Lagos, NG • GMT +1

Lagos, NG • GMT +1

480 views

480 views

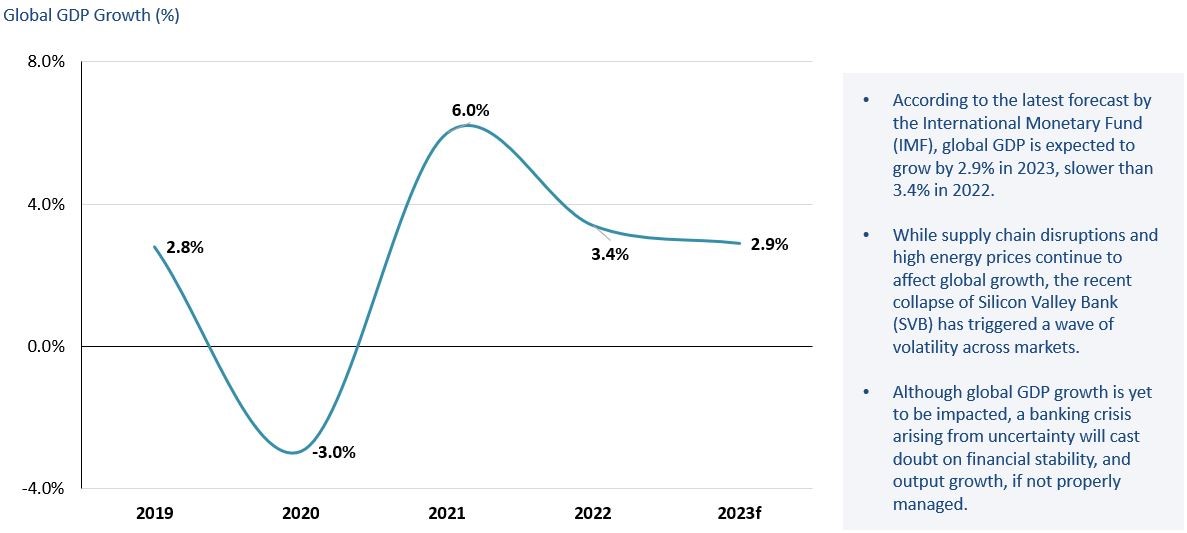

Review of the Global Economy

The collapse of Silicon Valley Bank creates a new global risk to growth

Data Source: International Monetary Fund (IMF)

Analyst Views on the Global Economy

• The need to tame inflation will be a major policy focus for many central banks and governments. However, we believe that this need will be balanced by the goal to support output growth, hence some countries will either slowdown the pace of rate hikes or begin to reduce rates in coming quarters.

• For Central Banks it is a balancing act between addressing price stability and ensuring financial stability. Both ECB and the FED hiked rates as control of inflation remains the priority even with the unfolding bank crisis.

• The collapse of SVB has raised a number of issues for the US banking system and the global financial industry:

• First, the pace at which Central Banks raise rates to tame inflation could present some risks to the financial system. Central banks may need to increase rates at a slower pace to allow the system to adjust to the new realities. In view of this, the US Fed could slowdown its rate hikes at least in the short term.

• Second, banking regulations and the role of Central Banks as a watchdog must be strengthened to ensure complete oversight of the financial sector.

• Third, Central Banks, at frequent intervals, must examine the impact of its actions (especially raising rates) on the risks level and governance of financial institutions.

• Still on the collapse of SVB, there is a possibility of contagion to the financial system and the real economy especially in view of the slowdown in real output and high inflation that have plagued the US economy. Where customers are not assured of the soundness of the financial system, this could trigger bank runs and have grave effects on the financial system.

• In Europe, there were contagion fears over the state of Credit Suisse Group AG and this was reflected across European markets. As at March 17, the European Stoxx 600 banks index had lost another 2.6 per cent, and was down 15 per cent for the week, according to Financial Times. It was announced that the Swiss Bank, UBS, will take over Credit Suisse, with assurances from the Swiss Central Bank to provide liquidity to the merged bank.

• In an already fragile global economic environment driven by high inflation and weak growth, a global financial crisis will leave a huge dent on households, businesses and economies across countries. While regulators have rapidly intervened to provide liquidity to ailing banks and assure customers and investors there is likely to be a tightening of financial conditions and resultant credit crunch in some economies that may lead to dampening of growth.

