Lagos, NG • GMT +1

Lagos, NG • GMT +1

7445 views

7445 views

Saturday, December 25, 2021 / 10:57 PM / by The Analyst, Proshare Research/ Header Image Credit: Ecographics

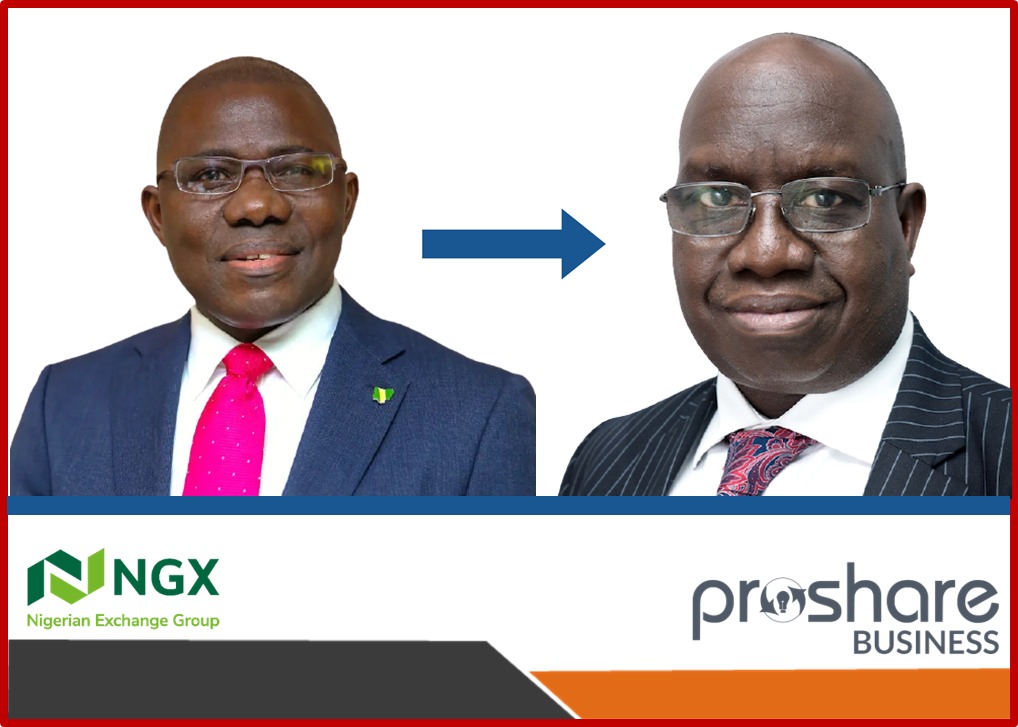

On Friday, December 17, 2021, Nigeria's financial media was shocked by the announcement of the resignation of FBN Holdings Board Chairman, Mr. Remi Babalola. The news filtered in during the evening as stockbrokers had just ended the heated passion of trading, and market operators had hoped that they had closed the best pre-holiday market deals of the year. The Nigerian Exchange (NGX) All Shares Index (ASI) was oblivious of the news of Babalola’s resignation and closed at 42,353.31 or rose by +0.2%. In comparison, FBNH shares masked the gravity of the group Chairman's decision and rose by +0.42% to N12.05. The market's calm indifference was understandable as Nigeria's premier financial Holdco's board change was a developing story newly announced and unassimilated.

However, in a swift response to the group Chairman's resignation, the Central Bank of Nigeria (CBN) replaced Mr. Babalola with Mr. Ahmad Abdullahi, a one-time Director of Banking Supervision of the CBN and current board member of the African Finance Corporation (AFC).

Abdullahi’s emergence as the Chairman of FBNH's board of directors was not particularly problematic given his broad regulatory knowledge. However, the former regulator's private sector inexperience and past regulatory antecedents (CBN and the Nigerian Deposit Insurance Corporation (NDIC)) would appear to make his appointment one of convenience rather than strategy. Abdullahi’s regulatory background created the semblance of another CBN boot in the doorway and hands on the rudder, leaving analysts to wonder about the true extent of control/intentions of the banking system supervisor over FBNH. For example, does Abdullahi's appointment amplify the CBN's concept and application of its 'forbearance’? Does it mean that the regulator (by proxy) and not shareholders through their nominated board now provides Nigeria's oldest bank with strategic and operational guidance?

