Lagos, NG • GMT +1

Lagos, NG • GMT +1

747 views

747 views

The NBS released its Q2 GDP data today as scheduled. Pleasantly surprising to analysts was the sharp increase in real GDP growth to 3.54%. This is 0.43% higher than in Q1’22 (3.11%). This means that there is an increase in output of goods and services of $1.8bn. From an analytical point of view, one data point increase does not mean a trend but suggests that the economy could be on a mend. At a time of a general slowdown in global growth, a spike in Nigerian GDP is good news for investors and creditors. However, the question on the minds of most analysts is why this blip or spike?

While there is enough reason to cheer, it also calls for a moment of sober reflection. Of the 46 activities tracked by the NBS, only 33% of them expanded compared to 54% in Q1’22. The sectors that expanded are not the ones that have greatest employability. Hence, it will have a minimum impact on unemployment, which is stubbornly high at 33%. Some of the sectors that contracted (rail transport and livestock) are the ones that are labor-intensive. The slowing sectors (agriculture, construction, trade, manufacturing, etc) are mainly major employers of labour and have huge linkage effects.

Is this economic growth (3.54%) propelled by speculation or panic?

The purchasing Managers Index, which is one of the most efficient predictors of cyclical trends, has been oscillating in the last 7 months. An interesting observation is that new orders increased consistently in the last 5 months. This raises questions as to whether manufacturers are optimistic about the future or they are hedging against a falling Naira. The fear of dollar scarcity means manufacturers will front load their inventory requirements, creating an illusion of expansion as against the real picture. This will manifest in a possible decline in purchases and ultimately slow GDP growth in the coming quarter.

Time Lags Between Events And Impact

During the quarter under review, the economy witnessed several exogenous shocks, which will manifest themselves in Q3. The second quarter was the pivotal moment of the Russian-Ukraine war, spike in diesel prices, currency crisis and monetary tightening. However, there is a time lag between events happening and the transmission effects. Hence, the real impact of these events will be felt in Q3.

