Lagos, NG • GMT +1

Lagos, NG • GMT +1

676 views

676 views

Thursday, April 28, 2022 / 07.00 AM / Teslim Shitta-Bey, CE/ME, Proshare/Header Image Credit: EcoGraphics

Nigerian banks are in war mode as the battle for digital supremacy turns from modest fisticuffs to a full-blown onslaught. The struggle for service space dominance rather than the power of physical place captures the essence of fintech entrepreneur Brett King's recent observation that "banking is what you do and not where you go."

The numbers for digital income growth for local Nigerian banks indicate their determination to upstage one another in using mobile digital platforms to squeeze larger banking service market share. With telcos like MTN and Airtel easing into the payment service business as payment service banks(PSBs), the arena is set for a grand battle of gladiators with full buckets of financial blood scattered everywhere. The digital war will be gritty, brutal, and unrelenting.

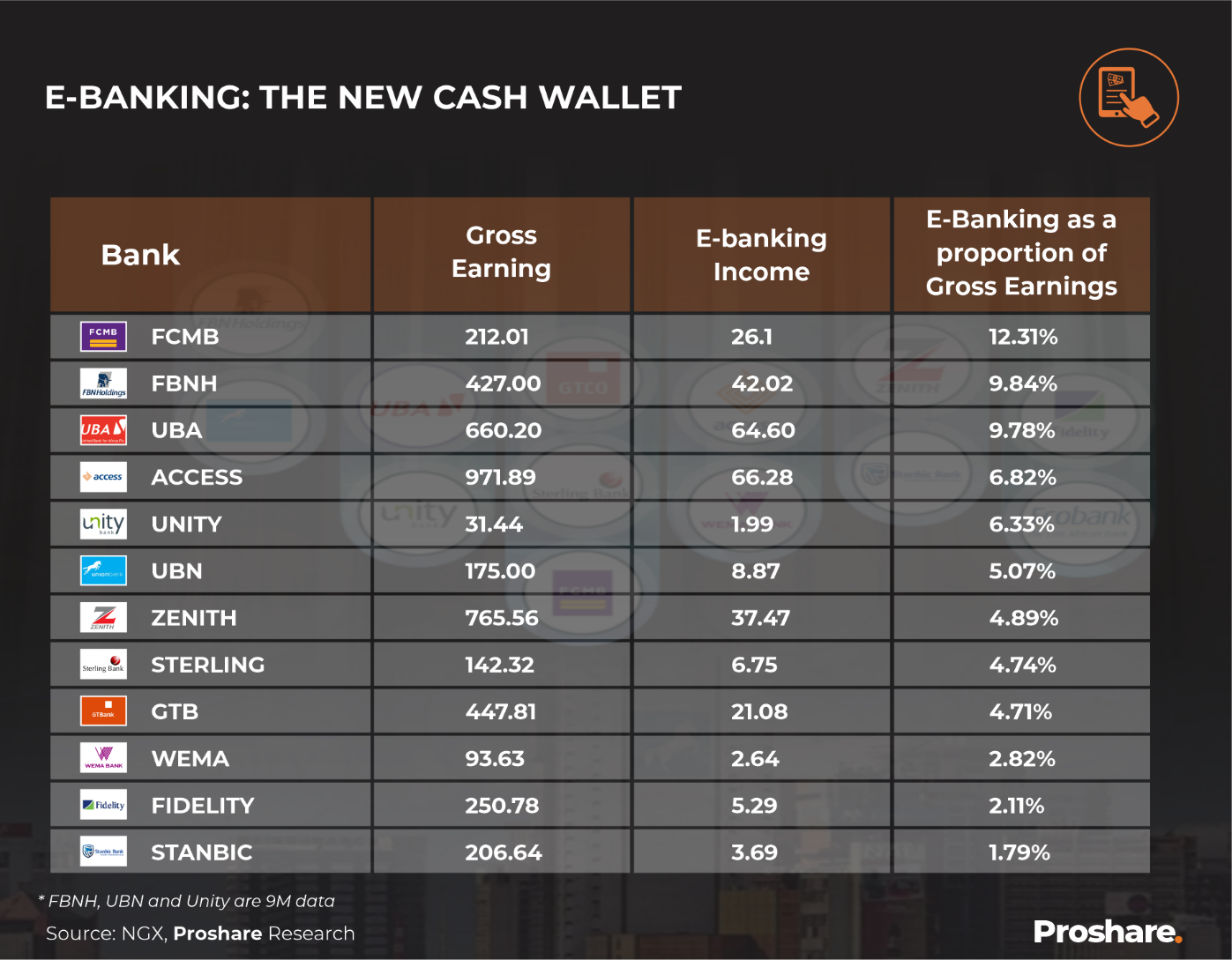

Interestingly, the upper hand in the digital wars is not strictly a function of bank asset size, deposits, or capital strength, but the bank's agility, vision, and business playbook. For example, the leader in Nigeria's digital market space as of December 2021 was FCMB, a bank considered to be a tier 2 bank according to Proshare's Bank Strength Index (PBSI).

FBNH, which seemed to have slipped from the tier 1 ranking based on a revised calculation for tier 1 status, still pulled strength in the digital warrior league table. As a proportion of gross earnings, FCMB had the best outcome for 2021, with digital banking income representing 12.31% of its total revenues. The proportion was 250 basis points above FBNH, which saw a ratio of digital revenue to gross earnings of 9.84% (in 9months 2021). Pulling behind FBNH at 9.78% was UBA (see table 1 below).

