Lagos, NG • GMT +1

Lagos, NG • GMT +1

1257 views

1257 views

Monday May 23, 2022 / 12:37 PM / by The Analyst, Personal Finance / Header Image Credit: POWEREXLIMITED

After Nigeria's independence in 1960, the economic clime represented by the waterfront of Marina in Lagos was dotted by more insurance companies than others including banks up till the 70s. Just walking down the boulevard at lunch time, one could easily distinguish the workers from the insurance companies amongst others and young graduates simply desired to be part of this new world.

On Marina, Royal Exchange Assurance Nigeria (REAN) had its imposing structure, then came United Nigeria Insurance Company (UNIC), African Prudential Insurance Company (APICO), African Alliance Insurance (AA) and later National Insurance Company of Nigeria (NICON), which became home to most insurance professionals evident in its 17-storey edifice. Through the 1976 indigenisation process, the Federal Government through NICON acquired Yorkshire Insurance Company and changed the name to Niger Insurance Company, with presence also on Marina, and it became easily reckoned with by customers of insurance alongside other leading players in the Nigerian market.

Under the leadership of the respected CEO, Alhaji Bala Zakariyau who later became Chairman, Niger Insurance excelled and later became publicly quoted in 1989 following the privatisation policy of the Federal Government, whilst expanding its reach to all major cities in Nigeria. The presence of Niger Insurance was best described by its blue buildings everywhere in Nigeria, and from where it served the interests of its policyholders according to their needs.

Today, Niger Insurance Plc probably still leads other insurance companies in Nigeria, in terms of the buildings held including its multipurpose state-of-the-art edifice located in Central Business District of Abuja valued at tens of billions of Naira.

However, quite coincidentally, the same Niger Insurance Plc has been in a financially debilitating state over the last 5-7 years, evident from its annual financial statements and reported cases of non-payment of claims. This culminated, first, in its suspension and expulsion by the Nigeria Insurers Association (NIA) in 2021 for not abiding to their ethos and failure to honour claims obligations to policyholders, then recently, the issuance of Notice of Withdrawal of Licence by the Regulator, National Insurance Commission (NAICOM).

The case of Niger Insurance Plc comes after other giants, like it, in the insurance industry in Nigeria, had been brought on their knees, killed and buried. UNIC, which became a member of the business empire of Late Chief Ernest Shonekan, had its operating licence withdrawn by NAICOM last year. NICON Insurance, once Nigeria's leading light in the insurance industry, has been embroiled in protracted legal issues over its ownership and seemingly inoperative though still retains its operating licence. The case of Industrial and General Insurance Plc (IGI) is also reportedly stalemated by Boardroom wranglings.

How Did the Mighty Fall?

News of the failing state of Niger Insurance Plc may have become noticed in 2016 when claimants started reaching out to insurance professionals and lawyers to assist them pursue their claims with the Company. In most cases, complaints had been lodged with NAICOM but no responses had been received and the claimants got even more worried. For some, the long wait had just started.

Then, with the announcement of the new capital requirement for insurance companies by NAICOM in June 2018, Niger Insurance Plc, like other players, got into the fray to meet the stipulated capital base for composite insurers, by announcing its intention to sell some of her properties towards meeting the new capital base of N18b for Composite Insurance Companies.

While subsequent news reports stated that the Company had a new CEO, Mr. Edwin Igbiti, former CEO of AIICO Insurance Plc, the complaints of claimants had now flooded the social media with little or no response from Niger Insurance Plc as 2019 was ending.