Breakdown of Data

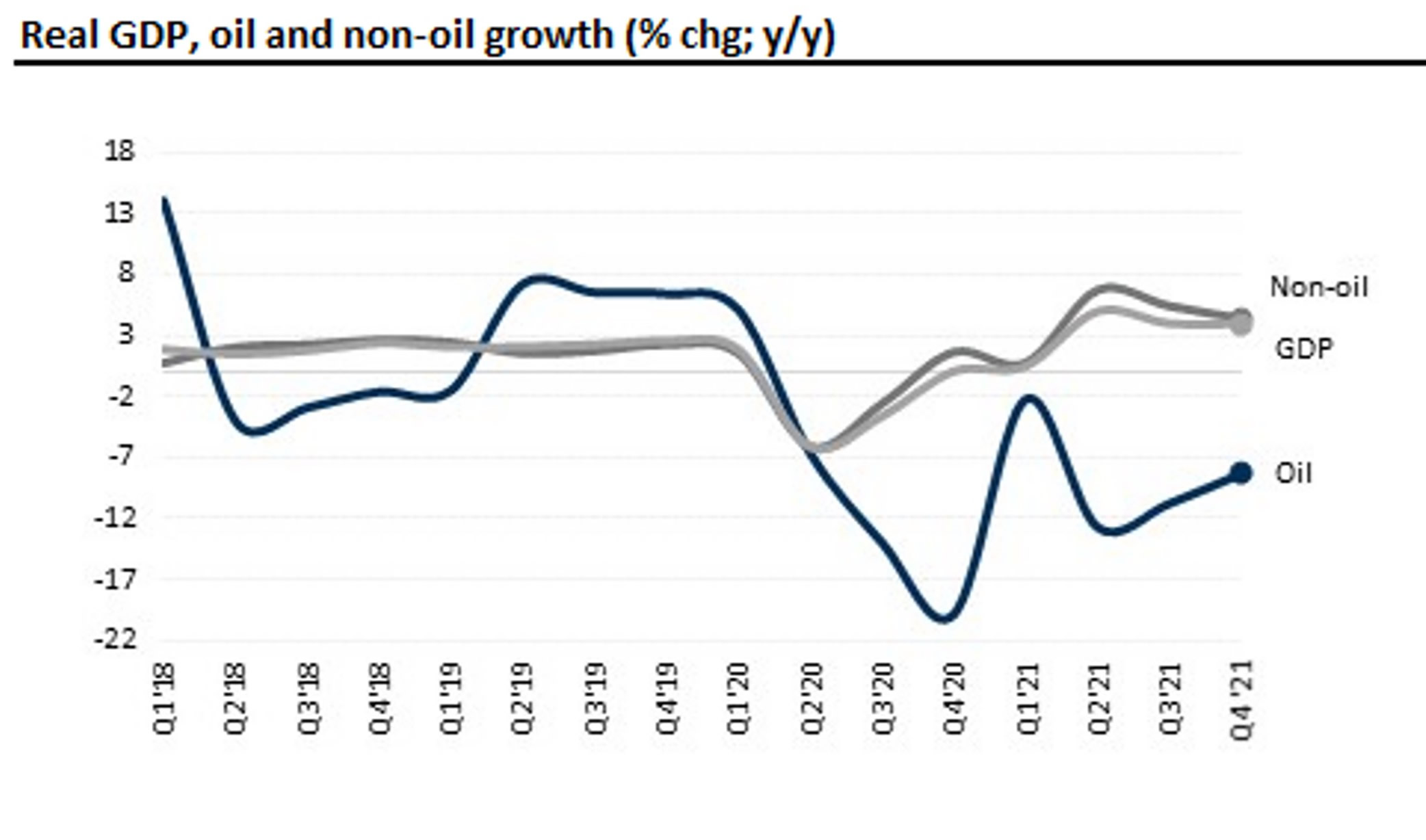

Oil and Non-Oil Sectors

The non-oil sector growth slowed to 4.77% from 6.08% in Q1’22 and 6.74% in Q2’21. This was largely due to a slowdown in ICT, trade, finance and manufacturing activities. Meanwhile, the sector’s contribution to GDP rose to 93.67% in Q2’22 from 93.37% in Q1’22 and 92.58% in Q2’21. The oil sector contracted by (11.77%) from the previous reading of -12.65% in Q2’21. Oil theft, pipeline vandalisation, underinvestment and other operational challenges continue to undermine oil production. The sector’s contribution to GDP slowed to 6.33% from 6.63% in Q1’22 and 7.42% in Q2’21.

Sector Breakdown - 15 Expanded, 22 Slowed, 9 Contracted

Of the 46 activities tracked by the National Bureau of Statistics, only 33% expanded (15 activities) compared to 54% (25 activities) in Q1’22. It is more worrisome that the expanding sectors are relatively job inelastic (road transport, coal mining, water supply, quarrying, etc) and will have limited impact on unemployment. It appears that the spike in airline fares is increasing the use of road transportation despite security threats.

Contracting and Slowing Sectors Are Mostly Job-Elastic

Some of the sectors that contracted are the ones that are labor-intensive. Rail transportation suffered partly from the Kaduna-Abuja train attack.

The slowing sectors (sectors that grew at a slower pace) are highly job-elastic. They account for over 70% of the workforce. The aviation sector growth declined significantly due to increase in the price of aviation fuel and forex scarcity. Agric sector growth was largely affected by the planting season, while trade and manufacturing activities were affected by forex scarcity and weak consumer purchasing power. While public

Outlook

We expect real GDP growth to sustain its positive trend in the coming months. The monetary policy committee (MPC) will most likely leave all monetary parameters unchanged and continue to monitor the impact of previous rate hikes on the economy.

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top