Lagos, NG • GMT +1

Lagos, NG • GMT +1

12565 views

12565 views

Sunday, December 15, 2019 / 14:47PM / By Ajibola Alfred / Header Image Credit: Straplan Advisory

The need to enhance stakeholder capacity for ongoing and future reforms through awareness.

Globalfinancial access and inclusion is on the rise

The finance and creditsystem is the key enabler of the other sustainable development goals,particularly in reducing poverty and in giving people dignity. Over the lastdecade, building inclusive financial systems has become an important objectivefor policy makers around the World. This has led to dramatic improvements infinancial access globally.

According to GlobalFindex, its 2017 database shows that the global share of adults who have anaccount with a financial institution or through a mobile money serviceincreased to 69% in 2017 from 62% in 2014, and 1.2 billion adults have obtainedan account since 2011. This share has also increased in developing economies,from 54% to 63%, amid gender constrains in account opening. Digital technologyhas become a key support and enabling pillar in the financial space worldwide. 'Technology giants have also moved into the financial sphere, leveraging deepcustomer knowledge to provide a broad range of financial services'.

Each economy has its ownstory of successes, challenges, and opportunities concerning financialinclusion, and the effects of these outcomes depend mainly on the strength ofthe credit architecture of each country. Nigeria achieved 63% financialinclusion in 2018 from 36.3% in 2010. It seeks to achieve 80% by 2020.

As with many developingcountries, an all-inclusive access to affordable finance and credit is still achallenge in Nigeria, particularly to women, rural dwellers and MSMEs. But theCBN and its stakeholders have been working to firm up Nigeria's creditarchitecture - strengthening the legal and regulatory framework to removeconstraints to the rights of both creditor and borrower thereby unlockingaffordable financing. This report therefore speaks to those government reformswhich focused on raising the pillars on which the operationalization of astrong credit and financial system lies, specifically, credit information,non-possessory interests and secured lending in movable assets, and creditorrights and insolvency frameworks. The report also serves as a platform forawareness to all stakeholders in line with the StraplanAdvisory tradition.

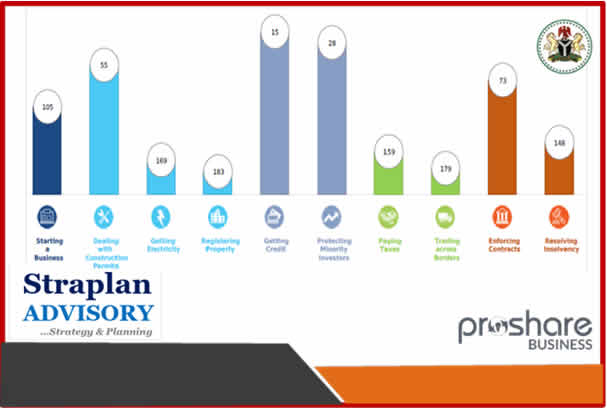

Nigeria's ranking in theGetting Credit category which rose from 44th in 2016/17 to its highest rankingof 6th position in 2017/18 has since slipped to 12th in 2018/19 and now 15th inthe recently released doing business report 2020. Although Nigeria's score in2020 re-mains the same as the previous year, it's ranking dropped as morecountries implemented significant reforms within this category and improvedtheir scores to leapfrog Nigeria.

Specifically, economieslike Azerbaijan, Jordan and Tajikistan upstaged Nigeria to rise respectively to1st, 4th and 11th positions in the 2020 report from 22nd, 134th and 122nd inthe previous year, despite Nigeria retaining its high score of 85 out of 100points.

Under the Getting Creditindicator, the World Bank's scope covers the depth of credit informationsystems and strength of secured trans-actions system and non-possessorysecurity interests of each country. Specifically, it measures the following:scope and accessibility of credit information distributed by credit bureaus; aswell as number of individuals and firms listed by the largest credit bureau asa share of the adult population. It also measures the availability of featuresfor the protection of rights of both borrowers and creditors through effectivecollateral and bankruptcy/insolvency laws.