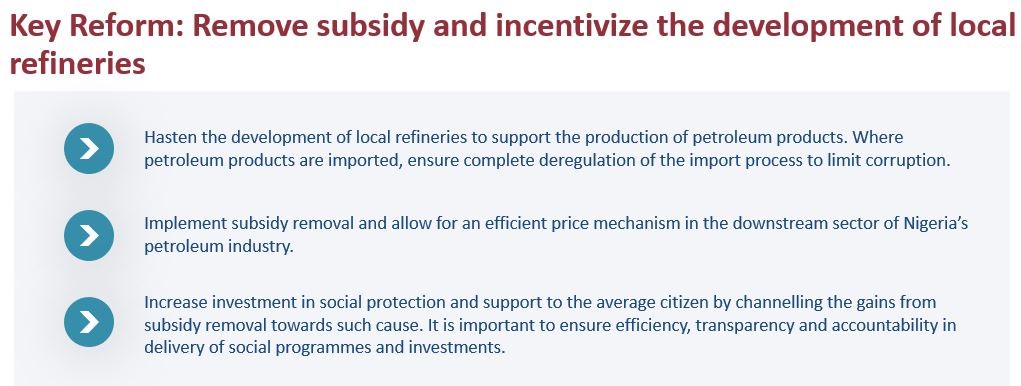

• While the role of regulators in ensuring a sound financial system is important, internal governance systems of banks and financial institutions are equally crucial. Financial institutions and regulators in Nigeria need to evaluate the soundness of financial institutions in the country. With the bearish reception from the oil market, the government needs to plan for the impact of a drop in oil price below the budget benchmark for the remaining quarters of 2023.

