Lagos, NG • GMT +1

Lagos, NG • GMT +1

238 views

238 views

It is not clear what we should make of the well-established fact that interest payments on debt are perennially consuming nearly 100 percent of the revenue available to the Federal Government of Nigeria. There is currently no consensus on the way forward. This piece simplifies the issues and points the way forward.

1. Structure of Nigeria's Debt Stocks

The main highlights of Nigeria's debt realities according to recent statements credited to the DG of the Debt Management Office DMO in BusinessDay are:

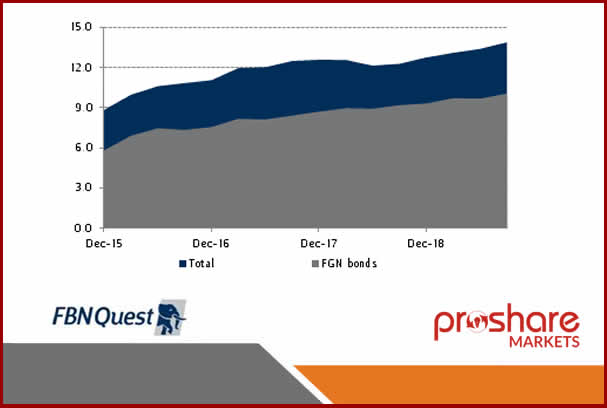

Public debt stock was N35.465 trillion or 21.92% GDP at the end June 2021

- Domestic Debt - made up of mostly Treasury Bills and FGN Bonds, and negligible stocks of Treasury Bonds, FGN Savings Bonds, FGN Sukuk and FGN Green Bonds, was 61.34% of the total debt stock;

- External Debt - made up of multilateral, bilateral, and commercial loans, was 38.66%,

- Multilateral Loans is 54.88% of total external debt stock and are all concessional 'donor funding'.

- Bilateral Loans or 'donor funds' from China, France, Japan, India, and Germany of 12.7% of total external debt stock funds building of airports, rail tracks, roads, and so on. China accounts for 78.7%.

- Commercial Loans is made up of mostly Eurobonds and miniscule stocks of Diaspora Bonds, and Promissory Notes; accounting for 31.88% of total external debt stock.

3. FG Debt of N29.46 trillion was 83.07% of total debt stock;

4. States & FCT debt was 16.93% of total debt stock; and

5. LGs Debt was 0% of total debt stock.

Source: DMO finalizes plan to restructure CBN's N10trn overdrafts to a long-term Tenored debt - Businessday, 15 Sept 2021

2. Excruciating Debt Costs to Revenue Ratios

The 2022-24 Medium Term Expenditure Framework and Fiscal Strategy Paper (MTEF &FSP) provides the following instructive facts and projections of Nigeria's debt costs to revenue ratios:

- Debt costs of N3.3 trillion in 2020 was 84.89 percent of N3.9 trillion FGN revenue. The actual debt cost was 113 percent of what was projected in the budget, while the actual revenue was only 73 percent of what was expected in the budget.

- Debt costs of N1.8 trillion incurred from January to May 2021 was 97.56 percent of N1.845 trillion actual revenue. The actual debt cost was 138 percent of what was projected in the budget, while the actual revenue was only 55 percent of what was expected in the budget.

- Projected debt costs are N3.6 trillion in 2022, N4.9 trillion in 2023, and N6.16 trillion in 2024; against projected revenue of N8.36 trillion in 2022, N10.18 trillion in 2023, and N10.9 trillion in 2024; implying debt cost revenue ratios of 43 percent in 2022, 48 percent in 2023, and 56.52 percent in 2024.

3. Reality Check on Fiscal Projections in the MTEF

Considering the now established tendency for actual debt service to overshoot projections and actual revenues to undershoot projections, it should be obvious to most unbiased observers that the debt service to revenue ratios over the 2022-2024 horizon would be closer to the stark realities depicted by the recent outturns in 2020 and January to May 2021 of 85 to 98 percent of revenue than the wish-driven 43 to 56.5 percent of revenue projected in the 2022-2024 MTEF.

Many countries now entrust responsibilities for fiscal making projections and setting fiscal rules to independent fiscal commissions who work in advisory capacity to avoid inadvertent biases inherent in allowing executive to set fiscal goals and rules for themselves.

4. Growing Concerns about High Debt to Revenue Ratios

Different observers have expressed disparate and rather confusing views about how to resolve the high debt service to revenue ratios. To hit the bullseye however, we must agree on the target to aim at among the growing and confusing list of rival targets being thrown up by supranational observers, reputable national thought leaders, and key government officials.

- Supranational bodies like the IMF and the World Bank have expressed concerns that high debt service to revenue ratios crowd out spending on economic and social priorities and urged the government to cut subsidies and/or increase taxes.

- Reputable national thought leaders have opined that high debt service to revenue ratios reveal a debt sustainability or solvency problem and urged government to stop borrowing and/or cut costs of governance.

- Key government officials have suggested that low revenue is the problem, and if we can get more revenue, the high debt service to revenue ratios will become much lower.