Nigeria's Getting Creditranking by the World Bank did not improve this year owing to two key factors:

1. Theinefficiency of registration of movable assets under the secured transactionsregime which is a dual process. In particular, the manual process of registeringmovable assets at the Corporate Affairs Commission (CAC) by companiesregistering their charges. This manual process undermines the online real timenature of information on movable assets accessible through the NationalCollateral Registry (NCR), the main registry for movable assets, as recognisedby the Secured Transactions in Movable Assets (STMA) Act.

2. The absence ofan established regulatory frame-work for insolvency and creditor rights tobring clarity into issues of priority and enforcement of rights for securedcreditors.

The WB ranking however isfocused on the high-level, the strength of the credit architecture, where asits operationalization is an enduring game involving various stakeholders. TheCBN has consistently demonstrated its commitment and efforts towards anall-inclusive easy access to affordable finance and credit in Nigeria.

When Nigeria rose to 6thposition in 2017 in the World Bank Getting Credit ranking, a section of thepublic were sceptical about the credibility of the claim. They cited theattendant challenges with accessing credit for both MSMEs and individuals. Whatmost of the critics were not aware of was that the World Bank's methodology wasfocused mainly on the architecture of credit, the pi-lars upon which anefficient credit system can thrive sustainably. And Nigeria has over timesuccessfully built a sustainable credit architecture which impact is graduallyunfolding.

Over the last decade, theCBN and other stakeholders have embarked on several access to credit andfinancial inclusion reform initiatives in line with the sector's FinancialSystem Strategy (FSS) and National Financial Inclusion Strategy (NFIS) 2012(revised in 2018). The last five years have particularly recorded significantreforms to improve the legal and regulatory environment of credit in Nigeria.

Currently, access tocredit is still a challenge in Nigeria but the foundation for a sustainable,efficient and transparent credit system has been laid and the outcomes, whichshould not be taken for granted, is beginning to yield fruits in terms ofincrease in credit, particularly through digital channels.

In its five year-strategydocument (2019-2024), the CBN established access to finance and financialinclusion as the main thrust of its activities over the next five years. Thereforms undertaken and ongoing have interesting outcomes but many of thestake-holders are not aware of the broader context. Thus, the reforms meandifferent things to different people.

In order to understandwhat the CBN and stakeholders have been doing, it is important to view thechallenges of access to credit in Nigeria from various lenses: one, is the needto unlock credit by increasing liquidity in the system and channelling it tothe real sector.

Financial institutions,particularly banks, are encouraged to create credit to enable individuals andbusinesses to meet their obligations, thereby creating value and wealth. It isessential to point out that in doing this, financial products must be tailoredto the needs and lifestyle of the immediate society.

The second aspect is thereach of these financial products to the whole society, particularly theunderserved who are clustered in the rural areas and the payment framework. Thethird aspect is in strengthening the rights of both borrowers and creditors.

It is important tostrengthen creditor rights through a framework that establishes the clear rulessurrounding issues of default and effective enforcement. Similarly, improvingconsumer literacy (including awareness of their rights) and enforcing consumer protectionthrough effective consequence management are quite important to the creditframework.

FIG 1: The pillars: fundamental plumbing of the financialsystem for economic growth and development. Recent reforms and regulatorydirectives on credit have been around these areas.

Note:

The principle of reformsfrom the government's angle is enhanced transparency and efficiency oftransactions.

The reforms have varieddimensions, from legal to regulatory and institutional reforms. Awareness ofwhat is going on is still poor.

FIG 2:

Reforms in Context: Addressing the challenges ofaccessing credit and financial inclusion

The Nigerian economy is basically cash-drivenand secured bank loans have been the main source of lending and obtainingcredit for individuals and micro-small and medium enterprises (MSMEs).

FIG 3:

Althoughaccessing credit is becoming easier in Nigeria for mostly bank customers,following recent reforms, it is an onerous task for most, with cumbersomedocumentation procedures and requirements. Loans are primarily secured withreal estate. Collateral is one of the main challenges of individuals and MSMEsseeking credit and loans.

