Lagos, NG • GMT +1

Lagos, NG • GMT +1

246 views

246 views

Tuesday, March 22, 2022 / 10:47 AM / by Coronation Research / Header Image Credit: Grist

Nigeria's economic fortunes wax and wane and so do those of its construction sector. But over the past four years the cement sector has been unusually buoyant. Why?

The Strange Case of Cement

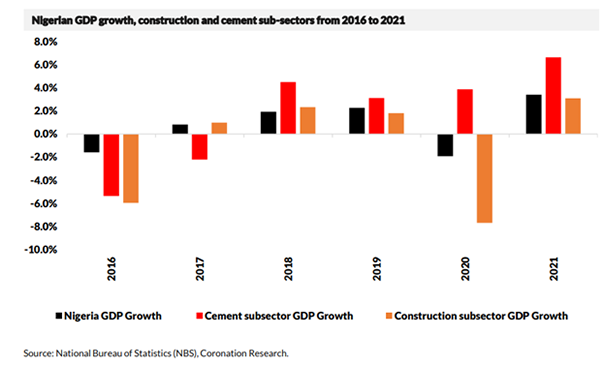

Nigeria's listed cement companies together account for some 30.0% of the NGX Exchange All-Share Index, yet the cement industry itself accounts for just 0.9% of GDP, according to data from the National Bureau of Statistics (NBS). So, is cement's over-representation on the exchange good or bad? In our view, it is good because cement is growing much faster than GDP overall.

Although the cement sector fared poorly during 2016 and 2017, it has been growing at an average of 4.5% per annum (pa) over the past four years (2018 to 2021) in inflation-adjusted prices, according to the NBS, which is about three times the rate of GDP growth over the same period. It has also been growing much faster than the construction sector.

The construction sector tends to grow when the economy grows and to shrink when the economy contracts. As a result, construction performs very poorly (see the chart entries for 2016 and 2020) when the economy is in recession. By contrast, the cement industry's performance has very little correlation with the economy overall, even growing during the recession year of 2020.

The size of the cement sub-sector gives us an important clue as to why this is so. It is roughly 25% of the size of the construction sector, a percentage that tallies with the cost of building the frame of a building (reinforced concrete beams, blocks) compared with its total build-cost. In other words, it seems that so long as there is enough money around to start a building project, people will do so. The ability to meet the much higher costs of erecting a roof, installing plumbing, windows and electrical wiring is susceptible to swings in the economy, in our view, and can be delayed for years while funds are found.

The next question is, "Where does the money come from in the first place?" After all, almost everyone suffers in a recession, including builders, whether they are large-scale companies or the millions of people who build their own homes. The answer, in our view, is likely to be connected with remittances. Remittances from Nigerians overseas can be negatively affected by global recession but are nevertheless substantial sums paid directly to family members during good years and bad. If our reasoning is correct, then it would account for the expansion of the borders of cities like Lagos year-in, year-out, and the success of the cement industry.

FX Market

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) declined by 0.04% to N416.67/US$1. Elsewhere, the foreign exchange (FX) reserves of the Central Bank of Nigeria (CBN) declined by 0.11% to US$39.70bn, the lowest level since 14 October 2021. On the positive side for reserves, in its eighth outing in the International Capital Market, the Debt Management Office (DMO) priced a US$1.25bn Eurobond issue with a coupon of 8.375% to finance critical capital projects in the budget. Consequently, our view is that the CBN's position will strengthen. Hence, stability will likely be maintained in the I&E and NAFEX rates in the medium term, we believe.

Bonds & T-bills Market

Last week, trading in the Federal Government of Nigeria (FGN) bond secondary market was bearish as market participants anticipated renewed supply at this week's bond primary auction. Consequently, the average benchmark yield for bonds rose by 10bps to close at 10.53%. Notably, the yield on the 7-year (+25bps to 10.37%) and 10-year (+34bps to 10.76%) bonds expanded, while the yield on the 3-year (-6bps to 7.23%) bond tightened. On Wednesday, the Debt Management Office (DMO) is expected to offer N150bn (US$360m) - N75bn of the January 2026 and N75bn of the January 2042 - worth of bonds to investors. We maintain our expectations of a rise in bond yields over the medium term owing to an expected increase in domestic borrowing by the FGN.

Activity in the Treasury Bill (T-Bill) secondary market was bullish as system liquidity remained buoyant. As a result, the average benchmark yield for T-bills dropped 13bps to close at 3.29%. The yield on the 356-day T-bill closed at 4.02%. At the primary auction, the Debt Management Office (DMO) allotted N172.61bn (US$414.25m) worth of bills across all tenors. Demand was strong, as a total subscription of N364.65bn was recorded, implying a bid-to-offer ratio of 6.28x (vs 5.14x at the previous auction). As a result, the rate on the 91- day bill fell 1bp to 1.74%, while the rate on the 182-day shed 28bps to 3.00%. At the long end, the rate on the 364-day bill fell by 10bps to 4.00% – the lowest level since 10 February 2021. Elsewhere, the average yield for OMO bills fell by 31bps to 3.61%; the yield on the 340-day OMO bill closed at 4.37%. At the OMO auction, the Central Bank of Nigeria (CBN) sold N40bn worth of bills to market participants and maintained stop rates across the three tenors.