Table 1 The Weight of Banks' Emerging Digital Transactions in 2021

Surprisingly, coming at the rear of the table were Fidelity Bank and StanbicIBTC, two banks that rank as tier 1 deposit money lenders based on Proshare's PBSI calculations. Digital income as a proportion of gross earnings for StanbicIBTC in 2021 was 1.79%, while Fidelity Bank posted a figure of 2.11% or 71 basis points behind Wema Bank (2.82%), which is considered as one of the weaker tier 2 banks listed on the Nigeria Exchange Limited (NGX).

In absolute revenues, the ranking looks a shade different. Access Bank would be at the top of the table, with a 2021 digital revenue of N66.28bn, followed by UBA, with a gross digital income of N64.60bn, and FBNH with a digital revenue of N42.02bn.

Climbing up the other end of the table is Unity Bank with a 2021 digital revenue of N1.99bn, Wema Bank with an electronic banking income of N2.64bn, and StanbicIBTC with a digital income of N3.69bn. The battle for digital/electronic banking dominance is not a passing fantasy but at the heart of the evolution of banks and banking.

The War Room

Bank Corporate strategists are sharpening their approaches to building up the digital income war chest by adopting a culture change that feeds into customers' preferred and expected service journey experiences. "Customer-centric" is the competitive language of choice as banks and fintech rivals slug it out on the streets.