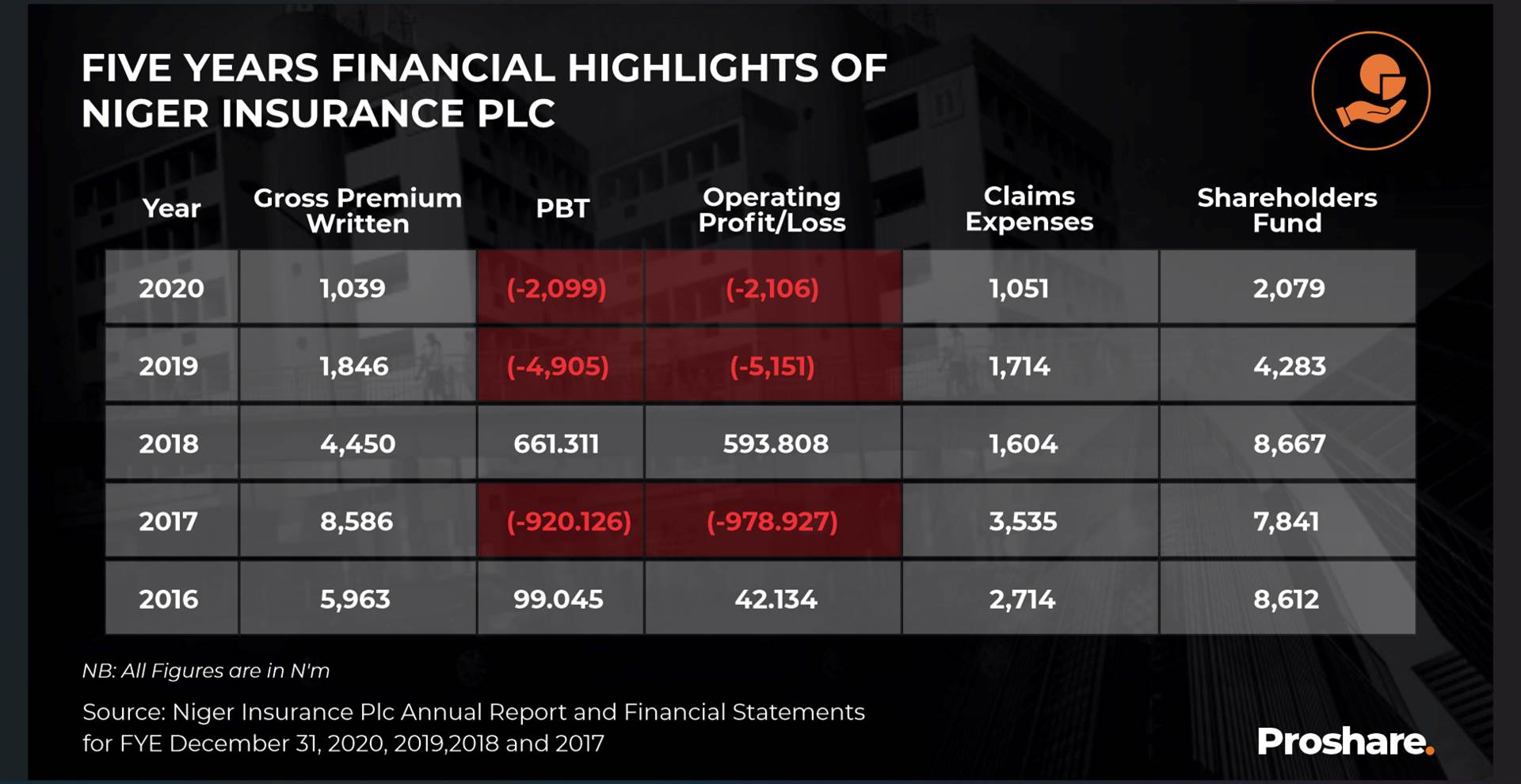

Probably, the first true sign of the Company's horrible state of affairs was as reflected in its Financial Statement for the year ended 2019. It was not only questioned by market analysts, but Niger Insurance Plc was forced to issue a rejoinder published in national newspapers. For instance, it recorded an operating loss of N5.151bn from N594m profit in 2018! (See Chart above)