5. Government Says Borrowing Continues

Meanwhile, Nigerian government has been borrowing more, is still borrowing more, and has bluntly made it clear that it will be more in the foreseeable future, partly because it must raise more debt to pay down over 10 trillion Naira outstanding ways and means advances from the central bank of Nigeria, and quite honestly, we must all admit that it is hard to fault the pragmatic realism of this disposition.

The suggestions from the supranational bodies, reputable national thought leaders, and key government officials all seem to suggest that we should leave the problem of high debt costs unresolved and go about solving entirely different problems like removing subsidies, increasing taxes, stopping borrowing, cutting costs of governance, or raising revenue.

6. Dealing with High Debt Costs

This piece argues that they all fail to address the primary portfolio management problem at issue- the urgent need to reduce or eliminate interest payments on existing debt stock through wholesale replacement of expensive commercial bonds in FG portfolio with interest-free commercial bonds that now abound at home and abroad.

This portfolio management failure has absolutely nothing to do with subsidy regime, tax regime, costs of governance, revenue adequacy (liquidity), and debt sustainability (solvency). While these unquestionably deserve chapters in Nigeria's unfolding financial narratives, they are red herrings in the chapter on minimizing or eliminating interest payments.

Insinuating that debt costs will increase as debt stocks increase is flawed because debt costs could well decline as debt stocks increase if government choses more efficient debt types, the most efficient in the current global environment being interest-free commercial bonds.

This piece points out that the only sensible way to solve the problems presented by debt costs is to reduce or eliminate the debt cost itself; not increase revenue, increase tax, remove subsidies, stop borrowing, or reduce cost of governance.

This places the ball back squarely in the court of the DMO. Issuance of interest-paying bonds is an unnecessary and avoidable drain on our hard-earned revenue, even if we have the revenue in abundance. Reducing interest payable on any given debt stock is the only enduring way of resolving the issue at hand. Other seeming solutions are red herrings.

7. The Silver Lining

Opportunities for issuing non-interest debt abound locally and internationally, other countries are seizing heavily on these opportunities, but Nigeria continues to shun such opportunities by continuing to unnecessarily pile up interest-paying debts in commercial markets at home and abroad.

The fact that public debt stocks are growing astronomically higher in both values and percentages of GDP in most healthy developed and emerging economies, while interest payments have remained reasonably small in values and as percentages of revenues and GDP is partly explained by increased issuance of more public asset-linked debts instruments, and partly because assets that are eligible for debt-securitization are easily convertible for equity-securitization at home or abroad, and vice versa, like Saudi Arabia did with ARAMCO, in initially issuing IPO at home before seeking sukuk globally. Assets-linked securitization strengthens fiscal situation in endless ways.

8. Connecting to Global Wave of Asset-Linked Securitization

Global wave of asset-linked securitization increasingly converts dead, idle, and underutilized public corporate, infrastructure, physical, and intangible assets into new sources of immediate fiscal liquidity and future revenue flows that are required to close infrastructure gaps and unlock latent growth potentials, without the burden of interest payments through the budget, as commercial investors in such securities are happy to wait for the profits or rent to be unlocked by the assets, mostly at their own risk, with the comfort that most of such securities have investment grade ratings by foremost agencies.

9. Lessons from Our Peers

The latest example is that global outstanding sukuk reached $754.1 billion in Q2 of 2021, according to Fitch, after racing from US$178 billion in 2011 to US$573 billion in 2020. New issuance of US$174 billion in 2020 was about the same as the total outstanding stock in 2011.

More importantly, sovereign, and quasi-sovereign bonds accounted for 52 percent of issuance in 2020, as Malaysia, Saudi Arabia, and about six other governments, mostly from oil producing countries, successfully issued interest-free commercial bonds to replace interest paying ones; corporate bonds were 38 percent; supranational bonds were 10 percent.

Sukuk's shares in the total funding mix has only just leaped to 36 percent in 2021, according to Fitch. Underscoring the fact that the gains of India and a few other countries who have learnt to attract record levels of foreign capital inflows by issuing asset-based bonds targeted at their diaspora predated the rise of sukuk, and the breakthroughs of China, Brazil, India, and a few other developing countries in leveraging on local assets to receive record levels of global equity inflows through cross-border mergers and acquisitions and greenfield deals have long been underway before the rise of sukuk. Nigeria's options are endless!

10. The Way Forward

Nigeria should aggressively restructure its debt portfolio by replacing interest paying commercial bonds with interest-free commercial bonds on a wholesale basis to drastically reduce or eliminate the N4.9 trillion annual average interest payments that is projected in the 2022-2024 MTEF. Rather than issue interest paying bonds to fund infrastructure, we should create special purpose vehicles for packaging infrastructure assets for interest-free financing through asset-linked non-convertible or convertible bonds. Ideally, this should happen in a rule-based fiscal regime with an independent advisory fiscal commission as watchdog.

About the Author

The Author, Dr. Ayo Teriba is the CEO of Economic Associates and can be reached via email at [email protected].

Click here to go to Author's Page

EDITORIAL NOTE:

Three hours after publishing this piece, the Debt Management Office released this press statement - Nigeria Raises USD4bn through Eurobonds; 30-Year Eurobonds Raised at 8.25% - Proshare, 22 Sept, 2021

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top