Lagos, NG • GMT +1

Lagos, NG • GMT +1

220 views

220 views

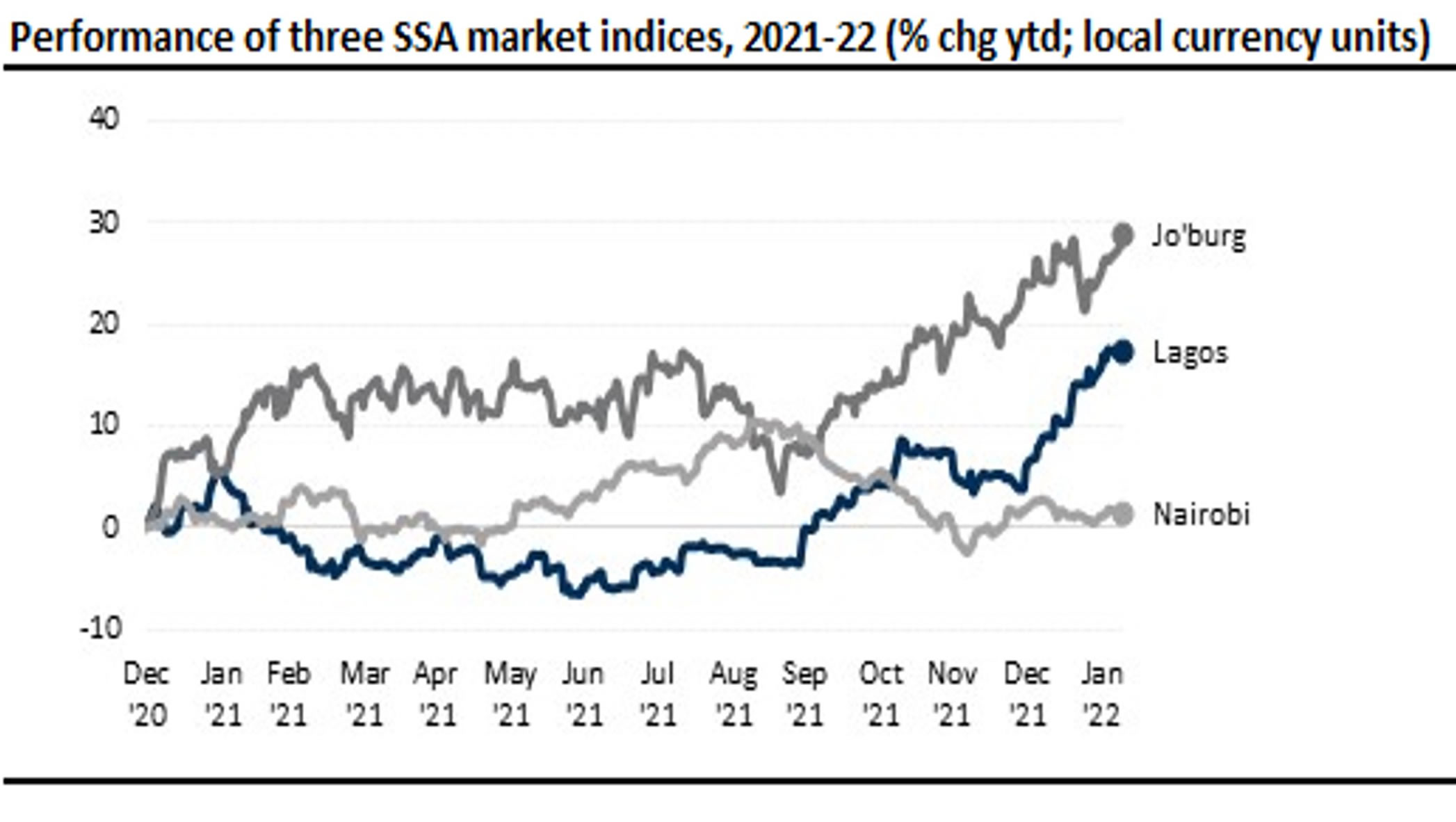

Today, we focus on the performance of the Nigeria’s Stock Exchange (NGX ASI) in recent weeks. The performance of the Lagos bourse has moderated after a stellar first half of 2022. As of end-August, the NSE’s year-to-date (ytd) return had moderated to c.16.7%, a sizable decline from the peak levels of c.26.6% it attained at the end of May. As seen in our chart below, the NGX has declined every month since May, shedding, -3.4%, and -2.8% m/m in June and July respectively. Its latest return for August was a slightly more modest decline of -1.1%. This compares with a -2.4% return for the Johannesburg (Joburg) exchange. In contrast, the NSE 20, our proxy for the Nairobi exchange, recovered some lost ground, gaining 2.9% in August.

Despite the change in fortunes of the NGX’s m/m performance in recent months, its ytd return is still comfortably ahead of those of its two counterparts, both of which are treading water. Notably, Joburg, its larger rival, is down -8.8% ytd, while Nairobi has not fared much better with a ytd return of -8.0%.

The performance of the NGX in H1 '22 was aided by the rising share prices of bellwether stocks, which are represented in vital sectors including cement, telecommunications, and FMCG.

The rally in crude oil prices for most of this year, driven by demand-supply imbalances brought on by the conflict in Ukraine also caused a surge in oil and gas names like Seplat Energy (Seplat) and Total Nigeria.

As such, the underlying driver of the recent downturn on the NGX has been sell-offs in many bellwether names, largely due to profit taking by investors, combined with a change in investor sentiments. Additionally, the recent drop in crude oil prices has sparked a sell-off in oil and gas shares like Seplat.

Although a few listed companies have reported strong earnings growth for Q2 ’22, the results have been broadly mixed. As such, Q2 earnings have not served as a catalyst for the market.

Following monetary tightening by the central bank, domestic bond yields have risen by roughly 200bps since April.

Going forward, we continue to see a more subdued performance for equities for the balance of the year, due to elevated yields on the fixed income market, and risk-off sentiments by investors as the 2023 presidential elections draw closer.

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top