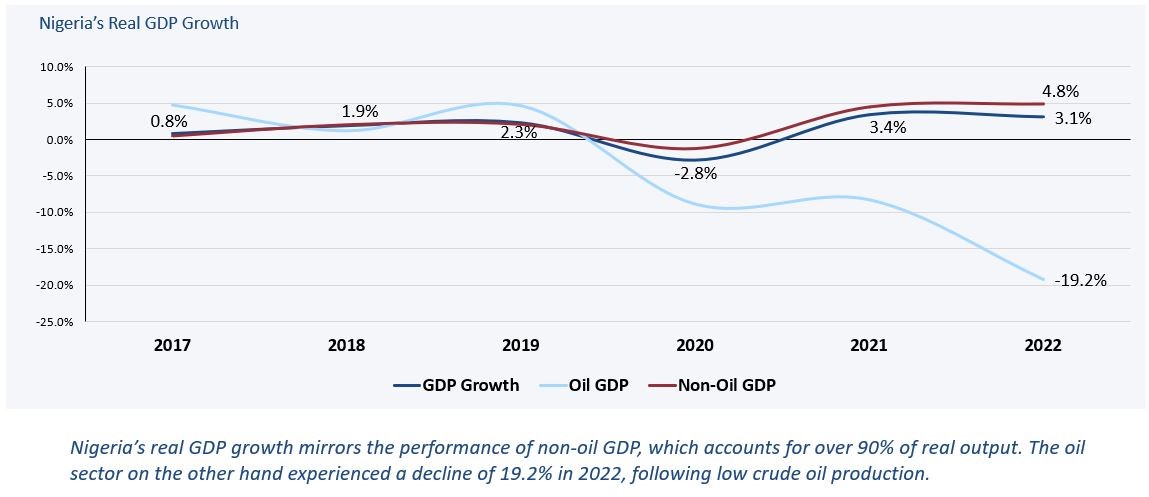

Nigeria's Macroeconomic Environment

In 2022, Nigeria’s GDP grew by 3.1%, lower than 3.4% in 2021

Data Source: National Bureau of Statistics

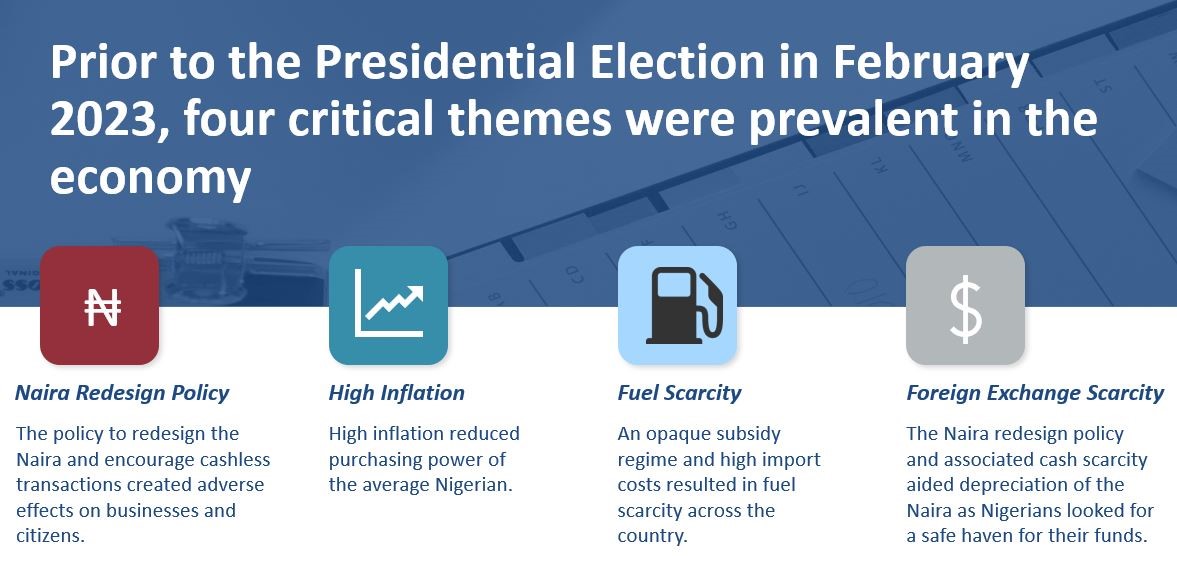

The Demonetisation Policy created undue pressure on banks and citizens

Poorly executed Naira redesign policy led to a cash crunch across Nigeria

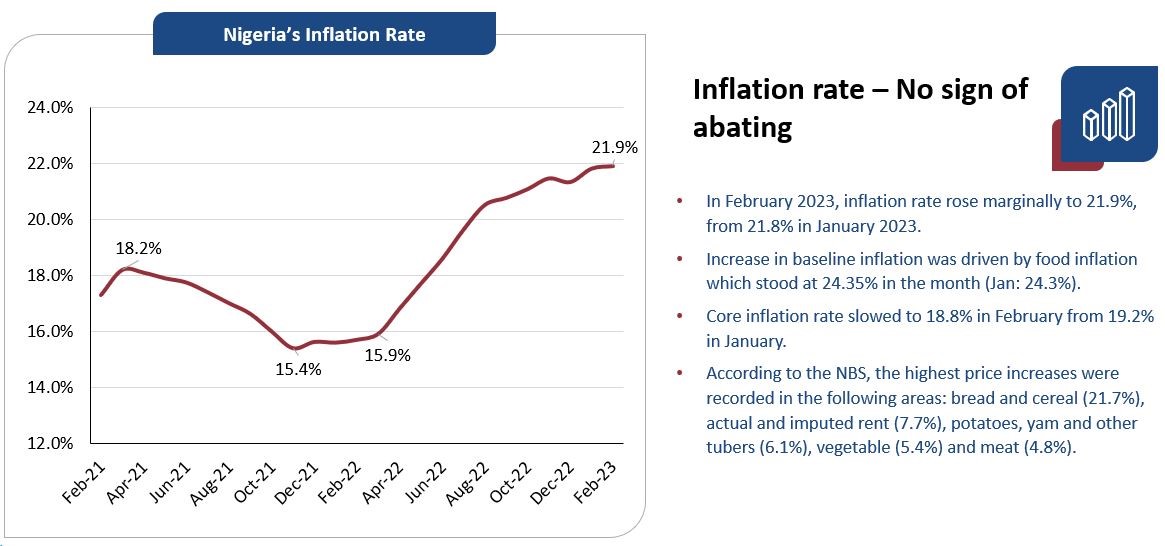

High Inflation persists amidst Naira scarcity

Data Source: National Bureau of Statistics

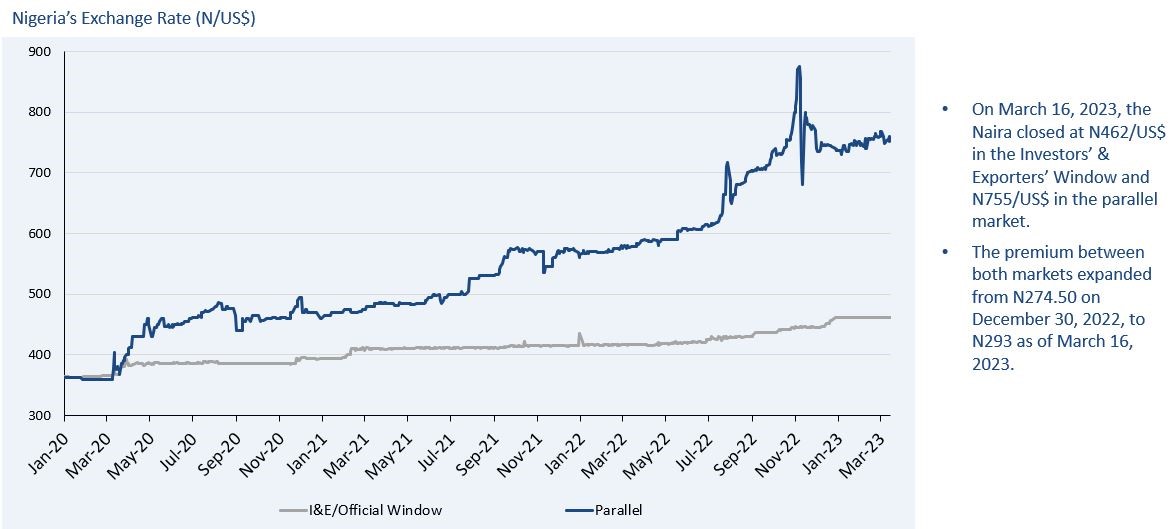

Exchange rate volatility intensifies, slightly motivated by the scarcity of cash

Data Source: FMDQ, (Parallel Market Rate updated from daily reports from Nairametrics)

Analyst Views on GDP Growth, Inflation and FX

• As noted by major forecasts, Nigeria’s GDP growth in 2023 will be lower than that of 2022. The deceleration of growth will stem from the impact of the Naira scarcity on aggregate demand, uncertainties about the new administration and existing structural problems. In terms of the growth drivers, the services sector led by trade, ICT and finance will play a major role.

• Since our last Macroeconomic Review, Nigeria’s oil production has been trending upwards. Oil production increased from 1.27 million barrel per day (mbpd) in December 2022 to 1.38 mbpd in February 2023. While this is a significant improvement, oil production is still below the budget benchmark of 1.69 mbpd. The government must continue efforts to curb oil theft and vandalism to ensure oil sales are reflected in government account.

• We expect inflation rate to remain high but fall gradually in 2023. This expectation is driven by the Naira scarcity which has suppressed demand for goods and services in the country. Upside risks are, however, still prevalent – infrastructure deficit, insecurity, exchange rate depreciation and poor power supply.

• For exchange rate, we expect a slow and steady depreciation as experienced in recent years. The currency will continue to face pressure from high import costs and demand for foreign currency for services but the CBN will continue to intervene in the FX market to limit the pace of depreciation. The possibility for crucial exchange rate reform in H1 2023 is limited and such reform can only happen in the second half of 2023 on the insistence of a new President. Currently at US$36 billion, external reserves which can finance about 6-7 of imports of goods and services will also face pressure in 2023.