Unfortunately,there is a mismatch in the type of assets owned by companies and collateralrequired by the banks. Records show that about 70% of total collateral obtainedby banks as security for loans to MSMEs are in real estates. Where as, 70% ofcapital stock of MSMEs in developing economies are in movable assets(machinery, equipment and receivables) to pledge. Movable assets typically formabout 70% of capital stock of MSMEs.

Affordability:loans are typically costly and not easily available to individu-als and MSMEs.Lending rates are usually high, average lending rate to consumers and MSMEs isabove 30%. Loan assessment, monitoring, and enforcement is still considered ahuge challenge by many lenders. There-fore, the financial service providerstend to prefer to invest in risk free securities than extend loans to MSMEs.

Longterm capital remains a challenge for the industry. Despite significant shortageof dwellings, mortgage loans are relatively in short supply and equally costly.

Financial inclusion isstill far from target; but the foundations have been laid

In 2018, about 63million adult Nigerians had access toboth formal and informal financial products, leaving 36.6 million people stillexcluded from accessing any form of financial products and services. Although,banking products dominate the array of financial products, only 39.5millionadults used banking services during the same period, while informalalternatives catered to a huge 14.6 million people or 15% of the adultpopulation.

77% of the unbanked are in the rural areas, thusconstituting a challenge to reach them easily with the same brick and mortarmodel. Digital payments have generally increased albeit slowly, from 12% to 16%between 2016 and 2018. Despite the increase it is narrowly confined to theformal, banked consumers and not yet within the reach of the 60 millionunbanked. The use of mobile money is deepening than expanding due to thedominance of the 'banked'.

Main barriers to financial inclusion remain lack ofproducts/services and channels; financial organizations unwillingness to lend;awareness and knowledge, and institutional exclusion and affordability.

Unlocking Credit:Legislative reforms

Therehas been some improvement in Nigeria's credit industry lately, particularly inthe ease of acquiring consumer credit by bank customers, owing to the variousreforms initiated in the past and ongoing ones. This improvement is howeverunequal and uneven. Compared to the potential of the credit architecturefollowing these important reforms, the growth of the credit industry is clearlyin its formative stage, set to build momentum.

Somany factors discourage or constrain financial institutions from unlockingcredit to the real sector and diversifying collateral requirements. Theseinclude issues of risk assessment-availability of credit information and KYC onborrowers and potential borrow-ers, especially in the rural areas; lack ofclear creditor priority rules and enforcement issues; stringent conditionsrequired by the CBN guarantee and intervention funds; hitherto lack of acentralised registry and legal framework; weak rural financing skills andknow-how, etc.

Inview of the aforementioned challenges faced by banks, the legal reformsundertaken were to provide fundamental and sustainable solutions to unlockcredit to the real sector: Without some external system of accountability,people do not cultivate the practices and habits necessary to develop internalaccountability (Daniel B. Klein, Associate Professor of Economics at SantaClara University).

TheCredit Bureau and Secured Lending in Movable Assets Acts: Strengthening riskassessment and improving credit culture:

CreditBureau Act - The availability of reliable credit information is sine qua non tosound decision making on credit provision by banks and other lenders. Thisrequirement is an end to end pro-cess involving collection of information aboutborrowers from all credit providers including banks, utilities,telecommunication companies, and even retailers, and establishing a uniqueidentification across all relevant institutions.

Inthe past, weak credit information systems had kept the Nigerian bankingindustry vulnerable to incidents of huge non-performing loans and increasedrisk in MSME and consumer lending. To address this situation, the CBN hadembarked on a series of reforms to increase credit information in the bankingindustry starting with the establishment of the Credit Risk Management System(CRMS), a public credit registry operated by the CBN, in January 1998. By 2008,the CBN released the Guidelines for the Licensing, Operations and Regulationsof Credit Bureaus in Nigeria. The Guideline was reviewed and made more robustin 2013 leading to the licensing of three privately owned credit bureaus - XDSCredit Bureau (now First Central Credit Bureau), CR Services Credit Bureau andCRC Credit Bureau.