Wading Through Murky Waters

The CBN's heavy hand in FBNH after replacing the previous Boards of the group and the bank in April appears to have been an ominous shadow over the Babalola-led board, one foretold by our analysts, hence the diligent follow-through by the unit on the precedent-laying actions by the Governor. It would appear that given the pedigree of the names that replaced the erstwhile board, as expected, the former Chairman's brave effort at refining processes and redesigning structures to provide an atmosphere for optimal performance was going to be a litmus test. Unfortunately, as they will discover, elephants are too big to turn corners. They need time and patience, two attributes in short supply in the race for recovery, which from the onset provided a collision course only a few not adept at governance issues at this level would have missed.

Babalola, weighed down by a platoon of operational problems, felt that he had plenty of patience to get things right following the mandate but little time. The banker and past Minister of State for Finance under the Umar Yar Adua's Presidency may have realized belatedly and come to the late conclusion that he was appointed as a public display of commitment to transparency standing in front of a messier reality. The easy take-over of FBNH by the CBN alludes to this. Still, the ex-banker should not be excused for underestimating the magnitude of the problem considering his previous insider status.

Those close to FBNH's immediate past Chairman pointed out that Babalola belatedly realized that the 'optimisation' of decisions and the rebuilding of the group’s statement of financial affairs would be hard and complicated. He, therefore, decided that suboptimal solutions would be acceptable as long as they created operational value.

His game plan, it appears, was to rebuild in small steps and then use the early successes to make a significant push to establish a basis for his eventual exit in April 2022, one that would lay a template for a turnaround managers' exit. Unfortunately, his patience and commitment to a proper process had a shorter expiry date than he thought.

Several factors would appear to have toppled the applecart and planted Babalola's feet firmly through the exit door.

The first challenge was the reluctant cooperation amongst colleagues at the bank board who had different interests they represented. The inability to establish a coherent majority interest objective was not only a challenge, but it also became a tool for sub-optimal utilization of the board given the 'expectations' from the 'regulator.' In both strategic and operational matters, as the document review, we accessed revealed.

Those close to the Holdco and bank had observed that queries had started flying fast and furiously early in the new administration as certain senior officers tended to act without either the knowledge or approval of the Holdco board. Another problem was that the regulator could 'without a stake' nullify decisions taken by the Holdco, including reversing decisions of the group's board and, indeed, its Chairman.

There were instances where the Holdco would send a query to the bank, which would be ignored by the bank's management as the sector's regulator routinely deemed disciplinary action by the Holdco to be of no effect. According to an actor close to events at the Holdco, "it was like watching a sprinter told to break a longstanding one hundred meters record, only this time, he would do it with his hands tied behind his back. The outcome was unavoidable and failure inevitable."

The issue was, therefore, not whether Babalola would leave but when. The decision to resign was known to persons in the system, and it was just a matter of how to mitigate the consequential outcome of such action.

Based on the former FBN Executive Director's antecedents, personal principles, and professional disposition, the decision matrix was clear, and the resignation decision settled (see illustration below).

The Battle of the Big Boys

To make matters worse, significant shareholder troubles began to mount on the back of struggles for commanding equity stakes in the financial institution. The battle between new notable shareholding entrant and energy maven, Femi Otedola, and existing influential and significant shareholder, Oye Hassan-Odukale, had raised the stakes for power and influence at the financial lender.

According to a credible board source, "the battle between Otedola and Hassan-Odukale, created sparks but kindled no fire that could worry the board. The two gentlemen were at best distractions; the more serious problem was the lack of clarity over Otedola's equity funding source. There was a growing belief that the equity play had deeper undertones with stronger institutional hands rolling the dice."

"Seeing that the underlying game was that of chess and not checkers; and that the interests involved were formidable, it would appear that our Chairman did the smart thing and hit the stop buzzer retiring from a game he could never win. He avoided allowing his name used as an imprint of validity."

In eight months, Babalola had seen the many grey sides of corporate Nigeria he had thought existed only in the hyperactive and perhaps over-indulged imaginations of Nollywood scriptwriters. At FBNH, fact and fantasy became indistinguishable. Babalola was either misled to have accepted the appointment or was motivated by something other than the Holdco's legacy reality. Whichever it was, he will have to address this introspection on his terms, boldly and frankly facing the man in the mirror.