Analyst Views on Naira Redesign Policy/Cash Crunch

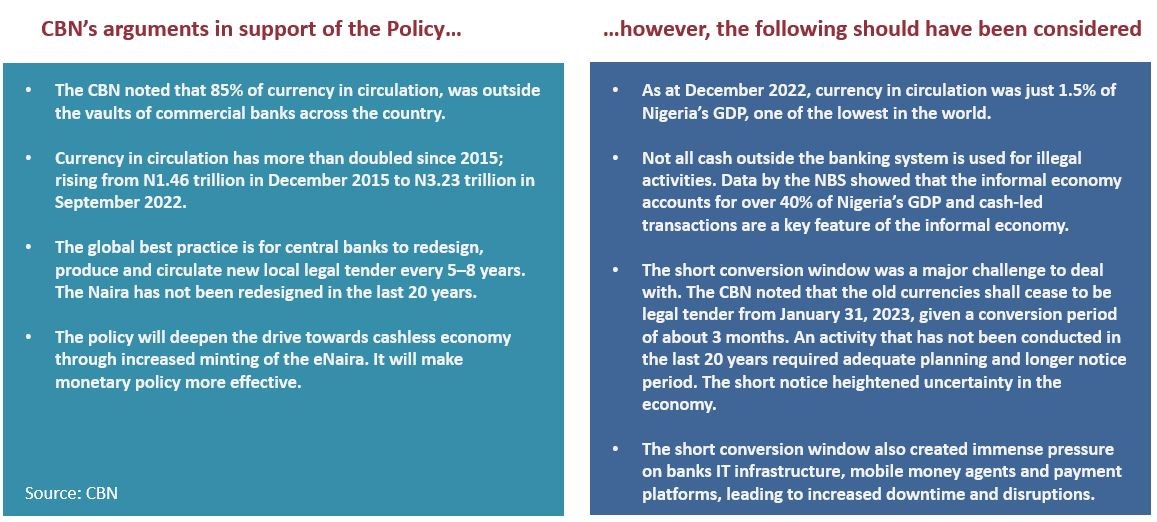

• The impact of the Naira Redesign policy has been profound for the economy and will be the major determinant of Nigeria’s economic trajectory in 2023. The associated cash crunch has led to increased pressure on the banking system, and on the financial system’s digital infrastructure. It has also resulted in the disruption of economic activities, created social tensions and distorted the trajectory of the economy. With a large informal economy that relies on cash, it will affect trade and other sectors as transacting becomes constricted. The extent of the distortion and how fast the economy recovers will depend on CBN’s ability to re-supply the old notes to alleviate the cash scarcity.

• The banking sector suffered severe loss of trust and confidence as a result of the policy. The inability of the banking system to facilitate the distribution of new notes and the scarcity of cash has depleted the trust and confidence in the banking sector by many Nigerians. Going forward, the banking public, particularly those in the informal sector, are more likely to withdraw cash from the banks and resort to the traditional means of keeping cash at homes. This will slow down efforts of financial inclusion.

• The involvement of the judiciary in the Naira redesign policy undermines the institutional independence of the CBN. Following the economic hardship emanating from the policy and ensuing litigations, the Supreme Court gave an interim injunction restraining the CBN from implementing its February 10 deadline and later ordered the immediate recirculation of the old naira notes. The intervention of the Supreme Court in the policy erodes the independence of the CBN on monetary policy. This is not a good occurrence for monetary policy in Nigeria and could be the start of judicial interference on monetary policy issues in Nigeria.

Analyst Views and Outlook on Monetary Policy

• Monetary tightening will persist for as long as inflationary pressures are not subsiding and central banks in advanced countries remain hawkish. The CBN continues to base MPC decisions substantially on inflationary pressures. Still, the continued increase in policy rates in 2023Q1 in several advanced countries further strengthens the need for high interest rate in Nigeria to prevent massive capital outflows. Coupled with issues such as Moody’s downgrade of Nigeria’s rating, the FGN borrowing need, limited Forex inflows and capital flight, the interest environment needs to be high to sustain and attract portfolio investment.

• Rising interest rates will have implications for Nigeria’s fragile growth. While inflationary pressures persist, continuous increases in interest rates will limit the ability of the financial system to provide funds for businesses. Besides, it will constrain business operations as lending rate approaches 30%.

• Given the structural characteristics of Nigeria’s inflation, a holistic approach is required. Recent inflationary pressures in Nigeria are largely motivated by structural constraints that inhibit the supply chain, such as infrastructure and logistic deficiency, insecurity, and regulatory bottleneck. Even the CBN, at some point, acknowledged that Nigeria’s inflation drivers are not entirely monetary factors. Hence, non-monetary authorities have a substantial role in tackling inflation by eliminating the hurdles in the supply chain.

• We do not expect any downward movement in MPR in 2023H1. This is on the back of amplified inflationary pressure, despite the constraints brought about by the Naira scarcity, the government borrowing needs and trend of rates in the global market. In addition, the MPC noted that factors such as future fuel subsidy removal and exchange rate pressures could drive up inflation in coming quarters. Thus, monetary policy rate will remain high to limit price increase.

Analyst Views and Outlook on Fiscal Policy

• The elections, as expected, will impact fiscal policy performance over the first quarter of 2023. Non-election fiscal spending is expected to slow but will increase after the elections. As noted by the Debt Management Office, it has, so far, raised N2.13 trillion in January and February 2023, of which N1 trillion has been deployed to budget financing (the remaining used for refinancing of existing debt).

• Fiscal sustainability is still a major source of concern. As seen in the 2023 budget, the projected fiscal deficit is 51.9% of total expenditure, exceeding the revenue projection. More so, based on 2022 (Jan - Nov) performance, over 40% of government spending went into debt service against a projected 22.1%, while other aspects of public finance suffered underfunding. The situation will likely continue in 2023, following the uncertainty from the elections, Naira scarcity, and other challenges that limited revenue generation from taxes.

• Moody’s rating downgrade truncates the viability of diversifying the government’s finances. Moody's downgraded Nigeria's ratings to Caa1 with a stable outlook from the previous rating of B3. This is on the back of worsening government fiscal and debt position and institutional weakness. Meanwhile, the government has identified external borrowing alongside multi-lateral/bi-lateral project-tied loans as a major source of financing its deficit. Moody’s downgrade will disincentivise investors, constraining the government to the domestic capital market.

