Lagos, NG • GMT +1

Lagos, NG • GMT +1

200 views

200 views

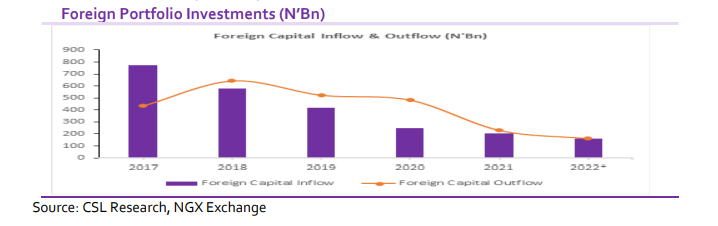

In periods of heightened risks and uncertainty, flight to safety becomes the only option. On the back of the global inflation triggered by the Russia – Ukraine war and its associated sanctions and supply chain disruption, most of the advanced economies have relied on contractionary monetary measures to stabilize prices. Expectedly, most foreign lines initially advanced to emerging markets and developing economies’ financial institutions were recalled while portfolio investors have continued to scale down their portfolio. Based on data from the Nigerian Exchange, Foreign portfolio inflows have declined steadily to N160.05bn as at September 2022 from N204.88bn in 2021, N247.27bn in 2020, N419.13bn in 2019, N576.45bn in 2018 and N772.25bn in 2017.

In September 2022, the total foreign portfolio transactions on the Nigerian Exchange stood at N19.67bn (comprising N10.08bn inflow and N9.59bn outflow) compared to N41.31bn (comprising N18.10bn inflow and N23.21bn outflow) in January and N45.43bn (comprising N20.86bn inflow and N24.57bn outflow) in February. Beyond global uncertainty as the trigger for the sell offs by foreign portfolio investors, the Naira exchange rate volatility created another layer of risk. Not only has the exchange rate been volatile, but the Central Bank has also not been liquid enough to timely meet foreign currency demands by foreign investors who needed to repatriate their investment proceeds. Recently, some operators in the aviation sector threatened to shut down operations over non-payment of trapped ticket funds with the Central Bank. Consequently, it was reported that the sum of US$265m out of US$650m trapped funds was paid on August 26, 2022. This has also been the experience of most foreign portfolio investors.

While, an overhaul of the country’s FX policies will be required, in the immediate, we believe it is critical to close the existing premium between the various official foreign exchange windows and the parallel market. There is currently about 76.58% premium between the I&E window and the parallel market. It is apparent that the CBN does not have sufficient capacity to continue its interventions at the official windows. Beyond the CBN’s monetary policies and interventions, accretion to the external reserves has been a function of the nation’s crude oil earnings. Fiscal policies and interventions aimed at boosting crude oil & gas earnings is a critical factor in ensuring exchange rate stability in the near term.

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top