Lagos, NG • GMT +1

Lagos, NG • GMT +1

356 views

356 views

Tuesday, May 24, 2022 / 08:22 AM / by United Capital Research / Header Image Credit: SME Futures

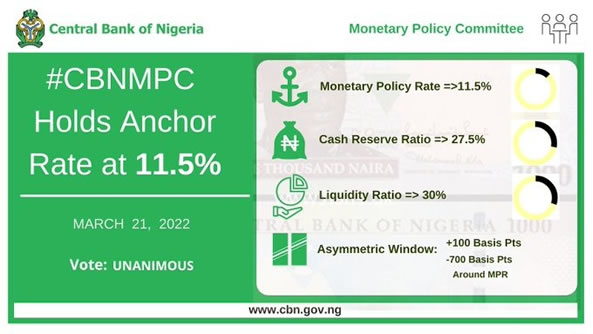

Today, the 285th Monetary Policy Committee (MPC) meeting will be concluded and the CBN Governor will announce the committee’s decision via its usual press briefing. At the meeting, key considerations will include the unabating global hawkish monetary policy stance from major central banks, domestic inflation estimates, economic growth considerations, money supply and interest rate environment.

We believe the appropriate policy decision will be to raise the Monetary Policy Rate (MPR). First, aggregate price level is spiraling out of control, following the 90bps surge in Apr-2022 while inflation is expected to sit pretty outside the CBN’s comfort zone. Also, the CBN’s dovish monetary policy poster boy has been its pro-growth agenda. According to the National Bureau of Statistics (NBS) Q1-2022 GDP report, the economy expanded by 3.1% in real terms. This implies the economy continues to remain strong in the aftermath of the pandemic, eliminating need for further monetary support at least not at the expense of surging inflation. Another consideration is the fast-depreciating naira, reflecting sustained weakness in CBN’s ability to defend the nation’s currency. Looking at the CBN’s alternatives for earning FX, net oil proceeds continue to dwindle, funding via Eurobonds issuance is unlikely given current market conditions while other policies designed to attract FX flows via official channels appear not to be yielding any fruits. This leaves the CBN to consider resuscitating fixed income FPI flows, but at the expense of raising interest rates.

Despite our preference for a hike in policy rate, we note the committee would likely not opt for this approach. Thus far, the CBN governor has argued that inflation has been driven by structural inefficiencies, rather than monetary supply imbalances. However, we think a combination of both factors is at play, evidenced in the fact that broad money supply is up 17.9% y/y at the end of Q1-2022, highest since 2017. In addition, the governor appears to prefer alternative measures to generate FX flows rather than attracting FPI flows which justifiably will be difficult to achieve even with interest rate hikes. Overall, we note the probability of a rate hike is higher than in recent times but reckon the committee may remain biased towards a HOLD stance with a focus on accommodative borrowing rates.

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top{kind=link}