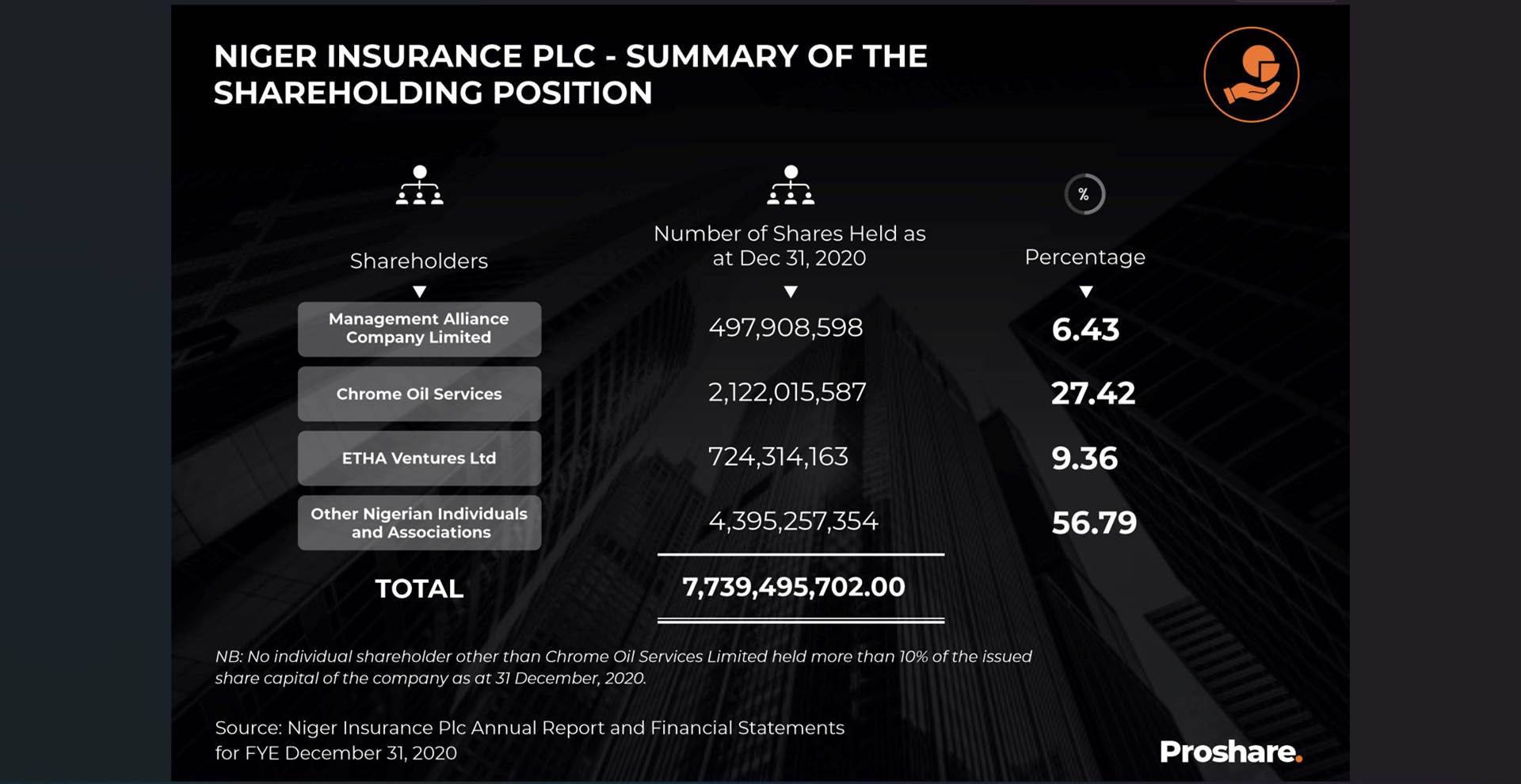

The concerns of Shareholders have since heightened as all efforts to correct the wrongs and put the Company back on track have not yielded positive results. From the Company's Financial Statements as at December 31, 2020 the single largest Shareholder with 27.64 percent is Chrome Oil Services, a leading business group owned by Sir. Emeka Offor. This quiet billionaire is also the power behind Guinea Insurance Plc, a licensed general insurer, making some market analysts wonder why he did not initiate moves for the merger of both companies.

Through the influence of Sir. Emeka Offor, Niger Insurance Plc got a good chunk of the insurance portfolio of Nigerian Customs Services (NCS) but failed to pay claims of billions of Naira due to the families of deceased officers for Group Life Assurance and Group Personal Accident Insurance policies placed between 2009 and 2014. The Comptroller-General of Customs, Col. Hameed Ali (Rtd) had threatened legal action after all steps had been taken including reporting to NAICOM but nothing positive.

Recent news of First Bank of Nigeria Plc seeking court judgement on claim of N134m further exposes the depth of the financial bad weather Niger Insurance Plc has found itself.

With a new CEO who replaced Mr. Igbiti, claimants are hearing new promises that the Company has assets worth hundreds of billions of Naira, which they are trying to sell and apply the proceeds towards the settlement of claims. Some claimants are however quick to restate that their claims are negligible amounts that Niger Insurance Plc should have settled years ago. Many range between N800,000 and N2,000,000 mostly for Individual Life Assurance policies.

Will NAICOM bite?

Given the sad and lamentable situation, which the mismanagement of Niger Insurance Plc have left policyholders and claimants, market analysts are watching with keen interest to see if NAICOM will press on to withdraw the operating licence of the Company.

The regulator is making lots of efforts through its Market Development and Restructuring Initiative to repair the damage done by insurance companies like Niger Insurance Plc and rebuild public trust, but existing and potential policyholders are yet to be convinced that NAICOM is capable of finishing the race.

With recapitalization in the cooler due to court injunction and the delay in signing the Insurance Amendments Bill into law, it is very doubtful that the administration of Mr. Sunday Thomas will achieve much towards improving the desired growth and development of the insurance industry in Nigeria.

To earn the confidence Nigerians require to go into any insurance company in Nigeria to transact business and execute contracts, NAICOM needs to keep Nigerians informed, especially about the insurance companies it has taken actions against, and protect policyholders strongly against insurance companies that fail to meet their obligations in time.

It is Niger Insurance Plc today, which other insurance company (nay giant) is on the verge of collapse? This is the reason analysts clamor for an industry risk assessment and sustainability audit/test as a critical first step in re-establishing trust with the consuming public.

This ought to be a growth period, not a burial season.

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top