However,these steps only remained regulations restricted to the financial servicessector, as there was no law to effectively support their operationalizationacross a wider spectrum of credit providers and borrowers. By 2017, the creditreporting Act (CRA) was en-acted and provided an established credit informationframework which expanded the scope of information obtainable on con-sumeraccounts across all credit providers, including utilities, telcos, retailers,etc,.

Theuse of credit information to determine reputation can help in many transactionssuch as applications for bank loans, insurance, apartment rental, utility,post-paid phone service, etc. The credit bureau act of 2017 is expectedly todrive significant in-crease in both unsecured and secured credit to the realsector and enable diversification of collateral requirements.

Nigeria'sthree private credit bureaus collect and maintain credit information for themutual benefit of all credit providers and interested parties, includingdeposit money banks, mortgage banks, micro-finance banks, finance & leasingcompanies, tele-communications, utility companies, service providers,retailers, landlords, etc.

AlthoughNigeria's credit bureau coverage (the number of individuals and firms listed ina credit bureau's data-base as a percentage of the adult population) hasexpanded to 14% of the adult population from 11% in 2018. it remains low incomparison to 67% in South Africa, and 100% in the US and UK.

Thecredit bureaus issue credit reports, credit scores and portfolio monitoringreports to enhance transparency and efficiency in the credit system. A wideruse of credit reports as basis for both financial and non financial transactionsis increasing the transparency and efficiency of loan assessment and riskmanagement of credit providers in Nigeria.

Creditscoring, an inclusive product that assigns every potential borrower a firststep assessment of their credit worthiness, is set to redefine credit cultureand assessment in Nigeria. Portfolio monitoring as a product will deepen thebanks' risk management.

Accordingto a World Bank Group publication, recent study in the United States finds thatthe acceptance rate for new loans increases by 10% when data from energyutilities (and 9% for telecoms) are included in the consumer credit reports,while the default rate declines by 29% (and 27% for telecoms).

Overtime, particularly since the establishment of credit bureaus, creditinformation reforms have enhanced financial sector stability and been able tocurtail non-performing loans from reaching huge levels in Nigeria. Forinstance, the increased ratio of non-performing loans in the banking systemoccasioned by the volatility in commodity prices in 2015/2016 has reduced from15% in June 2017 to 9% in May 2019, while capital adequacy and liquidity ratiosremained intact.

Creditbureau information fuelled explosion in consumer and mortgage creditavailability in the US. 45% of US households have mortgage loans. In 2001, 84%of automobile loan applicants in the U.S. received a decision within an hour,23% of applicants received a decision in less than ten minutes and manyretailers opened new charge accounts for customers at the point of sale in lessthan two minutes.

Creditproviders are now building capacity by increasing internal capacity orpartnership with fintech companies to use data and analytics to managetrade/consumer credit. Building fintech capacity would be a key competitivefactor amongst banks in the medium term. Credit scores provided by creditbureaus will also go a long way in engendering efficiency in fair assessmentinto the market.

Lendershave not adequately incorporated analytics and credit scoring methods inpricing interest rates on loans and credit: On average, with regards tointerest rate on loans, applicants are treated equally, from most creditworthyto least creditworthy, thereby discouraging customers with high disposableincome from taking loans.

Creditreporting can also be explored from a subnational perspective as the unbankedand financially illiterate are majorly in the rural areas.

Toraise the stakes to par, it would require a lot of engagements, advocacy andawareness amongst stakeholders.

Movable Assets, Non-PossessoryInterests and the Collateral Registry

Alongwith the Credit Bureau Act, the Secured Transactions in Movable Assets Act(STMAA) is another important economic law enacted in 2017. The STMAA providedthe legal and regulatory framework to facilitate the use of movable property ascollateral for both business and consumer lending, and a system for lenders toregister non-possessory security interests with a collateral registry. The keyobjectives were the diversification of collateral base of banks to reflect thereality of MSMEs and consumers, enabling the use of securities such asinventory, receivables, leases, farm products, equipment, electronic devices,jewellery, etc., to secure loans. The set-up of the National CollateralRegistry (NCR), a web-enabled and notice-based platform by the CBN was toengender transparency and secure the right of lenders to register theirinterests in movable assets thereby enhancing fair assessment of loans onmovable assets and their monitoring. Studies have shown that the introductionof collateral registries in many climes have led to increased availability ofcredit to firms and at better terms.

