Lagos, NG • GMT +1

Lagos, NG • GMT +1

8321 views

8321 views

Tuesday July 26, 2016 5:10AM /FDC

While market volatility has made many investors nervous, there are a few investment vehicles that have continued to grow. Exchange Traded Funds (ETFs) are pooled investment vehicles with shares that can be purchased or sold on a stock exchange at a Market determined price. They offer investors access to the markets such as the Nigerian Stock Exchange (NSE), the Standard & Poor's 500 (S&P 500), the Financial Times Stock Exchange 100 Index (FTSE), and Johannesburg Stock Exchange (JSE) while offering diversification, access to non-traditional asset classes and hedging tools.

Since the introduction of ETFs in 1993, they have gained widespread acceptance in most developed markets. Over the last 10years, investors’ demand for ETFs (both retail and institutional) has grown markedly, which in turn has led to a greater variety offered by ETF sponsors. Now there is one for almost every type of market index or financial benchmark in existence. As of September 2015, the ETF and exchange traded products industry managed 5,978 products, representing total assets of $2.8trn.

The Way It Works

An ETF originates with a sponsor - either a company or financial institution - who determines the investment objective. The originator is also referred to as an active participant (AP). The AP creates a basket of assets (e.g. equities, bonds, commodities, alternative assets, etc.) and in exchange for those assets receives creation units in the form of ETF shares.

Once the ETFs have been listed on the various exchanges, investors can then purchase and incorporate the securities into their respective portfolios. Institutional and retail investors can access ETFs in both the primary and secondary markets.

In the primary market, investors buy these securities directly from the company issuing them, while in the secondary market, investors trade securities among themselves. Investors can buy and sell these shares just like any other shares on an exchange

with easily accessible prices. The company with the security being traded does not participate in the transaction. A company publicly sells securities for the first time on the primary capital market. In many cases, this takes the form of an initial public offering (IPO).

ETFs share risks common to other pooled investments such as mutual funds. An ETF is similar to a mutual fund as it offers investors a proportionate share in a pool of stocks, bonds, and other assets and is most commonly structured as an open-ended investment.

A major difference is that investors trade ETF shares on the secondary market (stock exchange) through broker-dealers, just like other stocks. In contrast, mutual fund shares are not listed on stock exchanges. Instead, retail investors buy and sell mutual

fund shares through a variety of distribution channels, including investment professionals—full-service brokers or independent financial planners. Pricing also differs between mutual funds and ETFs. All orders of mutual funds placed during the day will receive the same price— the Net Asset Value (NAV) - while for ETFs, the price of a share is continuously determined on a stock exchange and can trade on any intra-day price. Hence the price an investor buys or sells may not be the same as the NAV.

ETFs are subject to standard downside market risks as well as individual risks specific to the content of each ETF. To mitigate general downside risks, investors can hold Inverse ETFs. These produce the opposite return of the underlying asset. For example, an investor who bought into an inverse crude oil ETF would have recorded gains in the period when global crude oil lost 65% of its value. By holding positions in inverse ETFs investors not only diversify, but can hedge against downside risks.

Even though rarely considered by the average investor, tracking error is a general risk that can have a potential impact on returns. As ETFs grow in complexity their tracking error (the difference between the returns of the index fund and the target index) grows.

While replicating the performance of an index may seem easy, there are a number of ways tracking errors creep into ETFs. The most common sources of tracking errors are high expense ratios and rebalancing of indexes. High expenses of an average fund are likely to reduce returns relative to those of the index being tracked. Rebalancing or Index reconstitution with the removal or addition of securities could also introduce tracking errors. When this occurs, fund managers have to make adjustments to their own fund composition. If this is not well monitored, it could lead to tracking errors.

While replicating the performance of an index may seem easy, there are a number of ways tracking errors creep into ETFs. The most common sources of tracking errors are high expense ratios and rebalancing of indexes. High expenses of an average fund are likely to reduce returns relative to those of the index being tracked. Rebalancing or Index reconstitution with the removal or addition of securities could also introduce tracking errors. When this occurs, fund managers have to make adjustments to their own fund composition. If this is not well monitored, it could lead to tracking errors.

To address this, investors are advised to understand what they are buying and make sure that the ETF index fund they are considering does a good job in tracking its index. Usually this information is provided by managers of the fund and in cases of IPO’s, prospectuses usually contain the necessary information.

In summary, key benefits of ETFs include diversification, the ability to engage in intraday trading and a means to hedge other investments in a portfolio.

The Nigerian Opportunity

A survey by Investment Company Institute and ETFGI (an independent research and consultancy organization on the ETF and ETP Industry) showed that the US and Europe accounted for 89% of the global ETF market in 2014.Africa and Asia Pacific accounted for $216bn of the market size. Within Africa, South Africa had the largest share of ETFs with 45 worth a combined total of $80.1bn (N15.88trn). Nigeria, on the other hand, only had seven valued at $22.6m (N4.5bn). However, with an 85% skew to equities, the Nigerian ETFs asset distribution closely aligned with the global average of 80%.

.jpg)

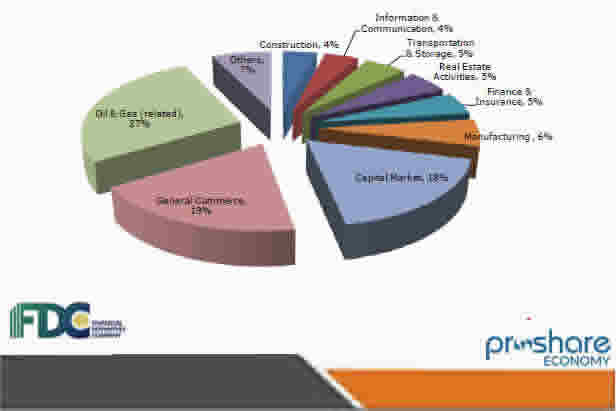

A breakdown of the Nigerian ETFs, their underlying assets and the indices they track is shown below:

.jpg)

Each of these funds attempt to replicate the price and yield performance of their respective indices by holding a portfolio of securities on behalf of unit holders that substantially represents all of the component securities of the index.

Click to Download: FDC BI-Monthly Economic & Business Update - July 25, 2016

Related News

1. An Avoidable Recession is Frighteningly Close – FDC

2. Oil Prices Recover, But May Not Be Sustainable – FDC

3. The Floating Exchange Rate and You – FDC

4. Managing Equity Investments during Market Downturns - FDC

5. Domestic Commodity Prices Declining in the Last 24hours - FDC

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top