Lagos, NG • GMT +1

Lagos, NG • GMT +1

1342 views

1342 views

Wednesday, September29, 2021 / 09:02 AM / FBNQuest Research / Header ImageCredit: FBNQuest

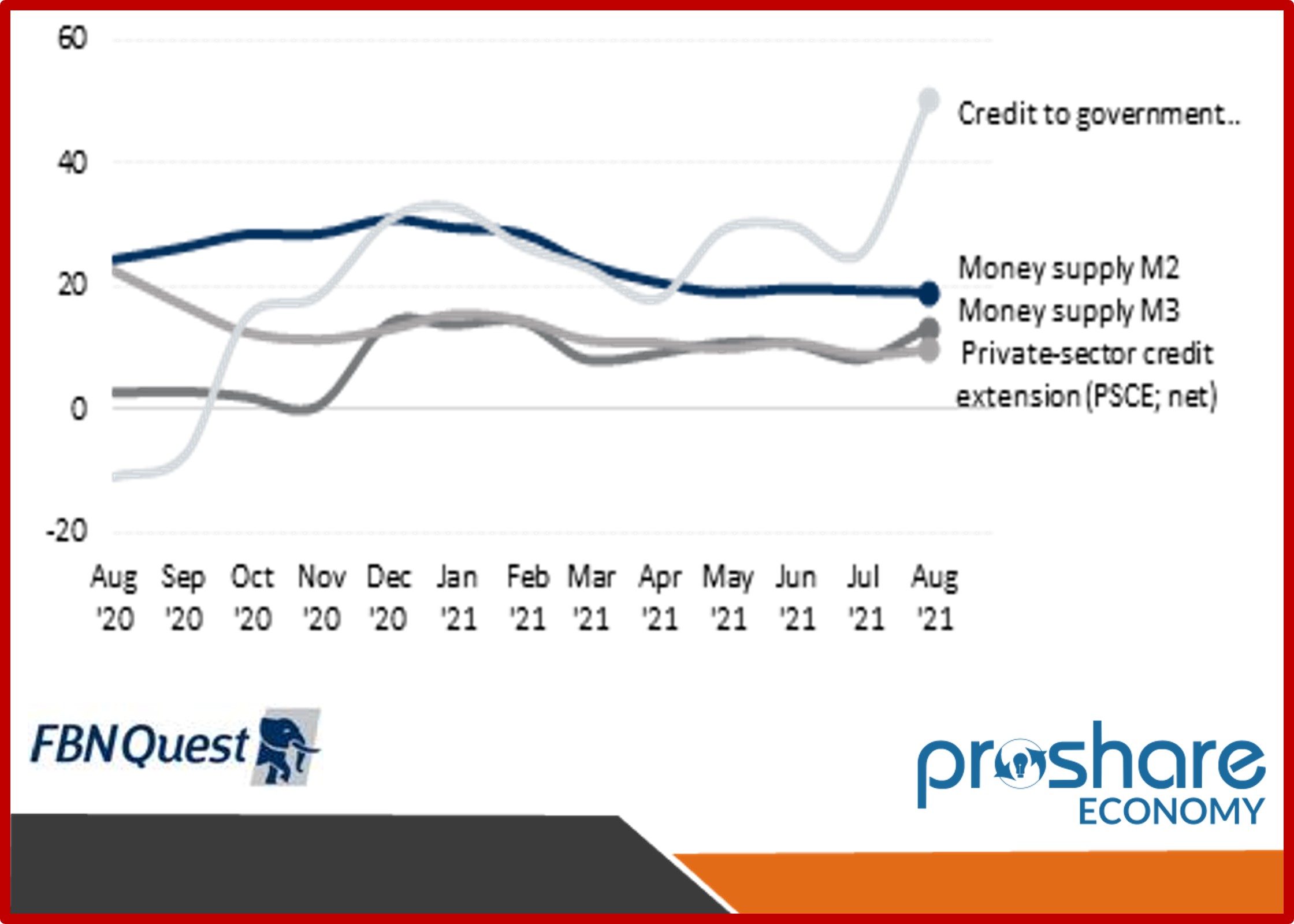

Totallending to the private sector grew by 9.8% y/y in August to NGN33.4trn(USD81.0bn). The trend rate of growth is slowing, however. The data, which isshared in today's chart for private-sector credit extension (PSCE), coverslending from all sources including the CBN and the state-owned developmentbanks. This measure of credit was growing at a treble-digit level y/ythroughout H2 '19 as the CBN twice increased the minimum permittedloans-to-deposits ratio. There is still some distance to travel in terms offinancial intermediation and inclusion when we consider the scale of theunbanked informal economy. Nigeria's PSCE/GDP ratio has picked up to 20.1% inQ1 '21 from 19.1% one year earlier. The comparable figure for Kenya from alllenders in Q4 '20 was 27.0%. The CBN plays a much larger role in lending to thereal economy than its Kenyan counterpart.

TheCBN's Quarterly Statistical Bulletin (QSB) shares another series covering thedistribution of credit by deposit money banks (DMBs). It gives a total ofNGN21.02trn in March 2021, which leaves a large gap exceeding NGN12trn with thefuller CBN measure. There is also a time lag of five months to explain away thedifference.

Anotherreason is the lending by four development finance institutions, led by therecapitalized Bank of Industry. These totalled NGN940bn in aggregate atend-2020 and will continue to grow strongly within the FGN/CBN agenda ofsupplying credit where the DMBs are seen as reluctant to tread.

Thelargest single explanation of the difference between the two measures has to bethe delivery of the CBN's development finance role. The latest communique fromthe monetary policy committee from September listed disbursements of NGN800bnunder the anchor borrowers' programme, NGN710bn under the commercialagriculture credit scheme, NGN1trn under real sector intervention and NGN340bnunder the targeted credit facility (TCF). The programmes other than the TCFwere launched before the pandemic but all have seen an acceleration over thepast 18 months. The communique lists smaller sums disbursed by another six CBNschemes.