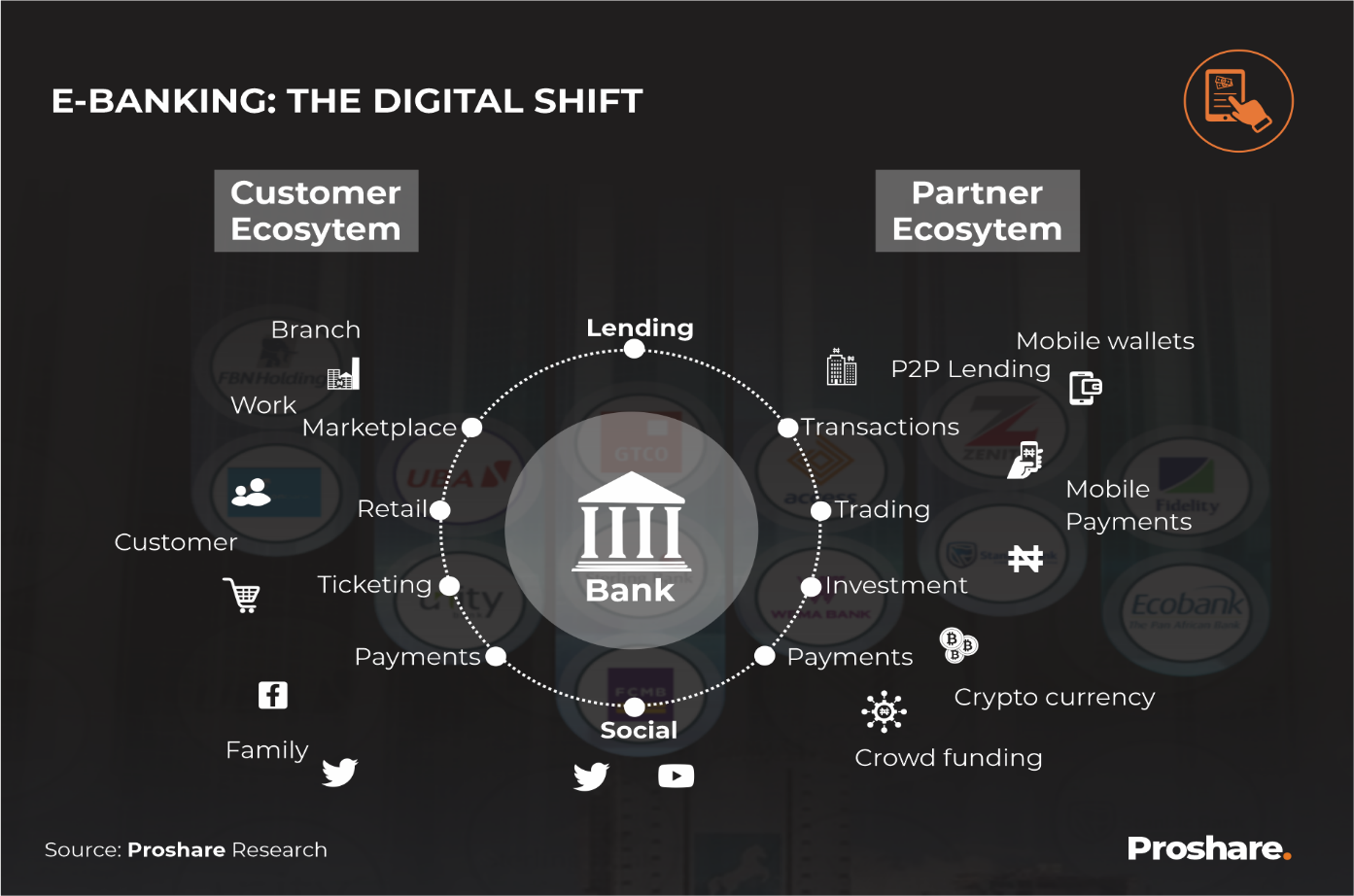

Analysts note that ecosystems are becoming nurtured to ensure that banks and their fintech rivals look for grounds where "co-opetition" (collaborative competition) improves earning outcomes for each organization. Even telcos are barging into the new digital battlefield with telecoms giant MTN spinning off its fintech operations into a separate business and providing it with the support to build products and services that increase financial service market penetration. The convergence of digital payment systems, social media, mobile telecoms devices and retail services creates a metaverse requiring different rules of corporate engagement. The digital world is where place gives way to space (see illustration 1 below).

Illustration 1 E-banking's Reality Shift

How Did David Defeat Goliath?

True, divine favour had a lot to do with Goliath's defeat at the hands of David, but a few other elements were in the mix. David fought Goliath outside Goliath's comfort zone; he shifted the terms of engagement from where strength was paramount to one where skill was of more importance. He turned the warfare from infantry against infantry to infantry (Goliath) against artillery (David). Projectiles have always defeated bayonets in war, so David was condemned by superior war strategy to succeed.