For instance, the introduction of secured transactionlaws and a centralized online registry for accounts receivables and leases inChina in 2007 and 2008, respectively, unlocked over $3.5 trillion in financingwithin a decade, with SMEs as the main beneficiaries. The law also opened upthe factoring and leasing industries in China. In Australia, within two yearsof its launch in 2012 the number of new registrations rose to 2.36 million andnumber of times searches were conducted increased by 1.4 million from 5.8million in 2012 to 7.3 million in 2014.

Since the inception of the National CollateralRegistry in Nigeria three years ago, there has been increased growth in securedloans in movable assets registered on the platform and the number of searchesconducted to determine status of secured as-sets. As of October 2019, 655lenders have registered to use the platform for their movable asset loans,including 566 micro-finance institutions, 21 deposit money banks (DMBs), fivedevelopment finance institutions (DFIs), 36 finance companies, four merchantbanks, one non-interest bank and 22 non-bank financial institutions. About N1.8trillion (approximately $5.9 billion) worth of financing statements have beenregistered on the platform with over 200,000 beneficiaries including 196,279individuals and 9,911 MSMEs. Cumulatively, the number of searches conductedhave increased to 57,700. 78% of these searches were conducted by financialinstitutions while there have been 12,902 searches by public users. Therelatively low number of searches by public users is an indication of the levelof awareness and adoption amongst potential borrowers. The lack of awarenessabout the registry and its functions among stakeholders is one of thechallenges to be addressed, especially at the subnational level.

Weak Creditor Rights andInsolvency Framework Undermines the Pillar of Trust:

Creditorrights and insolvency is the third pillar of the reforms undertaken by thegovernment in unlocking credit. Its regime in Nigeria is weak and inadequatewith huge negative implications for the efficiency of the financial sector andaccess to finance.

Lackof clear creditor priority rules and enforcement issues have constrained theoperationalisation of security interests in movable assets and non-possessoryinterests by financial institutions. Banks are reasonably reluctant to lend onsecured movable as-sets because framework establishing priority rules withininsolvency or bankruptcy proceedings is weak. As a result of unclear priorityrules, effective enforcement of security interests is also undermined. Legalproceedings against defaults are considered to be expensive and lengthy andseen to typically favour debtors to the detriment of lenders. This furtherdiscourages lenders from unlocking credit to the system and when they do, theyprice in the risks and weaknesses in the business environment thereby raisingthe cost of loans and making it more difficult to access credit in Nigeria.

Forinstance, majority of the 655 financial institutions registered on the portalhave not been active. This includes majority of microfinance banks, non-bankfinancial institutions, finance companies, merchant banks and developmentfinance institutions. Another indicator of activity level is the relatively lownumber of MSMEs that have so far benefitted as a percentage of the over 37million MSMEs in Nigeria.

Itis however important to note that the government and stake-holders, led by thePresidential Enabling Business Environment Council have been working to addressthis inadequacy as part of the Companies and Allied Matters Act (CAMA) Repealand Re-enactment Bill 2018. This is one of the biggest bills for business-es ingeneral and its enactment remains top on PEBEC's agenda as one of thelegislative reforms that would drive the ease of doing business across theboard. The CAMA bill was passed by the National Assembly in 2019 but yet to getthe president's assent. This may require further advocacy to speed up itsre-enactment. There is need to speed up other finance-related legislativereforms, like the factorisation and assignments bill and the warehouse receiptsbill which are yet to be enacted into law.