• Indefinite expansion of fiscal deficit needs to be checked. While the problem of revenue is well established, the unabated expansion of fiscal deficit, relying ultimately on borrowing, needs to be checked as it comes with new debt obligations. A good news, however, is the increase in oil production in the first two months of 2023, which could raise revenue from crude oil sales in the period. Such production needs to be sustained while the government intensifies effort to raise non-oil revenue.

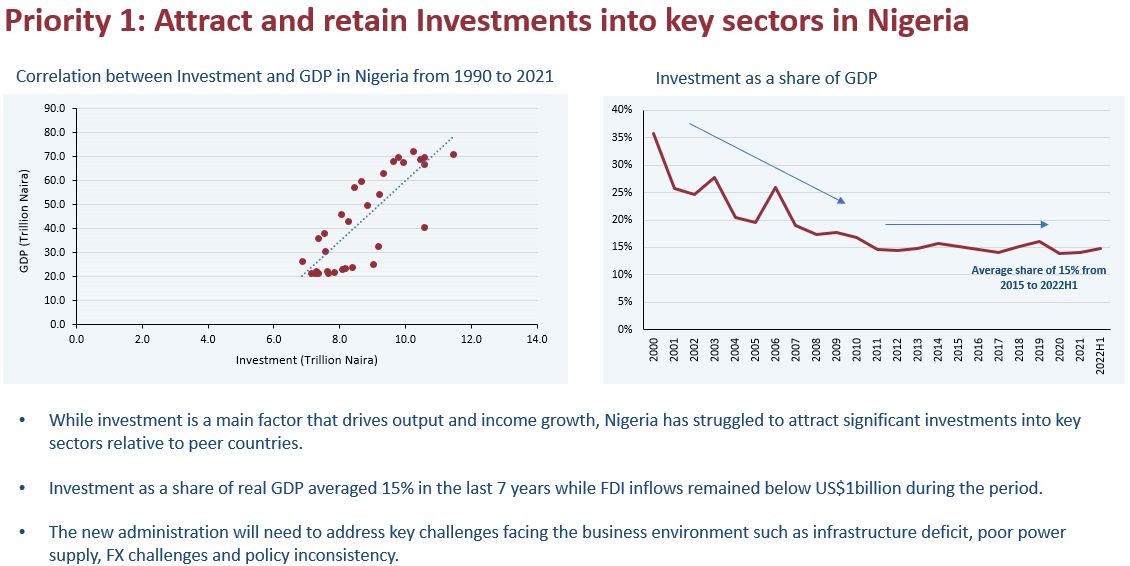

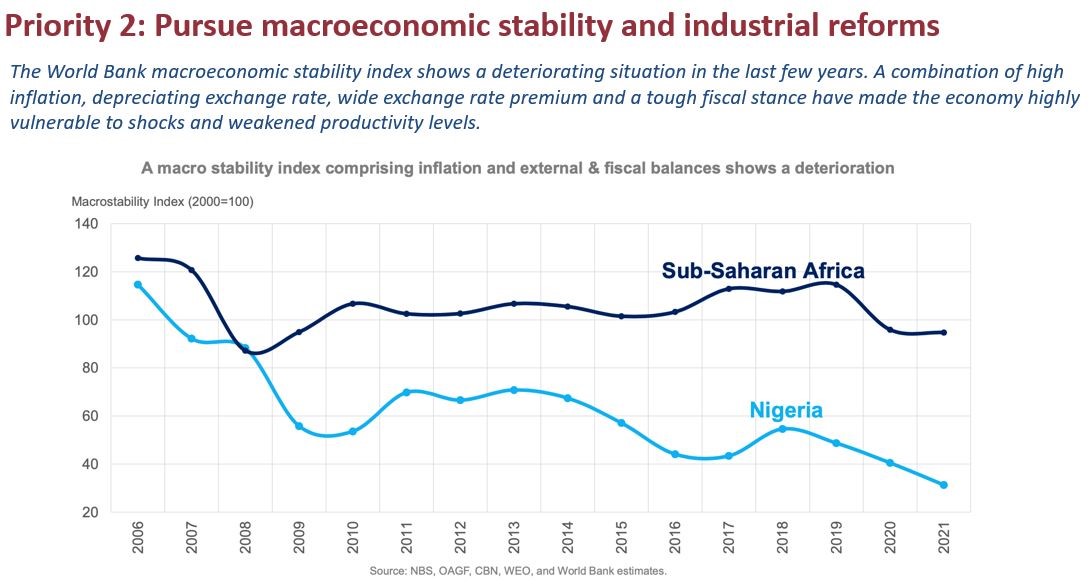

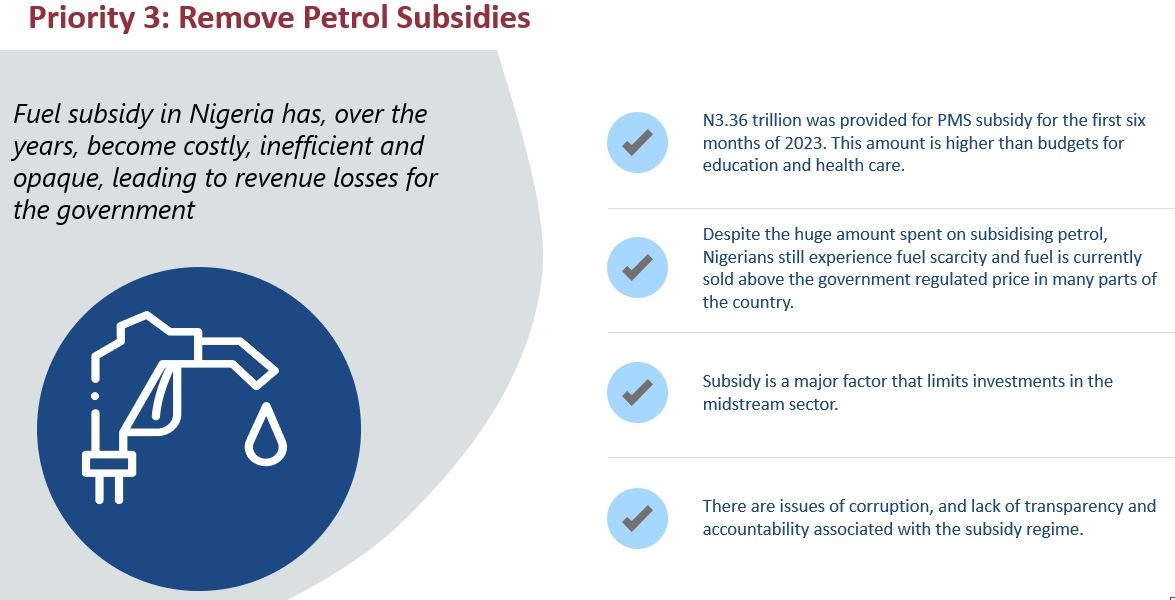

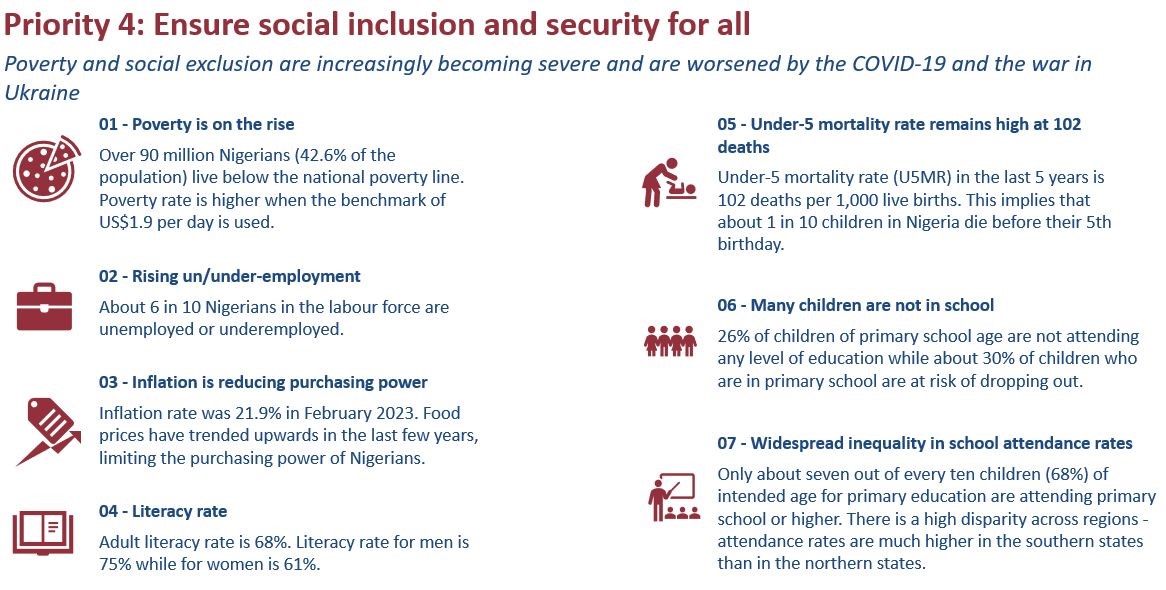

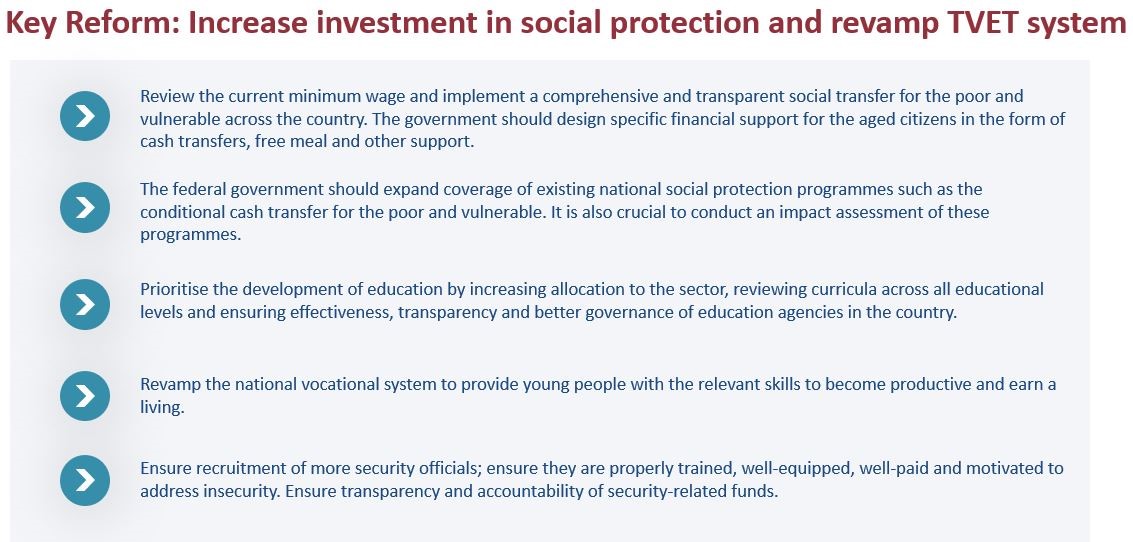

Four Key Priorities for the President-Elect to Tackle