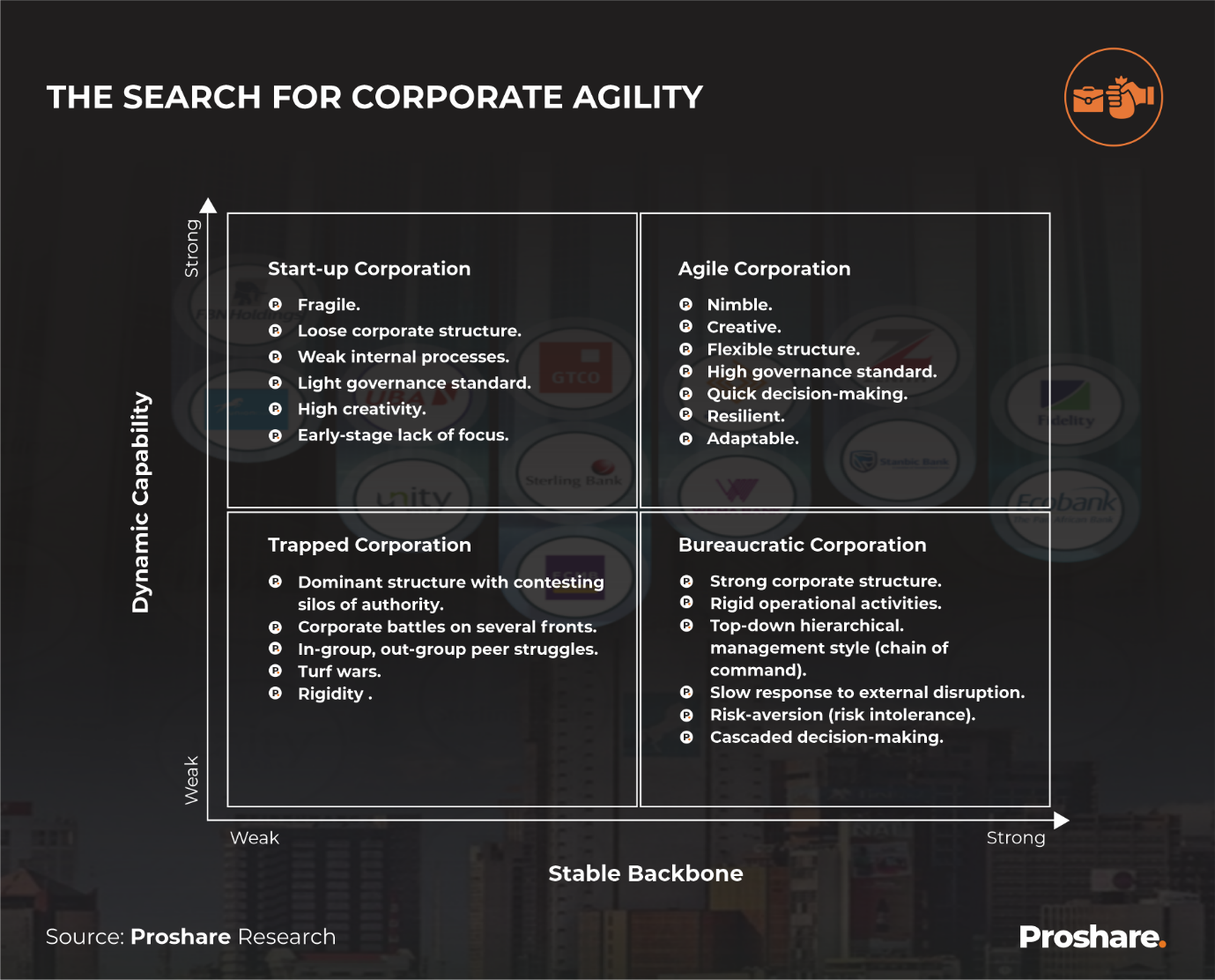

Banks are beginning to understand the lesson and are changing from exclusive brick-and-mortar combat to asymmetric digital dogfights. In other words, banks with smaller balance sheets are contesting market space with their larger rivals by being agile and flexible (see illustration 2 below).

Illustration 2 Banks Search for Agility

Nigeria's smaller banks hope to face down the blazing glare of their larger competitors by using the brilliance of local programmers and product designers to consistently surprise competitors with their understanding and peripheral vision of customers' future needs and knowledge of customers' evolving product or service experiences.

The banks that can pre-empt customer paint points will win digital market share. In contrast, those who cannot see the customers' future needs will experience a fizzling out of customary and digital revenues, which none would expect to cherish.

The new digital order is a sort of equalizer. In this space, smaller banks can go after customers of bigger rivals by being sensitive, responsive and iterative. Customers' feedback from application use would provide the inputs for a better product or service design and encourage repeat service or product engagement and loyalty.