Butthe recent small claims courts reform offers palliative, particularly at thelocal level: The small claims court reform re-quires a magistrate of aspecialized court to adjudicate on cases involving values not more than N5million ($16,333) and to deliver judgment speedily within 14 days of completionof hearing. It offers cost and speed advantage and will enhance enforcement andconsequence management especially for litigations at the subnational level.

Allstakeholders must be aware of these critical reforms to co-drive transparencyand efficiency as well as accountability and continued monitoring andevaluation for sustainable impact.

Next Steps for DeepeningCredit Information

Credit Reporting: There isstill need to increase the coverage of credit data suppliers (more Telcos,Landlords, Retailers, Courts and Collateral Registry) and create more awarenessabout the use of credit reporting as an enabler of credit in financial trans-actionsand even measure of character in the fulfilment of specific roles or positions.It can also be used as a form of vendor management. Many entrepreneurs do notknow that they can report credit defaults to credit bureaus to facilitatepayments.

Credit bureau coverageneeds to extend beyond 14%. The number of individuals and firms covered by theCredit Bureaus needs to expand beyond current levels. Credit Bureau coverage inthe US and UK is 100%.

Credit Scoring:Institutional support for the advocacy of credit scores as a key financialinclusion and credit/trade financing product in Nigeria is critical to thecredit framework. The use of credit scores has also become atrans-border/regional agenda with far reaching opportunities to increase trans-border/regional transactions for MSMEs, especially with the recent AFCTA.

Lenders must increaseinternal capacity to use data and analytics to manage trade / consumer credit.Many lenders/credit providers do not have adequate internal capacity to manageconsumer lending using data and analytics. The use of credit information todetermine reputation can help in many transactions, such as applications forbank loan, insurance, apartment rental, utility, post-paid phone service, etc.Fintechs are already taking over this space.

Collateral registry usagemust increase and all property registries linked to the registry. Morefinancial institutions need to lend on movable assets, and subnationalcollateral registries should be encouraged.

Some Recent Regulatory Reforms and Directives Relevant to theAchievement of Access to Finance Goals

Thefinancial sector has witnessed several regulatory reforms in line with thefocus of the CBN. Some of these include, the cashless policy,

1. Real Sector Financing Strategies: interveningin creativeindustry and facilitating exports.

2. Lower barriers to entry for mobile money wallet toattract more players: Ease in requirements. Telecoms in the mix withsuper agency licenses. Deposit Banks to no longer require prior approval fromthe CBN but notification before offering mobile money wallet services.

3. Boost availability of loanable funds inbanks: set minimum loans to deposit ratio (LDR) requirements to 65% to compelbanks to lend to the real sector; reduced remunerable Standing Deposit Facilityto N2bn from 7.5bn to increase loanable funds and discourage idleness of funds.

4. Consumer ProtectionGuideline: Ensuring increased transparency andaccountability in financial transactions by financial institutions withconsumers.

5. Improve provision offinancial products through issuance ofproduct specific prudential guidelines to increase efficiency and transparencyin mortgage refinancing companies (the CBN also made mortgage chargescompetitive rather than fixed); micro-finance banks; commercial, merchant andnon-interest banks; the guidelines were to eliminate restrictive pricing andpromote competition by allowing market forces to determine pricing.

6. Cross-Bank Loan Servicing:increased transparency and efficiency in tracking loandefaulters and enforcing repayment. Unveil serial industry defaulters.

7. Increased transparency inthe operations of Development Finance Institutions-seekingfull disclosures on subsidiaries.

8. Enhancing digital paymentsservices: intensified efforts to in-crease digital transactions by compellinguse of digital channels for amounts above N500,000 ($1,633) and reduction ofmer-chants service charge rates on electronic transactions from 0.75% to 0.5%;New regulations on electronic payments and collections.

About TheAuthor

Ajibola Alfred is founder and director, Research & Strategy atStraplan Advisory Limited. He is a policyanalyst with over 15 years experience in research and evaluation and strategicplanning roles in private and public institutions in Nigeria. His experiencecovers total quality management, asset management and financial markets,export/trade development finance and commodities markets, project management,public sector reforms and performance management. He recently served as reformleader and technical consultant at the Presidential Enabling BusinessEnvironment (PEBEC) Secretariat between 2017 and 2019.