Wehave extended our chart to include net credit to government. Its y/y growth hasaccelerated in the past few months, reflecting a combination of the FGN'sexpansionary fiscal stance and the regular underperformance of revenuecollection relative to budget (Good Morning Nigeria, 22 September '21). AnotherCBN publication shows a record FGN deficit of NGN2.5trn in Q1'21.

| Money and credit indicators (% chg; y/y) |

|

|

| Sources: CBN; FBNQuest Capital Research |

Related News on Monetary Policy

- How to Stabilize the Naira - Ayo Teriba

- CBN Communique No. 138 of the MPC Meeting - Sep 16-17, 2021

- September 2021 MPC Meeting: CBN Retains All Policy Parameters

- Pre-MPC Note: Will Status Quo Be Maintained?

- A Winning Formula for MPC Members

- Personal Statements by the MPC Members at the 137 MPC Meeting of July 26-27, 2021

- Single-Digit Growth in PSCE in July 2021

- Post MPC - July 2021: Reactive in Action... Proactive in Guidance

- A Slowdown in Growth in PSCE, Rose by 10.9% in June 2021 to N32.64trn

- CBN Stops Sale of FX to BDCs, Holds Policy Parameters Constant

- CBN Communique No. 137 of the MPC Meeting - July 26-27, 2021

- July 2021 MPC Meeting: CBN Holds All Policy Parameters, Stops Sales of FX to BDCs

- MPC Likely to Hold Rates

- The Rationale for No Change in the MPC's Stance

- Personal Statement of MPC: If It Ain't Broke...

- Personal Statements by the MPC Members at the 136 MPC Meeting of May 24-25, 2021

- Double-Digit Growth in PSCE in May 2021

- System Liquidity in Deficit on Persistent CRR Debits

- Intricacies of Liquidity Management in Nigeria

- Steady Growth in Private Sector Credit Extension in April 2021

- Post-MPC May 2021: Status Quo Justified but Economy Still Shackled

- May 2021 Meeting: Another MPC Decision to Wait and See

- CBN Communique No. 136 of the MPC Meeting - May 24-25, 2021

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top