Data Source: Central Bank of Nigeria and National Bureau of Statistics

Data Source: Ministry of Finance, Budget and National Planning

Data Source: National Bureau of Statistics and World Bank

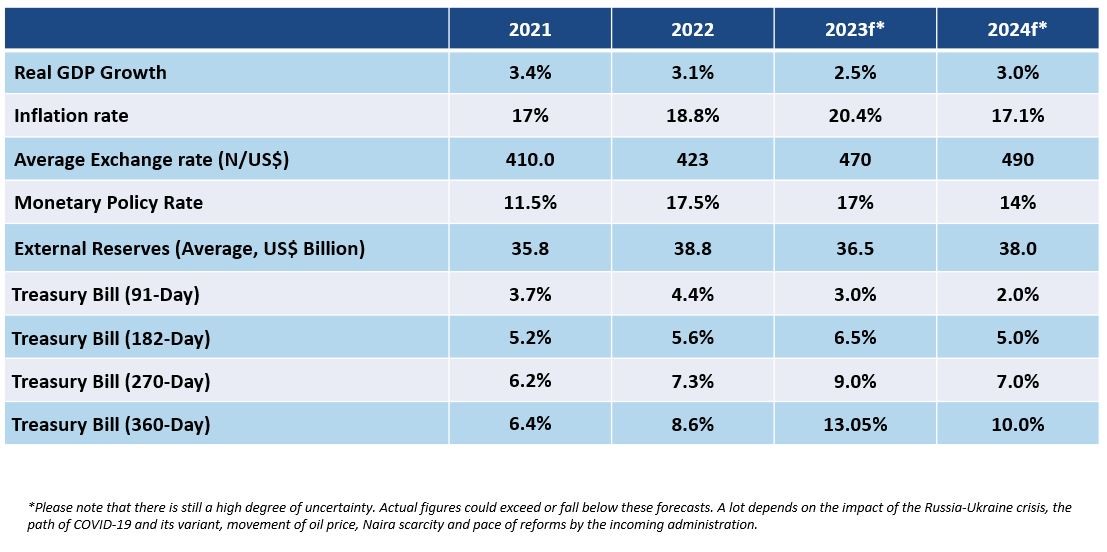

Macroeconomic Projection for 2023 - 2024 for Nigeria

Download Full PDF Report Here

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top