Lagos, NG • GMT +1

Lagos, NG • GMT +1

1182 views

1182 views

Wednesday, April 28,2021 / 10:04 AM / by Coronation Research / Header ImageCredit: Coronation

Since the beginning of the year fixed income yields have beenrising. Yet the movement in rates has been unequal across durations. Long-termbond rates have risen sharply and so too have 1-year T-bill rates at auction.But short-term T-bill rates have stayed low.

FX

Last week the exchange rate in the Investors and Exporters Window(I&E Window) strengthened by 0.24% to close at N410.00/US$1. In theparallel, or street market, the Naira weakened by 0.62% to close atN485.00/US$1. The gap between the two markets is 18%. There was slight, 0.08%,fall in the level of the CBN's FX reserves to US$35.12bn, though this levelappears quite reassuring to the market, especially in the context of theability of the Federal Republic of Nigeria (FGN) to make a substantial Eurobondissue, which it intends to do. There is not the sense urgency now that existedin February, when the I&E Window rate last shifted in the direction of theparallel rate. But without such shifts we doubt that liquidity in the I&EWindow and NAFEX markets will pick up meaningfully. Over a period of months, webelieve that there will be continued pressure on the I&E and NAFEX rates

Bonds & T-bills

Last week, the secondary market yield for a FGN Naira-denominatedbond with 10 years to maturity rose by 53bps to 12.70% and at 7 years rose by26bps to 12.43% while at 3 years the yield contracted by 3bps to 9.92%.Activity in the market was typically low given that the FGN bond auction tookcentre stage. After the auction bearish sentiment was characteristic. Given marketsentiment, our sense is that the bear run in bonds is likely to continue for awhile.

The Debt Management Office (DMO) offered for subscription FGN bondson 21 April 2021, reopening the March 2027, March 2035, and July 2045 issues. Atotal of N265.68bn (US$648.05m) worth of bonds were bid for against N150bn(US$365.85m) offered and N157.95bn (US$385.24m) worth of bonds were allotted.

The annualized yield on a 342-day T-bill fell by 1bp to 8.06%, andthe yield on a 326-day OMO bill declined by 2bps to 9.12%. The CBN's OMOauction of N20.00bn managed to sell N12.84bn of the total offer and had stoprates for the 96-day note at 6.90%, 187- day note at 8.48% & 355-day noteat 10.10%. We expect a T-bill auction on Wednesday this week and, given thesteady upward movement in 1-year T-bill stop rates, it wouldn't surprise us tosee 1-year yields reach or even pass 10.00% though, based on experience so farthis year, yields on short-dated paper may not increase.

Oil

The price of Brent crude dropped by 0.99% last week, closing atUS$66.11/bbl, a 27.63% increase year-to-date. The average price to year-to-dateis US$62.02/bbl, 43.52% higher than the average of US$43.22/bblin 2020. Newsearly in the week about the continued increase of Covid-19 cases in India andJapan were offset by bullish economic data from the US and Europe. Later thisweek the Organization of the Petroleum Exporting Countries and its ally Russia(OPEC+) meet, and their decision on the duration of current production cuts islikely to influence the market strongly. In general, OPEC+ appears to haveshifted its position on the ideal level of prices, with prices well aboveUS$60.00/bblnot causing disagreements (even though this encourages US shaleproduction). Our sense is that prices remain supported at US$60.00/bblover thecoming weeks

Equities

The Nigerian Stock Exchange All-Share Index (NSE-ASI) rose by 1.27%last week bringing the loss year to date to 2.41%. PZ Cussons +21.11%,Honeywell Flour Mills +17.65%, and Sterling Bank +8.78% closed positive lastweek, while Guinness Nigeria - 9.89%, Fidelity Bank -7.08%, and Cadbury Nigeria-3.70% closed negative. Performance across sectors was broadly positive as theNSE-Industrial index was the highest gainer for the week with +4.82% while NSE-30advanced by +1.64%, NSE Consumer Goods by +1.05%, NSE Insurance by +0.40% , andNSE Oil & Gas by +0.29%.

