeding in increasing its volume sales in Nigeria, which grew from 15.1 million metric tonnes (mmt) in 2016 to 18.6mmt in 2021, a compound annual growth rate of 4.2%. This period includes the recession year of 2016 (when volume sales fell) and the closure of land borders in 2019 (which interrupted overland exports and brought a slight fall in volume sales that year). How many listed Nigerian manufacturers have recorded volume growth of this order over the past five years?.

Management executes a strategy of building out capacity far in excess of demand in Nigeria, with the consequence that the company's capacity utilisation in Nigeria fell from 51.7% to 48.7% over the period from 2016 to 2021. Yet, remarkably, the commissioning of the 6.0mmt Okpella plant in Edo State last year only led to a slight fall in capacity utiltisation across the totality of its Nigerian plants. Building for future demand appears to be paying off because the market absorbs much of the new capacity.

Having enormous capacity brings a high market share in Nigeria, roughly 60.0%, and with this comes pricing power. Price increases since 2016 have broadly kept up with inflation. When the company combines growing volumes with price increases broadly in line with inflation, the result is sales growth well above the rate of inflation. Economies of scale are developed, and operating margins increase.

The picture in the other African countries is more complicated than in Nigeria (where the company tends not to have a dominant market share) but capacity and volume sales growth is evident there, too.

We initiate coverage of Dangote Cement with a target price of N328.65 per share, implying 20.2% potential upside from Friday's closing price of N273.50/s

FX

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) weakened by 0.01% to N416.67/US$1. Elsewhere, the foreign exchange (FX) reserves of the Central Bank of Nigeria (CBN) gained 0.28% to US$39.65bn, the highest level since 18 March. Our view remains that the CBN's position is strong as the additional US$1.25bn Eurobond borrowing will help shore up the FX reserves. Hence, stability will likely be maintained in the I&E and NAFEX rates in the medium term

Bonds & T-bills

Last week, trading in the secondary market for Federal Government of Nigeria (FGN) bonds was bearish as participants positioned themselves ahead of the Q2 bond issuance programme. Following news of a substantial increase in the FGN's 2022 budget the average benchmark yield for bonds rose by 31bps to close at 10.99%. The yield on the 7-year(+47bps to 11.07%) and 10-year (+62bps to 11.49%) bonds expanded while the yield on the 3-year (- 22bps to 8.68%) bond declined. The Debt Management Office (DMO) duly released its Q2 2022 bond issuance calendar and is expected to offer between N630bn - N720bn (US$1.51bn to US$1.73bn) across the March 2025 (reopening), April 2032 (new issue) and January 2042 (reopening) maturities. Looking forward, we expect a rise in bond yields over the medium as FGN borrowing rises.

Activity in the Treasury Bill (T-Bill) secondary market was also bearish, as the average yield widened by 6bps to close at 3.32%. However, the yield on the 335-day T-bill declined by 6bps to close at 4.42%. This week, the DMO is set to roll over N141.26bn (US$339.02m) worth of maturitie at the T-bill primary auction. Elsewhere, the average yield for OMO bills closed flat at 3.61%; the yield on the 319-day OMO bill remained unchanged at 4.36%.

Oil

Last week, the price of Brent dropped by 1.54%, its second consecutive weekly loss, to US$102.78/bbl, its lowest level since 7 April. Nevertheless, Brent is up 34.14% year-to-date and has traded at an average of US$98.38/bbl, 38.78% higher than the average of US$70.89/bbl in 2021.

It was a topsy-turvy week for oil prices as the market weighed, on one hand, the threats of increased sanctions on Russia, following war crime allegations and a pause in talks to revive the Iran nuclear deal; and, on the other hand, expectations of a combined 255 million barrel stock draw-down by the United States, IEA member countries and Japan. In addition, the resurgence of Covid-19 cases in Shanghai heightened concerns that Chinese demand would falter.

