Lagos, NG • GMT +1

Lagos, NG • GMT +1

907 views

907 views

With uncertainty and anxiety ruling global money markets, given the backdrop of historical inflation rate increases and tight monetary policy across continents, Nigeria's Central Bank (CBN) recently decided to jerk up its policy rate by 100 basis points to 14%. The Bank's move was a strong policy statement to the domestic markets that the regulator would dig into the trenches to curb inflation.

The CBN's combat readiness is, however, suspect. The regulator has spent a large part of the last four years pushing against conventional global monetary policy practices by trying to cope with the trilemma of a falling exchange rate, rising unemployment rate, and rampant domestic inflation rate through well-intentioned but cavalier credit policies. The effort has had unintended consequences.

To be fair to the regulator, some of the reasons for policy weakness were beyond its control. For example, insecurity

By using unconventional development finance (DF) approaches to economic expansion and employment, the Bank weakened its hands by using money supply controls or monetary policy rate changes to curb rising consumer prices. So far, the jury is out on how well the CBN has supported macroeconomic stability. On the balance of evidence, the outcome of the regulator's policies remains modest.

The recent policy decisions of the CBN Monetary Policy Committee (MPC) in July 2022 reflect the long walk down a rugged terrain of slim macroeconomic options.

Wise Counsel

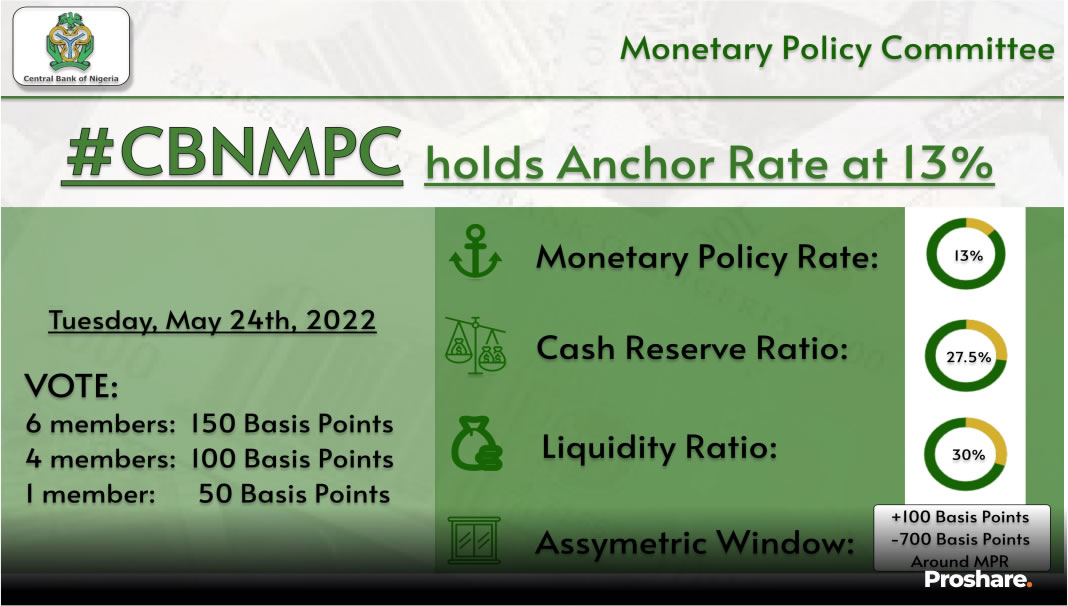

Six of the ten members of the Monetary Policy Committee (MPC) voted for a 100basis points hike in the Monetary Policy Rate (MPR). While briefing Newsmen on Tuesday, CBN Governor Godwin Emefiele noted that the Committee unanimously voted for another rate hike following the surge in inflation even after 150bp hiked rates in the May meeting.

With inflation hitting 18.6%, 89bp up from the 17.71% recorded in May, analysts expected the MPC to extend its hawkish stance. The CBN boss noted that the increase in money in circulation has fed into the depreciation of the Naira, and the decision to raise the base rates by 100bp was necessary to reduce the erosion of consumer purchasing power.

However, the unintended consequence of a rate hike is the higher cost of funds and a slow-down in manufacturing output. Still, to address the situation, the Committee recommended that the apex bank continue intervening through its Development Finance initiatives in selected priority sectors. The CBN extends loans to selected sectors through its multiple interest rate regimes at a concessionary interest rate of 5%.

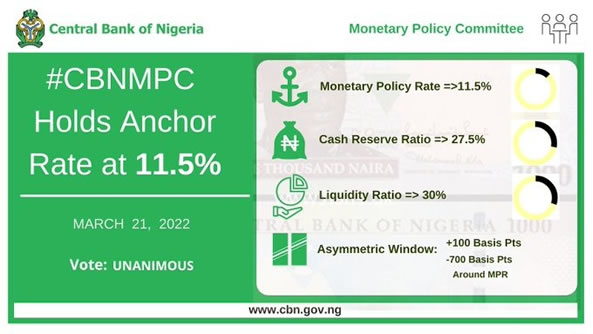

The lower rate is a subject of controversy, with several analysts calling for a review of the system seen as a market distortion. It is difficult to determine the administration's monetary policy stance (see chart1 below).