Oil Market

Last week, the price of Brent fell to as low as US$96.02/bbl, the lowest level since 21 February 2022, before recovering to US$107.93/bbl. Nevertheless, the price still settled 4.21% lower, marking the second consecutive weekly drop for the commodity. Year-to-date, Brent is up 38.76% and has traded at an average of US$95.04/bbl, 34.07% higher than the average of US$70.89/bbl in 2021.

The Energy Information Administration (EIA) announced that oil inventories in the United States climbed by 4.3 million barrels during the week to 11 March to 415.9 million barrels, against an expected decline of 1.4 million barrels. Against this, hopes that Russia and Ukraine would come to some sort of agreement during the most recent round of talks evaporated, sending oil prices back above the US$100/bbl threshold. The IEA stated that the current energy crisis may worsen during over the coming weeks if the war in the Ukraine does not end. In our view, significant price volatility is likely to continue, though with Brent comfortably above the US$60.00/bbl mark during the first half of this year.

Equities Market

Last week, the NGX All-Share Index lost 0.33%, reversing most of last week's gains to settle at 47,282.67 points - the lowest level since 8 March 2022. Consequently, its year-to-date return fell to 10.69%. MRS (-9.96%), Seplat Energy (-6.06%) and Access Bank (-3.45%) closed negative, while PZ Cussons (+17.01%), Ecobank Transnational Inc (+8.18%) and Presco (+6.40%) closed positive last week. Performance across the NGX sub-indices were broadly negative, with the NGX Oil and Gas index (-3.87%) leading the laggards, followed by the NGX Insurance (-2.93%), NGX Consumer Goods (-0.43%), NGX Pension (-0.36%), NGX 30 (- 0.19%) and the NGX Banking (-0.17%) indices. On the flip side, the NGX Industrial Goods (+0.14%) index closed positive.

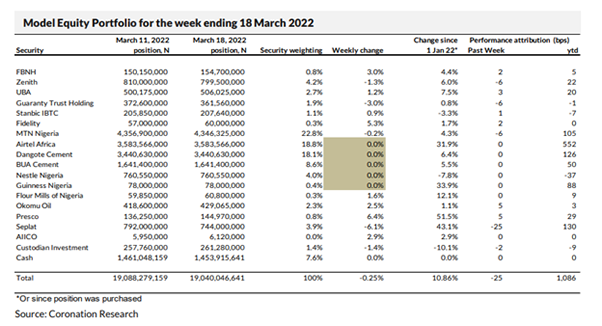

Model Equity Portfolio

Last week the Model Equity Portfolio fell by 0.25% compared with a fall in the NGX Exchange All-Share Index (NGX-ASI) of 0.33%, therefore outperforming it by 7 basis points. So far this year it has gained 10.86% against a 10.69% gain in the NGX-ASI, outperforming it by 17bps.

Our technique is to take overweight notional positions in stocks which we believe are undervalued, and vice-versa. We do not make large decisions regarding the direction of the market overall, unless circumstances are exceptional (as they were in Q1 2020, for example). That said, we have noticed that the performance of the NGX Exchange All-Share Index has been unusually flat over the past six weeks (it is up 0.01% since 4 February), which is an unusual formation for any equity market anywhere in the world. And last week there was no price change in four large index weights: Airtel Africa; Dangote Cement; BUA Cement; Nestle Nigeria (all highlighted in the table). We would expect a change in market direction soon (reasoning that a market cannot be flat for long). For the time being the decline in short-term market interest rates appears to be the factor holding it up, though bond rates tells a slightly different story.

Last week the biggest single loss came from our double-overweight notional position in oil & gas company Seplat, which cost us 25bps. As we wrote a fortnight ago, we must be prepared for Seplat's price to be volatile: but if we are convinced of the company's value (especially with oil prices high and the possible execution of an excellent acquisition announced by the company) then we will stick with our position. Other losses came from our notional positions in banks. Our overweight notional positions in Okomu Oil and Presco made useful contributions, 5bps each, last week.

Last week, and as earlier advised, we took advantage of exceptional liquidity in Custodian Investment to slightly raise our notional stake. This week we plan no changes to the Model Equity Portfolio though, again, if we see high liquidity in Custodian Investment then we will take the opportunity to raise our notional stake towards the 2.0% mark.

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top