Elsewhere, Russia's 150,000 bpd TAIF refinery in Tatarstan shut down operations due to product overstocking as demand for Russian oil products fell due to Western sanctions, while only India continues to buy from Russia at discounted prices, according to reports. Despite concerted efforts to increase supply by the US and the IEA, prices remain headed for volatile sessions, in our view. The implication for Nigeria, we believe, is that the price of Brent is likely to remain comfortably above the US$60.00/bbl mark during the first half of this year and beyond.

Equities

Last week, the NGX All-Share Index lost 0.45%, extending losses for the fourth consecutive week to settle at 46,631.46 points – the lowest level since 7 Apri. Consequently, its year-todate return fell to 9.17%. Lafarge Africa (-6.78%), PZ Cussons (-5.21%) and MTN Nigeria (- 3.28%) closed negative, while Ardova (+9.87%), Guaranty Trust HoldCo (+6.59%) and International Breweries (+6.59%) closed positive. Performances across the NGX sub-indices were mixed, with the NGX Oil & Gas index (+3.14%) leading the gainers, followed by the NGX Banking (+1.51%) and NGX Pension (+0.87%). On the flipside, leading the laggards was the NGX-30 (-0.43%), followed by NGX Industrial Goods (-0.42%), NGX Consumer Goods (- 0.35%) and the NGX Insurance (-0.42%) indices.

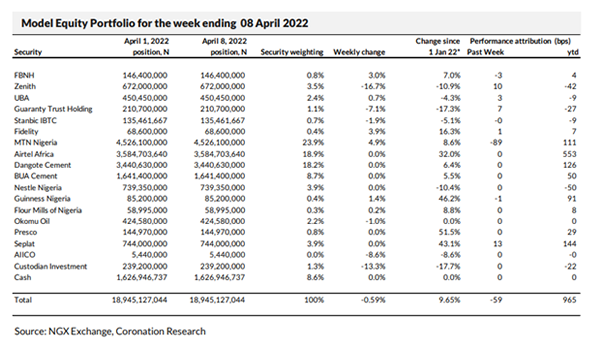

Model Equity Portfolio

Last week the Model Equity Portfolio fell by 0.59% compared with a fall in the NGX Exchange All-Share Index (NGX-ASI) of 0.45%, therefore underperforming it by 14 basis points. So far this year it has gained 9.65% against a 9.17% gain in the NGX-ASI, outperforming it by 48bps.

Last week the biggest loss came from our overweight notional position in MTN Nigeria which cost us 89bps (a neutral position would have cost us 58bps). We are not perturbed: the stock was marked down for a final dividend payment (i.e., it went ex-dividend) of N8.57 per share on Thursday. Such a performance in the underlying share is to be expected (and note the useful 4.0% gross dividend yield). If we adjust for the gross dividend, the stock was up 0.3% on the week. We expect it to perform well when its Q1 2022 results are announced in a few weeks from now and the market may indeed anticipate this.

Elsewhere the portfolio was helped by a rise in our total aggregate position in banks which delivered 18bps. Our notional overweight position in Seplat which delivered a useful 13bps.

Last week we raised close to 100bps in notional sales of bank stocks, as earlier advised (although we did not get as much done as originally intended). Also, as earlier advised, we lightened our notional holding in Flour Mills of Nigeria.

The direction of bank stocks confounds us. The overall market is falling (though not by very much), and the direction of market interest rates is sharply upwards, as seen by the rise in FGN bond rates last Thursday, in reaction to the rise in the FGN budget and the commencement of the Q2 2022 FGN bonds issuance programme. In these conditions we would expect bank stocks to be weak (assuming that they will find it difficult to pass on interest rate rises to their customers later this year). Perhaps this a timely reminder that our real job is not to predict the overall direction of the market, but to buy value when we see it.

We still intend to make notional sales of up to a further 100bps in bank stocks, and considering that this week and next week will be short trading weeks, we will spread this over eight trading days. If we see high liquidity in Custodian Investments, we will to raise our notional stake in it towards the 2.0% mark. We intend to further lighten our notional position in Flour Mills of Nigeria. We plan no further changes.

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top