He also powerswww.jaraja.com.ng, an onlineplatform that seeks to create market access for made-in-Nigeria products bybridging the value-chain and eliminating unproductive middlemen. For more onfinancial infrastructure and access, you can send emails to [email protected] or [email protected] or simplycall +234 803 860 8755 or +234 808 311 3785.

Previous Article by Author

Nigeria'sLong Term Economic Development Strategy: A Primer on Re-Orientation andCoordination

Related News - Doing Business in Nigeria

1. CBi Tasks Operators In Eastern Nigerian Ports,To Actively Engage The PSSP Platform

2. Pres. Buhari Signed EO5 For Devt Of Local Content In Science, Engineering And Technology

3. CBi and MACN Takes the Round-Table Session On "Ports Service Delivery" to Port Harcourt

4. Nigeria Moves Up 15 Places To 131 In World Bank Doing Business Ranking For 2020

5. World Bank Doing Business 2020 Report: Tackling Burdensome Regulation

6. CBI-MACN Roundtable: Stakeholders Call For Increased Awareness of The Maritime PSSP

7. CBi and the Maritime Anticorruption Network to hold Roundtable Session in Abuja on October 22, 2019

8. Azuka Azinge's Two Years As Head of Corporate Affairs Commission (CAC)

9. MACN - CBI and BAAC Discuss Service Delivery At The Nigerian Ports: Emphasise Procedural Compliance

10. Towards A Functional Nigerian Port System - Beyond Ease of Doing Business Executive Order

11. Port Reforms: Why Nigerian Ports Lose Money; Understanding The Economics of Inefficiency and Sleaze

12. CBi and MACN Explain Inefficiency At Nigerian Ports; Corruption Still A Problem

13. Maritime AntiCorruption Network (MACN) to hold Session On Service Delivery at The Nigerian Ports

14. Doing Business 2020 Rankings: Nigeria Named One of The Top 20 Improvers

15. CAC Apologises For The Current Disruption Of Its Online Services; Sets Up CSS Nationwide

16. CAC Makes Changes To Pre And Post-Incorporation Processes On Its Portal

17. PEBEC Engages Stakeholders on Legislative Reforms, Agribusiness and Apapa Gridlock

18. PEBEC Engages NBA Section on Business Law On Provisions In CAM Bill 2018

19. 2nd Annual PEBEC Awards Recognises MDAs, Public and Private Sector Supporter

20. Transmit CAM Bill 2018 For Assent Into Law, Now - Business Community

Related News - Credit Services & Registry

- CRC Credit Bureau Ltd 10th Anniversary Forum Examines Credit Penetration In Nigeria

- UK Financial Conduct Authority Launches Review Of The Credit Information Market

- Investing Under IFRS 9 Regime: Why Credit Ratings Matter For Asset Managers

- CBN Publishes Q1 2019 Credit Conditions Survey Report

- CBN, NJI Hold Workshop for Judges on Collateral Registry

- UK's Financial Conduct Authority: Registering As A Credit Rating Agency Post Brexit

- Dissecting the CBN's Real Sector Support Facility (RSSF) Guidelines

- Demand for Secured Lending for House Purchase Increased in Q2 2018

- A Look at Nigeria's Credit Economy

- What Every Borrower Should Know

- Bank Credit Increases in Q1 2018

- The Impact of Private Sector Credit on Economic Growth in Nigeria

- CBN Publishes Credit Conditions Report for Q1 2018

- Roles Of Consumer Protection And Small Business Access To Credit In Financial Inclusion

- Using Credit Bureaus, Telcos, Discos and Others Can Enhance Ease of Doing Business

- All You Need to Know About Credit Bureaus in Nigeria

- Some Space for Lending Growth Ahead

- ASIC Reports On Credit Rating Agencies, Recommends Changes

- Likely Improvement in Credit Extension Ahead

- Cautious Approach to Credit Extension

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top