Chart 1: Adjustments in MPR 2016-2022 (%)

The MPC's Considerations

Surging Inflation, a Global Contagion

The global economy has continued to witness one of the worst inflationary spells in its history and chalked up partly to remnants of the covid-19 supply chain breakdown and the several sanctions imposed on major oil producers - Russia as a penalty for invading Ukraine. The inflationary worries on the global scale have so far proven intractable as the decision by central banks to normalize monetary policy has so far yielded very few gains in terms of lowering inflation.

The Committee considered the situation with inflation in the US (9.1%), the UK (9.4%), and several other advanced economies where inflation has exceeded the long-run targets of monetary policy authorities, reflecting the sustained increase in food and energy prices. Given the unlikelihood of OPEC+ increasing production, the Crude oil market is still expected to remain tight, and prices are expected to remain above US$100/barrel, this is despite the resumption of Libyan exports and the gradual expansion of US shale production. Rising energy prices have fed into Transport and Aviation costs in Nigeria. Food Prices also rocketed due to the geopolitical conflict in Europe (see chart1 below).

Chart: Headline Inflation & Monthly Inflation (%) May 2021-June 2022

For Nigeria, the implications of elevated crude oil prices have had is that Fiscal deficits would widen as the Federal government would continue to make large subsidy payments while the import-dependent economy would have to endure imported inflation

Monetary Policy Normalization and the fear of a BOP Dip

In a May 4, 2022, press release, the Federal Reserves communicated its plans for reducing the size of Treasury and Mortgage-Backed securities held on its balance sheet. Through a portfolio runoff (whereby the Bank reinvests only a portion of the proceeds on existing securities), long-term interest rates are expected to rise, complementing the upwardly adjusted short-term interest rate to deliver a contractionary monetary policy across tenors. In its case, the Bank of England (BoE) has indicated a 50bp hike in rates after recording a 9.4% inflation rate in June. The BoE has raised rates in each of its last five meetings. The situation in the EU is not different; the ECB is weighing a 50bp hike in its policy rate as inflation surged to 8.6%.

For emerging markets, rising domestic inflation and higher yields in more advanced economies have spurred capital flow reversals like 'the 2013 taper tantrum' and 'the May 2018 storm'.

Analysts believe that the Balance of Payment problems that would ensue in many emerging markets may worsen with a fall in merchandise trade as the advanced economies seem to be on the verge of an economic contraction. In the Nigerian case, however, the fear of capital reversals appears to be tepid; At the same time, the Federal funds rate was raised from 0.25% in February to 1.75% in June, and Nigeria's foreign reserve dipped slightly from US$39.86bn to US$39.43bn over the period (see chart1 below).

Chart: Federal Funds Rate (%) & Nigeria's Foreign Reserves (US$Bn)

Money Supply

The surge in inflation could be attributed to the rise in Money supply, as Pre-election spending and early preparations for the 'Eid festival increased the demand for money. The MPC considered the need to mop up excess liquidity through a policy rate hike. According to the CBN, the Money supply rose to N48.87trn in June, up from N47.21trn in April and N42.6trn in January (see chart1 below).

Broad Money (M3) and Net Domestic Assets (N'trn) (Jan 2021- June 2022)

Private Sector Productivity: PMI on the borderline

The CBN's Purchasing Managers' Indices (PMIs) increased above the 50-index point benchmark to 51.1 and 50.3 index points in June 2022, compared with 48.9 and 49.9 index points, respectively, in May 2022. While it would suggest improvement in private sector productivity, Analysts consider the recent data somewhat counter-intuitive especially following the hike in rate in June. The Stanbic IBTC reading for June had come in at 50.9 index points, slightly above the contraction range (see chart1 below).

Chart: Manufacturing & Non-Manufacturing PMI Sept. 2021-June 2022

With the recent 100 basis points increase in the MPR, manufacturers worry about the possibility of a slow-down in economic activities, longer supplier delivery time, and the cost of raw materials and inventory.

Does the RT 200 FX program reflect the Parallel Premium Problem?

Proshare analysts believe that a significant part of the economy's inflationary worries is due to the weakening Naira. The efforts of the CBN to increase export proceed remittances came under review at the policy meeting. While the apex bank believes that the RT200 program has made significant progress, Proshare Analysts believe that the N65 per dollar rebate incentivizes exporters to remit their proceeds to the I&E FX Window, only bringing the effective exchange rate to around N490 per dollar. It, however, still leaves a parallel premium of close to N170. The premium gap would be a significant disincentive for more exporters to enroll in the program.

The Implications of a 14% MPR and Other CBN Policies

Analysts believe that the implications of the recent hike in policy rate include:

- Investors would further rebalance their portfolios away from gold and equities to fixed income securities to take advantage of rising yields

- NPLR may increase slightly, reflecting relative strain on credit performance

- PMI would further slow down, foreshadowing lower real GDP growth in the year's second half.

- Despite the 100bp increase in interest rates, Capital flows would not increase substantially due to structural issues.

- The foreign reserve would continue to be supported by export proceed remittances under the RT200 Programme. However, the considerable demand for FX in the next year's run-up to the general elections would put downward pressure on the Naira.

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top