While he went through this appreciation of reality, growing doubts about why Otedola acquired 7.57% of FBNH shares gained currency when he insisted in a press statement that he was not gunning for a seat at the FBNH board table but merely wanted to see good returns coming from sound management at the group. According to media reports, Otedola had said, "I am simply an investor who saw an opportunity in the financial institution and decided to take advantage of it through the investment I have made. My interest, contrary to speculations, is not to become Chairman of the bank or its Holdco. Moreover, I am in semi-retirement."

Of course, this could have been casual modesty, but Otedola is not known to be either casual or decidedly modest. As we alluded to in the article The Phoenix Rises Again, the Nigerian business gamemaster is deliberate, smart, and calculating, depending on which side of the table you are sitting on.

In this light, the decision not to sit on FBNH's board was not a nod to the competence of the other people running the company in which he 'currently' holds the largest individual interest. It was more a desire to keep to his chest the subtle undertones of his equity move and to shield the expected final payoff from the prying eyes of third parties. A single move to sell his stake under a "willing buyer and willing seller" mode would change the ownership structure of the legacy institution, and the market caught this. The tussle with Hassan-Odukale over the appellation of the largest individual shareholder of FBNH was smoke; keen observers believe that the fire is even yet to come.

Under the Hawk's Eye

In understanding the backroom maneuverings and the potential equity payoffs around the Otedola FBNH share acquisition, Babalola's "regrettable" exit finds context and meaning. The erstwhile FBNH director came out of a fog, economists call "mission creep," as he slowly developed hawk eyes to see the broader corporate card game. The game included a few flash moves that classical economist Adam Smith once called the "invisible hands" motivated by what he also called "animal spirits."

The local media freely attributed Babalola's resignation to the battle for shareholder supremacy between Hassan-Odukale and Otedola, but this was not entirely or majorly true. The former Chairman of the Holdco was reasonably comfortable managing the fragile egos of the two significant company shareholders, but much less easy was managing the personal frustration at not taking optimal operational decisions without the rib-breaking hug of a regulator.

A Holdco insider, who requested anonymity, as he was not authorized to speak on the matter, noted that the former Minister of State for Finance was irritated at the continued poor governance practices that still prevailed in the system. Babalola, according to the source, was tired of tiptoeing around decisions taken between the regulator and the bank without providing first recourse to the Holding company's board. The alleged sidelining of the Holdco's board concerning strategic and consequential operational bank issues was said to have left as our taste in the mouths of those at the Holdco.

"Babalola was in a steamy hot kitchen with few ingredients, minimal ventilation, and a recipe book which only he intended to follow or perhaps understood but yet was subject to the decision of the regulator." In other words, the ex-Executive Director of FBN was, skinned, sauntered and roasted even before he took the job as FBNH's Chairman.

Babalola came to the card game late. Eight months into the steering of the financial Holdco, several veils began to fall from his eyes, and increasingly the task at hand became less one of a salvage and recovery mission than a moral and professional burden. The shaky house of cards had served him with a few trick hands as he suddenly realized that he had no Ace, King, Queen, or Joker. The game was stacked nicely against him (see illustration below).

So, how does this affect the bank and Holdco's stakeholders?

The stakeholders are likely to be affected differently with each coping as best they can. Minority shareholders, however, may need to keep their eyes on the ball as backroom significant shareholder manoeuvres may break away from collective interests. The high-stakes negotiations and agreements reached between known and unknown interests around the bank and Holdco could lead to surprising future outcomes (see illustration below).

As minority shareholders keep an eye on future earnings, the regulator needs to ensure that the Holdco and bank internalize best governance practices and create an internal oversight structure that prevents the reoccurrence of legacy challenges.

Both institutions may need to do the following:

- Business Process Audit (BPA) to recalibrate and reinforce the quality of customer-facing operations

- Review workflow optimization measures to enhance operational efficiency

- Respect inter-organizational authority and control to avert 'mission creep.'

- Commit to a Rethink, Rebuild, and Rebrand agenda

- Elevate corporate business rather than office politics

- Internalize loyalty

- Reimage business operations in a world of volatility, uncertainty, complexity and ambiguity (VUCA)

The lender must equally prevent insider distrust, sustain performance metrics, and establish leadership in adopting and adapting digital technology. Ahmad Abdullahi has his job cut out for him. Part of the mandate would be to see that the Holdco and bank staff remain adaptable to the evolving open and digital banking landscape (see illustration below).