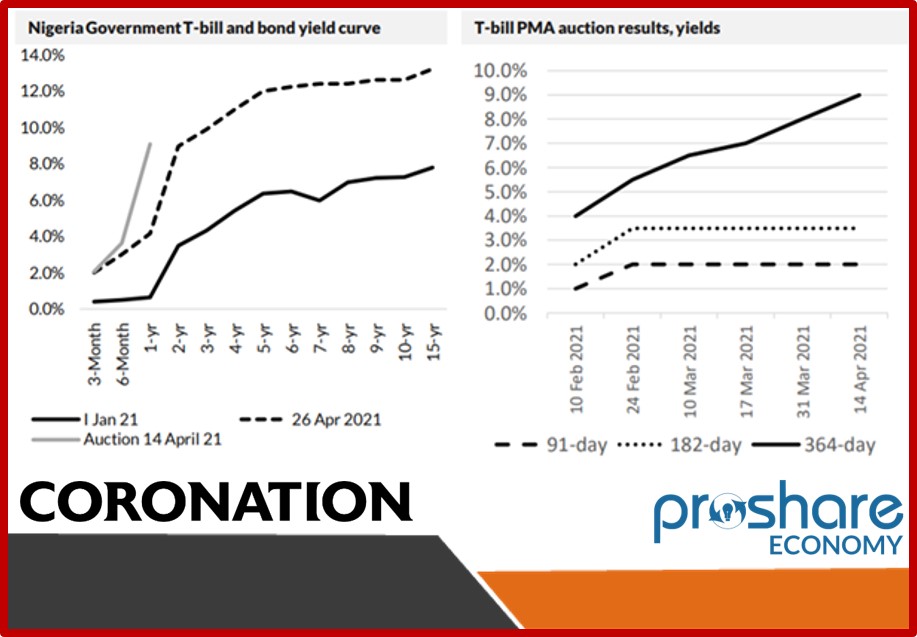

The Strange Yield Curve

The past month has seen a rout in the bond market, with prices ofFederal Government of Nigeria (FGN) bonds falling heavily. The average yield of10 FGN bonds which we track, with durations of between two and 15 years, hasincreased by 216 basis points (bps) over the past month, and by 561bps sincethe beginning of the year. This is bad news if you are required to mark bondpositions to their market price, but good news if you are considering a futurepurchase of a bond, although it has to be said that, so far, no FGN bond yieldcomes close to matching the rate of inflation at 18.17% year-on-year (inMarch).

What about Nigerian Treasury Bills (T-bills), with duration of upto one year? Most of the action takes place in the Debt Management Office'sPrimary Market Auctions (PMA), which are held two or three times per month.Here the rates on 1-year (or 364-day) paper have been moving up at successiveauctions, with rates actually matching those of 2-yr FGN bonds.

However, while the rates on 364-day T-bills in the PMA have beenmoving up, those on 91-day and 182-day T-bills have stagnated since the ofFebruary. In part this is due to the fact that the short-term market is seen asseparate from the 364-day market and the FGN bond market. And there are someprofound effects.

One is that it is difficult for Money Market Funds, whichconstitute the largest class of Mutual Fund (or Collective Investment Scheme)to generate yields close to 364-day yields, given that they must hold aproportion of their funds under management in short-term money marketinvestments. Retail savers who access the market through Money Market Funds arenot getting the full benefit of rising rates, so far.

Naturally, this is good news for banks, since the fundamentalbusiness of banking is to take short-term liabilities (mainly deposits) and tocreate, or buy, long-term investments. To have such a large gap between 91-dayand 182-day T-bills on the one hand and 364-days T-bills on the other is helpful.Preferred clients can be offered deposit rates well above short-term moneymarket rates.

The question arises as to how long this situation can last. Theparadox of this year's rise in market interest rates is that it is taking placewhile there is still quite a lot of institutional and corporate liquidityaround, so it does not seem likely that liquidity conditions will force upshort-term rates soon. Therefore, this situation may last a while yet.

ModelEquity Portfolio

Last week the Model Equity Portfolio rose by 1.46% compared with arise in the Nigerian Stock Exchange All-Share Index (NSE-ASI) of 1.27%,therefore outperforming it by 19 basis points. Year to date it has lost 1.17%against a loss in the NSE-ASI of 2.41%, outperforming it by 124bps.

Maintaining our conviction in Stanbic IBTC paid off as our notionaloverweight position (5.0% versus the index weight of 2.7%) delivered 41bps.(This notional position caused us some concerns a few weeks ago, but we stuckwith it.) Our notional overweight position in GT Bank (7.9% versus the indexweight of 4.8%) delivered 53bps. Our newly neutral notional position in MTNNigeria (we spent the weeks of the 26 March and 6 April restoring it from anunderweight to a neutral, as we forewarned before the Easter break) earned22bps.

What do we do now? We will deploy a little more of our cash intoour bank positions, reducing our notional cash position by between two andthree percentage points this week. We will look for opportunities among the insurancestocks and report back.

Relatedto Coronation

1. NairaBonds Sell-Off, US Bonds Rise

4. MonetaryPolicy Rate Decision

5. Inflationand Interest Rates

6. The US 10-Year Bond andNigeria

7. T-Bill Rates HeadingTowards 10.0%

8. Q42020 GDP and the Implications for Markets

9. Eurobondsand Foreign Financing

11. NigerianGDP Better Than Thought

14. Interest Rates on the Rise

15. Oil Above US$50.00 per Barrel

18. CBN Likely to Leave MPR at 11.50%

19. Second-best Equity Market in the World

20. TheBiden Effect

21. US Dollar Eurobond Yields Now HigherThan Naira Yields?

22. Fiscal and Monetary Response toEvents

23. Winners and Losers in Africa

24. The Return of the Equity Market

25. Which Way for Interest Rates?

26. Coronation Research Releases Report Themed: From Savings toMutual Funds

27. A Case of Eurobond MarketContagion

29. The Policy Mix and The Markets

30. The Oil Price and ProductionParadox

31. Cracks In The Bond Market?

32. No Big Change in FX Policy

33. Coronation Research Releases Outlook for Insurance Sector -From Lagoon To The Blue Ocean

34. Micro-Insurance, Tech, Key toDeepening Nigeria's Insurance Sector - Coronation Research

35. Navigating the Capital Market:The Investors' Dilemma

36. Market Interest Rates Back Up- Coronation Research

Related News

1. Hotels - A Peep intoPerformance

2. Hospitality: COVID-19Related Policy Shifts

3. Planning for400million: Nigeria's Opportunities and Challenges - 2050

4. Hospitality Before andAfter - The Unmaking of Hotels

5. Hospitality: APost-COVID-19 Reality

6. HospitalityPost-COVID-19: Making the Future Count

7. BOFIA 2020: Impact onthe Financial Services Industry

8. A Case for the FGN'sReform to Focus on Household Income Growth

9. Inflation Rate: The 18.17%Rise of a Monster

10. Economic Recovery isGaining Momentum Globally - Comercio March 2021 Report

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top