Kicking Over A Case Study

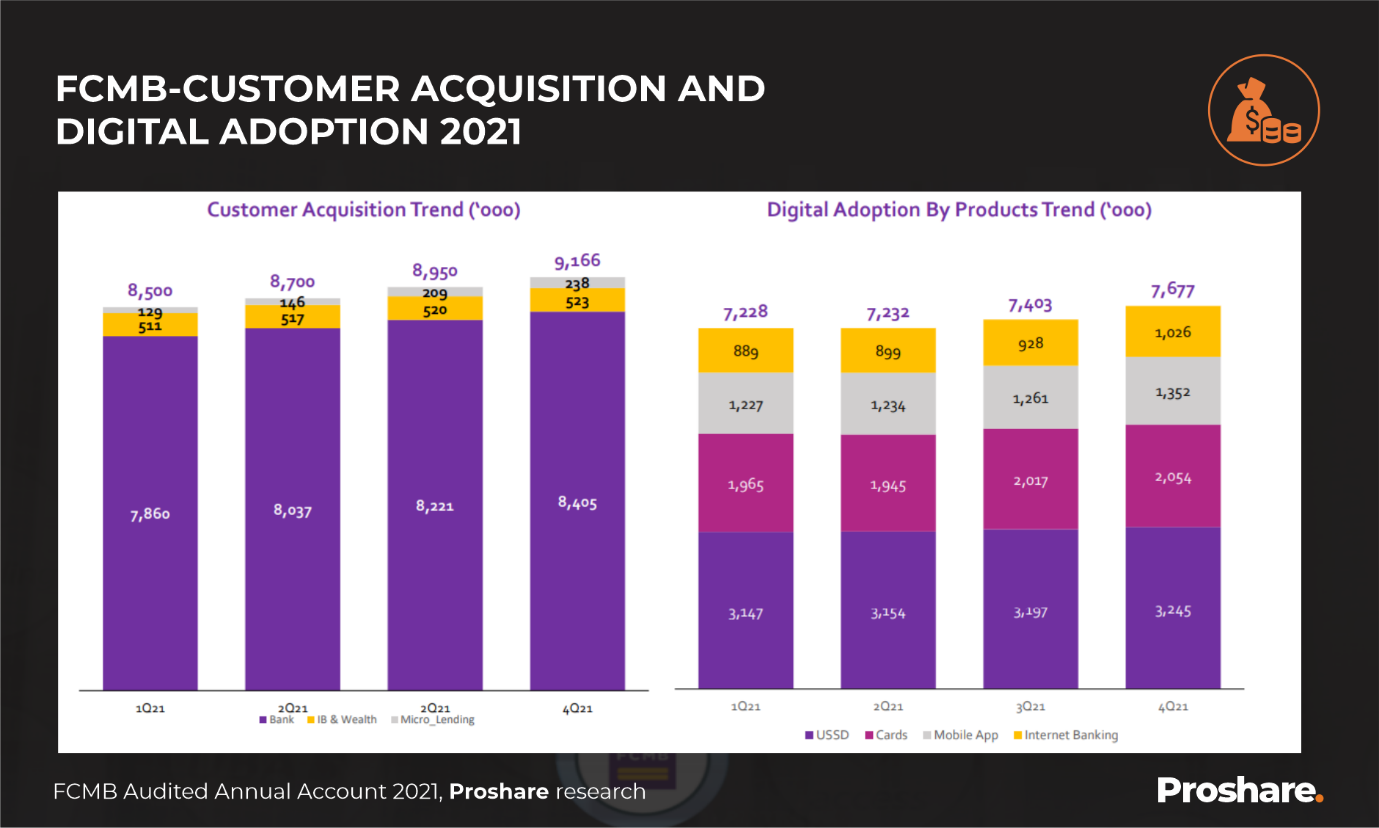

To see how banks with smaller balance sheets can upstage their bigger rivals in the battle for revenues and earnings, FCMB's 2021 performance in digital revenue growth is an obvious example. On a compound quarterly basis, the bank group saw its customer acquisition grow by +2.55% on a compound average quarterly basis (Q-o-Q) or +7.84% year-on-year (Y-o-Y).

The bank's digital product adoption rose by +2.03% on a compound quarterly basis (Q-o-Q) and +6.21% annually. Dollar-denominated products were the most popular, but cards and mobile apps combined were not far behind. Internet banking grew on an average quarterly basis by +4.89% (see chart 1 below).