Indeed, Abdullahi (with his limitations) will have to address the concerns of minority shareholders who, among other issues, have been worried about the following:

- The appointment of Mr. Nnamdi Okonkwo, former Managing Director of Fidelity Bank, as the new FBNH Managing Director replacing retired U.K. Eke. Minority investors were worried about his legacy challenges from his previous bank.

- Public arguments over who was the largest individual shareholder of the group were causing problems of adverse public perception of the financial Holdco. The minority equity holders have been concerned about the alleged 'battles' overcontrol of the financial lender, which has promoted a poor image of the group’s governance stability and sustainability.

- The appointment of new directors had equally become a sore point for minority shareholders. The shareholders have complained that despite the Central Bank (CBN) Governor repeating that the Holdco's board change was to protect minority investor interests, this, in their opinion, has not happened. They argue that recent developments still reflect a CBN-appointed board that would likely see the appointment of directors representing a dominant investor. According to the financial lender’s smaller shareholders, the selection of two directors to the board by Otedola would stack the board against minority shareholder interests.

The rise of minority shareholders is understandable as the CBN public commitment to protecting their interests and addressing their concerns has not been fulfilled. The pole vault in shareholder activism was discernible against the rising ambiguity and uncertainty in the Holdco's boardroom.

Epilogue - When Clarity Matters

Of course, Abdullahi may have good intentions as the new Chairman of FBNH, but good intentions are not enough. FBNH/FBN's problems are not about intentions but shadowy powerplays, business alignments, and realignments masked by a need to run a profitable lending and borrowing business.

Babalola’s fears have not suddenly disappeared with his exit; they remain alive and well. Abdullahi will, therefore, need to decide where his professional and moral compass will swing and determine how he will keep the Holdco and bank on track without getting sucked into the swampy waters of disclosed and undisclosed personal interests.

So far, FBNH has had a decent price rally on the Nigerian Exchange Limited (NGX). The group’s share price has risen +69.72% year-on-year(Y-o-Y), +67.36% year-to-date (YTD) and +62.84% by half year 2021. The only disappointing number was its -2.82% three-month fall (see table below).

Yet, there are real concerns related to FBN UK's unresolved issues, the planned COM bond, treatment of recovered bad debt proceeds, and the numerous credit requests that touch on governance and credit ethos, addressed in the subscriber's confidential briefing.

Of Market Pricing and Inefficiency

When the news of Babalola's resignation hit the market on Monday, December 20, 2021, after a weekend of delayed response, analysts had expected that traders would go short as the market figures out the implications of the CBN-appointed Chairman’s resignation. Surprisingly this did not happen.

Investment professionals explain that there are two plausible reasons for the weak market reaction:

- Investors had already discounted the importance of FBNH's board of directors and considered the Central Bank to be the most vital centre of corporate action and decisions. If this were true, then the Holdco is in the position of being a slave to the bank regulator’s whims (and possibly caprices). Share price action would reflect CBN action and not the governance direction of a shareholder-nominated and approved board. Suppose this was correct, the stock market is in dire trouble, and the Securities and Exchange Commission (SEC), the capital market regulator, needs to be worried.

- Information asymmetry has led to retail traders being ignorant of insider actions such that minority investors and their brokers wrongly discount the importance of FBNH's board actions. The difference between small and large investors in understanding the implications of the board or individual board member action on the fortunes of the Holdco and bank creates a technical price action delay that could hurt smaller investors. The delayed retail investor reaction to market news makes equity pricing inefficient.

The fact that the market was unresponsive to the decision of Babalola to resign as Chairman of the Holdco remains a worry for analysts who feel that such important board member action should see investors respond by either taking a short position (sell) if the Chairman was essential to the rebuilding process of the group or take along position (buy) if the Chairman was a stumbling block. The Holdco's share price movement between December 13 and 23 was bullish (rose), plateaued, and reversed just before Christmas. What does this mean? So far, very little (see chart below).

Chart 1: FBNH's Share Price Movement 13th - 23rd December 2021

Source: NGX, Proshare Research

The resignation of Remi Babalola and the appointment of Ahmad Abdullahi as Chairman of FBNH have been business as usual. A slight bump on the road to somewhere or nowhere.

Abdullahi's Burden

Despite what appears to be a steady corporate recovery, Abdullahi would do well to note that the new job is not sinecure or a place to sit and collect easy pay. He will have to roll up his shirt sleeves or Babanriga and balance the desire to get the operational numbers rolling along the right track while equally handling the individual meddlesomeness and personality conflicts that could slash and burn corporate performance.

