Lagos, NG • GMT +1

Lagos, NG • GMT +1

166 views

166 views

Tuesday, April 26, 2022 / 09:18 AM / by Coronation Research / Header Image Credit: Ecographics

As we wrote last week, the Federal Government of Nigeria (FGN) bond market is correcting as market liquidity remain tight and participants consider the likely consequences of significant government borrowing. The strange thing is that the equity market is rallying. We suspect this has to do with the shortness (four days either side of the Easter break) of recent trading weeks, in which case we would expect more volatility next week around the Eid al Fitr holiday.

FX

Last week, the exchange rate at the Investors and Exporters Window (I&E Window) weakened by 0.20% to N418.33/US$1. Elsewhere, the foreign exchange (FX) reserves of the Central Bank of Nigeria (CBN) gained 0.19% to US$39.81bn, the highest level since 4 March. Given that the data for the CBN's FX data is a moving average and given that proceeds from the recent Eurobond issue are being included, this strength does not surprise us. The FX reserve position is close to its historic high and we doubt that the CBN wishes to see the exchange rate slip this year. Therefore, we believe that the current I&E Window rate, or something very close to it, can be maintained for at least several months

Bonds & T-bills

Last week, trading in the Federal Government of Nigeria (FGN) bond secondary market remained bearish as system liquidity continued to tighten and market participants positioned themselves ahead of primary market auctions in bonds and T-bills this week. Consequently, the average benchmark yield for bonds rose (+11bps) to close at 11.16%. Notably, the yield on the 3-year (+13bps to 9.20%) and 7-year (+13bps to 11.19%) bonds expanded; however, the yield on the 10-year (-2bps to 11.48%) bond declined. Today, the Debt Management Office (DMO) is expected to offer N225bn (US$537.85m) - N75bn each of the March 2025 (Re-opening), April 2032 (New issue) and the January 2042 (Re-opening) - in bonds to investors. Our view remains that the combination of thin system liquidity and elevated Federal Government domestic borrowings is likely to extend the rise in bond yields over the medium term.

Activity in the Treasury Bill (T-Bill) secondary market was also bearish following lowered demand and anticipation of the PMA, bringing the average yield up by 35bps to 3.66%. Notably, the yield on the 342-day T-bill closed at 4.48%. The DMO is expected to offer N5.86bn (US$14.01m) worth of maturing bills to market participants. Elsewhere, the average yield for OMO bills expanded by 23bps to close at 3.95%; while the yield on the 319- day OMO bill closed at 4.25%.

Oil

Last week, the price of Brent rose to US$113.16/bbl, before settling at US$106.65/bbl, down 4.52%, its lowest level since 20 April. The loss reversed some of the gains of the week before. As a result, Brent is up 37.12% year-to-date and has traded at an average of US$99.55/bbl, 40.43% higher than the average of US$70.89/bbl in 2021.

Oil prices moderated following strong selloffs on the prospects of weaker economic growth as the International Monetary Fund (IMF) cut its global growth forecast from 4.4% to 3.6% for 2022. The chances of a half-point interest rate hike by the US Federal Reserve alongside an announcement by Shanghai of further round of Covid-19 lockdowns heightened concerns about faltering demand, pushing down prices. Elsewhere, the European Commission stated that Russia's newly introduced gas payment system to receive Rubles for its energy exports might be compatible with the EU sanctions regime, easing fears across the European oil & gas markets.

Our view remains that Brent is expected to stay above the US$60.00/bbl mark during for several more months. We choose this US$60.00/bbl benchmark because historically, as a general rule, Nigeria's public finances have been strong when oil prices exceeded it.

Equities

Last week, the NGX All-Share Index gained 1.89%, the second consecutive week of gains, to settle at 48,459.65 points, the highest point since 15 September 2008. Consequently, its year-to-date return rose to 13.44%. Oando (+21.33%), Guinness Nigeria (+17.50%) and Lafarge Africa (+10.61%) closed positive, while Unilever Nigeria (-3.94%), Access Holdings (- 2.44%) and Guaranty Trust Holdco (-1.22%) closed negative. Performances across the NGX sub-indices were broadly positive, with the NGX Oil & Gas (+6.36%) in the lead, followed by the NGX Consumer Goods (+3.31%), NGX Pension (+2.05%), NGX Industrial Goods (+1.65%), NGX-30 (+1.50%), NGX Banking (+0.60%) indices. On the flip side, the NGX Insurance (-0.05%) index was the only loser.

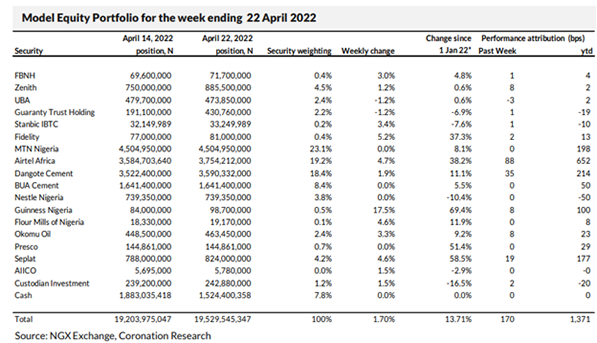

Model Equity Portfolio

Last week the Model Equity Portfolio rose by 1.70% compared with a rise in the NGX Exchange All-Share Index (NGXASI) of 1.89%, therefore underperforming it by 20 basis points (allowing for rounding of basis points). So far this year it has gained 13.71% against a 13.44% gain in the NGX-ASI, outperforming it by 26bps.

Last week there were big gains from our notional positions in Airtel Africa, which delivered 88bps, and in Dangote Cement, which delivered 35bps. In these two stocks we have notional positions close to their index weights. Our overweight notional position in Seplat earned a useful 19bps last week

The reason we underperformed the market last week was that a number of mid-cap stocks rallied quickly, and we are not much exposed to them, with the exception of our notional and neutral position in Guinness Nigeria. It was the second short week (just four trading days) in a row and perhaps it was not surprising to see participants driving stock prices hard. In that case we should not worry too much about our underperformance, even though to miss the benchmark by 20bps in a single week is a lot. We are happy with our key overweight positions in MTN Nigeria, Seplat, Okomu, Presco and Custodian Investment.

Last week, and earlier advised, we began to take our overall position in the banks back towards an overall neutral weight and we will continue to execute this going forward. If we see significant liquidity in Custodian Investment, we will raise our notional position in it towards the 2.0% mark. In addition, we intend to build up to a neutral position ion BUA Foods. No further changes are planned.

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top