Chart 1 FCMB's Customer Acquisition and Digital Adoption 2021

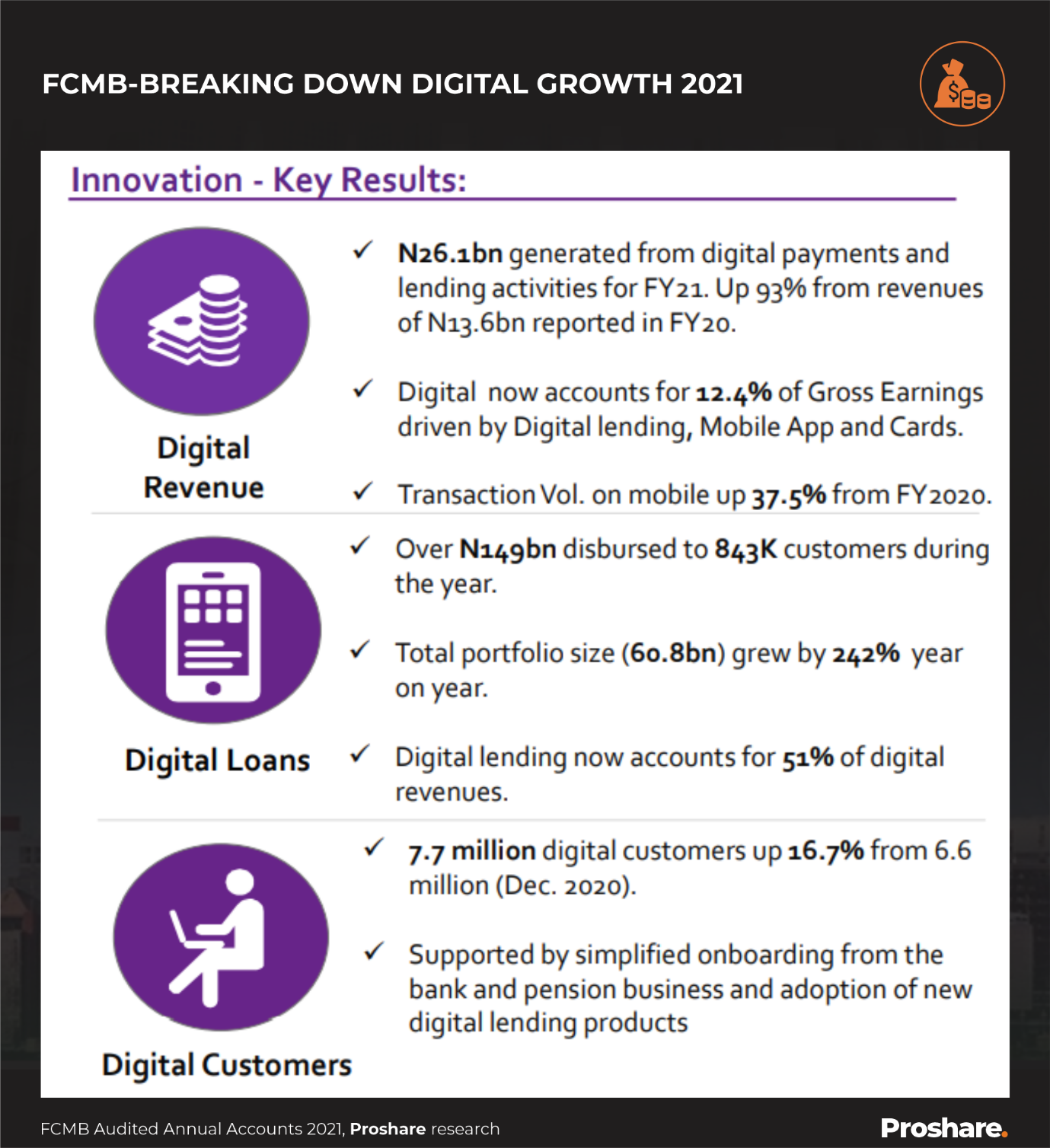

A few more numbers show how a Tier 2 bank can gain market traction if it competes for business outside traditional brick-and-mortar rules. Digital revenues of the bank rose from N13.60bn in FYE 2020 to N26.10bn in FYE 2021 or a rise of 93% over twelve months. The bank's digital revenue for 2021 was 12.31% of its gross earnings, which was the highest of all banks listed on the Nigerian Exchange Limited (NGX).

The bank disbursed over N149bn to 843,000 customers. FCMB's digital loans grew by 242% Y-o-Y with a portfolio value of N60.8bn. The bank's digital customers grew by 16.67% to 7.7m in 2021 against 6.6m in 2020 (see illustration 3 below).