Equally, Abdullahi must check his deck of cards and be sure that it is fair, thus giving him a decent chance to win the transition and transformation game, unlike his predecessor. He must also quickly learn that not all the players are sitting at the table in plain sight, so there may be unexpected consequences for any decision taken. He must understand the underlying abuse of entrusted power for private gain and its costs.

Another major problem for Abdullahi is the moral and professional burden of unexpected insight. Often, ignorance is bliss, but ignorance could also be bitter and painful. The new FBNH chairman may have to find peace within the troubling knowledge of the true interests fighting for the soul of the institution. Nevertheless, as far as outsiders are concerned, there is no guarantee that the shaky FBNH house of cards will get proper structural support even with the change of its corporate captain.

Analysts have raised concerns over the disturbing coincidences of ex-CBN officials taking over large local deposit money banks (DMBs). A former Deputy-Governor of the CBN, Mr. Tunde Lemo, has recently completed arrangements with CBN approval to take over Nigeria's second oldest bank, Union Bank. The vehicle for the approved takeover was Titan Trust Bank, licensed to carry out banking activities as recently as 2019. FBNH being under the direction of a former director of the CBN raises a red flag of governance intrusion by regulatory insiders or their recent or former associates. The role of Abdullahi may rightly or wrongly be to align FBNH and FBN firmly behind the regulator.

Dotted Connections

The relationship between the CBN and FBNH/FBN goes beyond personnel. FBN serves as the clearinghouse bank for a few deposit money institutions (DMBs) with weak shareholder funds and poor liquidity. These institutions have operational credit exposures to FBN for which the CBN provides forbearance, underscoring the importance of FBN to systemic financial stability. Banks like Heritage Bank, Unity Bank and Enterprise Bank come under special CBN arrangements and may soon require decisive regulatory resolution. The issue, however, is whether the solutions feed into a CBN-affiliated old boys network or whether a professional arms-length best offer approach is adopted. So far, the old boys CBN network seems alive and well.

Contrary to earlier media reports, Tunde Lemo is not the major acquirer of Union Bank through Titan Trust Bank. It turns out that the former CBN Deputy Governor owns relatively small shares in Titan, but he does give leadership direction as Chairman of its board. Titan Trust Bank is 85% owned by a private group registered abroad. The group equally has interests in fast-moving consumer goods (FMCGs), Beverages, Pharmaceuticals, Agriculture, and Trading. Titan Bank has the ambition of being a Tier 1 bank in seven years, meaning that from the end of 2018, when it started operations, it expects to be at the gilded table of big banks by 2025at the latest.

The Union Bank/Titan Bank combination may result in further banking sector consolidation as weaker banks may be forced to allow themselves to be acquired between 2022 and 2023 as the burden of forbearance weighs heavier on the CBN.

As things stand, Babalola’s resignation from the board of FBNH opens a window to the give-and-go emerging from the management of deposit money banks (DMBs) under the CBN's laudable forbearance programmes. However, critical to the success of these programmes is governance integrity and coordination with the capital market regulator SEC, the primary equities Exchange, NGX, and their representatives of minority shareholders. Some issues need to be urgently addressed to protect market integrity and minority market interests:

- SEC must take a keener interest in the management of banks listed on the NGX

- CBN must abide by the codes of listed companies and should not willy nilly appoint management and boards outside established governance rules

- NGX should raise red flags when board issues become a matter of regulatory concern. The management of the Exchange cannot remain docile when company boards are changed by interests outside those recognized by the Company and Allied Matters Act (CAMA).

- The control and management of the board of directors of listed companies in special situations should be resolved by the CBN with the SEC and NGX subject to 'sunset' clauses that limit the period of intervention and reestablishes the appropriate procedures for board and management appointments

The capital market oversight evidence so far does not speak to optimism. Stakeholders have to remain vigilant and interpret actions proactively to establish new paradigms.

Finally, introducing a woman to a man is no excuse for sleeping with her after her wedding day. Regulators must understand boundaries and set such boundaries to sustain and support the best global oversight practices. Babalola may have left FBNH, but the problems persist, and the only way to tackle them is by stepping back and seeing a broader interest beyond self.

Kindly send feedback, comments and contributions to [email protected]

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top