Illustration 3 Break Down of FCMB Digital Growth 2021

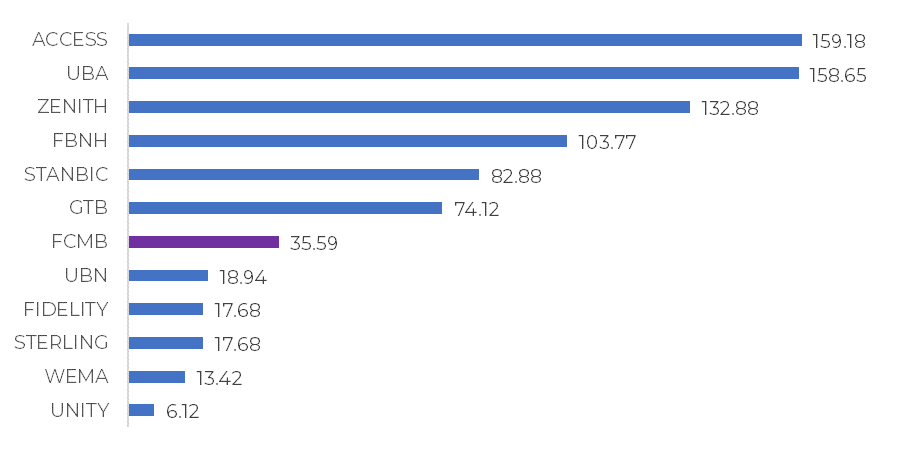

Eyeing the bank’s non-interest income in 2021, FCMB saw a notable contribution to fees and commissions coming from e-banking, which contributed 36% to non-interest-sensitive earnings. Other Tier 2 bank rivals recorded fees and commissions below N20bn with lower e-banking contributions (see chart 2 below).

Chart 2 Fees and Commissions of Nigerian Banks in FYE 2021 (N’bn)

Source: Banks’ 2021 Financial Statements, Proshare Research

Why Does FCMB Seem to Be Doing So Well Digitally?

Digital success is both an art and a science. The art comes from the ability to rethink, reimagine and restrategize product and service delivery; the science comes from applying artificial intelligence and machine learning to cleverly use recursive customer data to map service and product journey experiences. The use of big data strategically will separate David from Goliath.

Two bank technology experts that requested anonymity because they were not officially permitted to discuss with media informed Proshare that there were six principles of leveraging digital technology and analytics for competitive advantage.

The principles were equally mentioned in a previous report by McKinsey, a global consulting giant. According to these digital professionals, the six principles include (see illustration 4 below):

- Starting with a leadership-backed impact-driven strategy. Most of the time, digital strategy is a stand-alone activity driven by a bank's IT department. The drive for technological competitiveness should be led by the bank's chief executive officer (CEO) with a cross-functional team that includes IT, Product Development, Research, and Operations.

- Accelerate transformation with experience and skill. For businesses like banks to quickly build scale into their operations, they must rely on the experience and skill of their workers and professional partners and collaborators. The digital teams must be multifunctional and cohesive.

- Data architecture and governance must be the best-in-class. The data management and deployment strategy must be tested against focus group trials and feedback to improve customer journey experiences.

- Build trusted delivery methods for digital and analytics solutions. The delivery method for the product or service offering must calibrate to meet customers at their point of need; it is all too easy to have a good product or service relying upon a weak delivery channel.

- A fit-for-purpose technology stack must be built to support sustainable growth. Different levels of technology will drive a bank's business model. It is critical that each digital level 'talk' to one another seamlessly and interactively, reinforcing digital learning and service quality.

- Frontline engagement of bank front desk with customers is crucial for digital success. Analysts note that the front desk function must undergo evolution as the digital culture deepens within banks and amongst customers. Customer care officers would become caseload officers for digital interventions rather than operating personnel for physical help desks. Successful digital deployment should see customers interface with technology to resolve routine problems.

Illustration 4 Six Principles of Leveraging Digital Technology

FCMB does not tick all the boxes, but its transition is evident, and the steady growth of its digital metrics underscores its upward progression.

Banking is changing. Banks, and their customers, are riding a wave of innovation, reimagination, and reinvention, thereby intensifying retail competition and how customers are serviced. Technology has 'canceled' routine teller functions, but it has also placed less repetitive jobs in the crosshairs of software developers aiming at automating lending and loan recovery decisions as financial service operators increasingly use big data to hedge loan risks and guide loan selection. The AI of banking is not on its way; it is here and regardless of the size of banks the digital battles will be determined by the size of the fight in the dog and not the size of the dog itself.

Sponsored Ad

Sponsored Ad

Advertise with Us

Advertise with Us

Back to top

Back to top